For US workers in 2026, the most advantageous way to save on taxes is by strategically utilizing retirement and investment accounts like the IRA (Individual Retirement Arrangement), Roth IRA, and taxable brokerage accounts. Prioritizing these accounts can maximize your year-end tax deductions and investment growth, potentially creating tens of thousands of dollars more over a decade compared to standard savings.

Why Are Tax-Advantaged Accounts Essential for US Workers?

Just as important as selecting the right investments is managing the taxes associated with them. Utilizing tax-advantaged accounts can significantly boost your long-term returns by deferring or eliminating taxes on your investment gains. With a regular brokerage account, taxes are typically due on dividends, interest, and capital gains each year, which can erode the power of compounding. Tax-advantaged accounts, however, allow your entire investment to grow and compound without annual tax interference. This is particularly crucial for long-term investments like broad market ETFs (e.g., S&P 500 or Nasdaq 100 trackers) or dividend-focused funds. For employed individuals, leveraging these government-provided tax benefits is essentially a guaranteed return, especially when factoring in potential tax refunds during tax season. The key question for US investors shouldn't just be 'What should I buy?' but rather 'Which account should I use to buy it?'

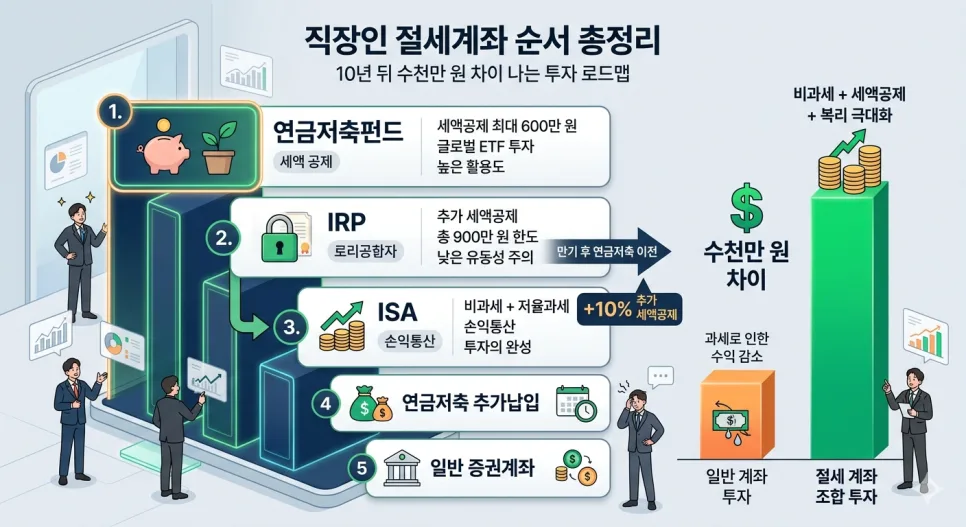

What's the Most Efficient Order for US Tax-Advantaged Accounts?

To maximize tax benefits, US workers should follow a strategic order for funding their accounts. First, prioritize contributing to your employer-sponsored 401(k) up to the company match, as this is free money and offers immediate tax deferral. If you max out your 401(k) or don't have one, consider contributing to a Traditional IRA or Roth IRA. For 2026, the Traditional IRA offers tax-deductible contributions if you meet certain income limitations, while a Roth IRA offers tax-free withdrawals in retirement. After maximizing these, look towards a taxable brokerage account for further investment. While it doesn't offer upfront tax deductions, it provides the most flexibility and allows for tax-loss harvesting. For those with high incomes, consider a Health Savings Account (HSA) if eligible, as it offers a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. The optimal strategy involves understanding your eligibility and contribution limits for each account type to build a diversified, tax-efficient portfolio.

What Are Recommended Strategies for IRA Contributions and Monthly Investments?

If you have additional funds beyond your 401(k) and IRA contributions, consider utilizing a taxable brokerage account for further investment. This account offers the greatest flexibility for accessing your funds at any time without penalty, making it suitable for medium-term goals. A key strategy here is tax-loss harvesting, where you sell investments that have lost value to offset capital gains taxes on investments that have appreciated. For those investing in dividend-paying stocks or ETFs, a taxable account allows for reinvestment of dividends, though these dividends will be taxed annually. A recommended strategy for monthly investments varies based on your capacity: investing $500 or less per month might focus primarily on maximizing IRA contributions. Between $500 and $1,000 per month, consider balancing IRA contributions with initial investments in a taxable brokerage account. For those investing over $1,000 per month, a diversified approach across IRAs, taxable accounts, and potentially an HSA (if eligible) is advisable to leverage various tax benefits and investment flexibility.

What Should You Be Aware of When Using Tax-Advantaged Accounts?

Effectively using tax-advantaged accounts requires understanding their specific rules and limitations. For Traditional IRAs, contributions may be tax-deductible depending on your income and whether you're covered by a workplace retirement plan. Withdrawals before age 59½ are generally subject to a 10% penalty and ordinary income tax. Roth IRAs have income limitations for direct contributions, and while qualified withdrawals in retirement are tax-free, early withdrawals of earnings can incur penalties. 401(k) plans have their own contribution limits set by the IRS, and early withdrawals are also penalized. HSAs have strict rules regarding qualified medical expenses for tax-free withdrawals. It's crucial to stay updated on IRS contribution limits, income phase-outs, and withdrawal rules, as these can change annually. Because individual financial situations and tax laws vary, consulting with a qualified financial advisor or tax professional is highly recommended to ensure you're optimizing your strategy and complying with all regulations.

English crawl path

Next English reads from this pilot cluster

Continue through the category hub, latest English stories, and related posts so this translated article is not an isolated URL.

Tags

💬Frequently Asked Questions

What should I check first in 2026 Tax Savings Accounts for US Workers: IRP, ISA Guide?

Does this Finance article link back to the Korean source?

Where can I find similar English stories?

English discovery path

Explore more English K-culture stories

Keep browsing the indexed English pilot cluster so Google and readers can move between this story, the category hub, and fresh discovery pages.

Original Source

Read the Korean original