The best way to generate a 4-5% USD cash flow from direct US Treasury investments in 2026 is by utilizing a 'bond ladder' strategy. This involves diversifying your investment across US Treasuries with staggered maturity dates, ensuring regular interest payments and guaranteeing your principal back upon maturity.

Direct US Treasury Investment vs. ETFs: Which is Better for 2026?

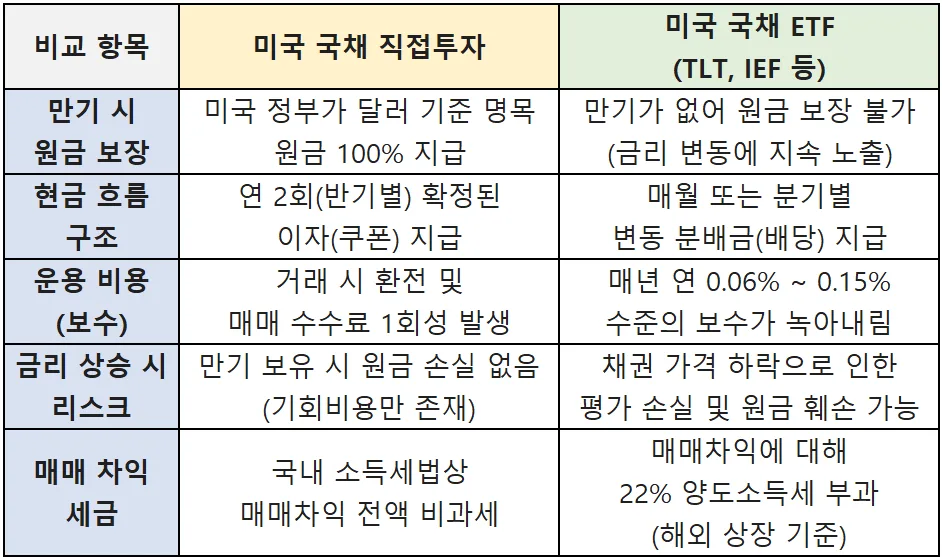

While Treasury ETFs like TLT, IEF, or EDV might initially catch your eye for US Treasury exposure, direct investment in individual bonds often proves more advantageous for investors prioritizing predictable cash flow. The key distinctions lie in principal protection at maturity and tax implications. Individual Treasuries have clear maturity dates, and holding them until then guarantees 100% of your principal back, backed by the full faith and credit of the US government. In contrast, ETFs continuously manage their holdings, replacing bonds as they mature, meaning they don't have a fixed maturity date. This continuous management incurs expense ratios and can lead to prolonged principal loss during periods of rising interest rates. Therefore, for those focused on stable income and capital preservation, direct investment is the more suitable path.

What is the 'Bond Ladder' Strategy for Staggered Maturities?

Related Articles

To address potential liquidity concerns associated with investing in long-term bonds, the 'bond ladder' strategy is highly effective. This approach involves diversifying your investment across bonds with varying maturity dates – for example, 1, 3, 5, 10, and 30 years. This structure ensures that bonds mature annually, providing a regular stream of cash for living expenses or emergency funds. Short-term Treasuries (under one year) can be purchased at a discount to their face value, generating profit upon maturity and immediate liquidity. Longer-term bonds provide semi-annual interest payments. When short-term bonds mature, you can reinvest the principal into the longest-term bonds available at the current highest rates, effectively extending your ladder and maintaining a competitive average portfolio yield during periods of high interest rates.

Is There a Risk of Loss from Currency Fluctuations? Why You're Still Safe Without Hedging

It's a valid concern that investing in US Treasuries, denominated in USD, could lead to losses when converted back to your home currency if the USD weakens. While this is technically true, the long-term picture often tells a different story. Historically, during periods of domestic economic instability or global financial crises, the USD has tended to strengthen against other currencies, including the KRW, while domestic assets like stocks have declined. Therefore, holding USD-denominated assets can act as a form of insurance, protecting your wealth. Direct investment in US Treasuries, backed by the robust creditworthiness of the US government, offers a level of stability that can effectively offset currency fluctuation risks.

What Should You Watch Out For When Investing Directly in US Treasuries?

When investing directly in US Treasuries, there are a few key considerations. Firstly, while individual bonds can be purchased for as little as $100, implementing a comprehensive 'bond ladder' strategy with multiple maturities may require a more substantial initial investment. Secondly, although US Treasuries offer very low principal risk when held to maturity, selling them before maturity can result in a capital loss if market interest rates have risen. Thirdly, direct investment requires careful attention to currency exchange rate fluctuations, which can impact the value of your investment when converted back to your local currency.