A woman in her 40s successfully discharged over $75,000 of her $120,000 debt through personal bankruptcy, a process that can offer a fresh financial start. This case highlights how business failures and family support burdens can lead to overwhelming debt, and how legal avenues like personal bankruptcy can provide significant relief. This guide breaks down the process and crucial considerations for those facing similar financial challenges.

What Causes Over $75,000 in Debt for a 40s Woman?

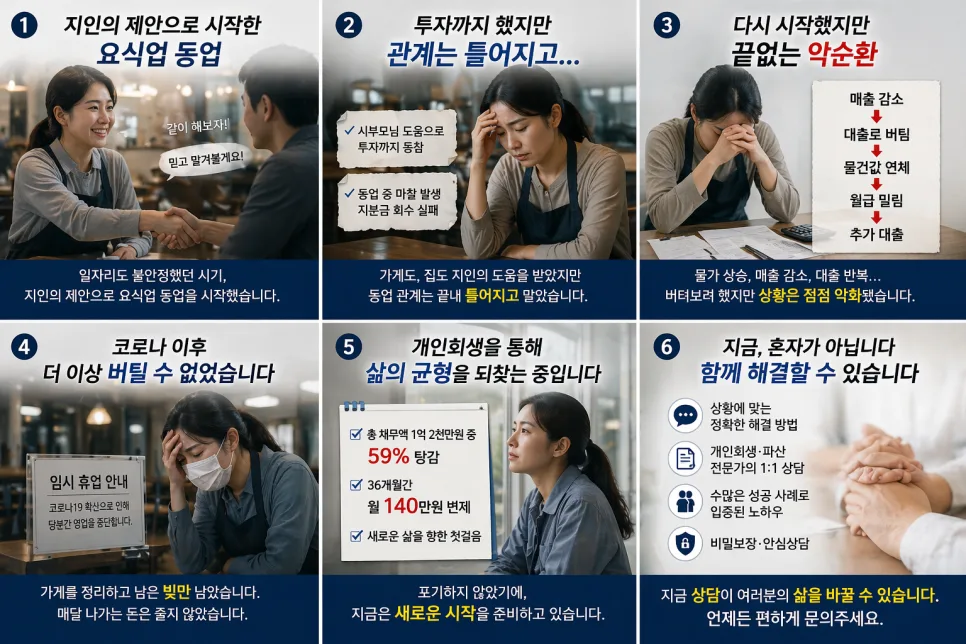

In this specific case, a woman in her 40s faced significant debt accumulation due to a failed business venture with a partner. After the partnership dissolved, she attempted to relaunch a business with her family's financial support. However, lower-than-expected sales and ongoing operational costs led to a cycle of taking out new loans to cover existing ones. The COVID-19 pandemic further exacerbated her situation, forcing her to close the business. Even after using her security deposit and business goodwill payments to settle some debts, she was left with approximately $120,000 in outstanding debt. This wasn't a result of reckless spending or speculative investments, but rather a confluence of difficult business circumstances, personal commitments, and external economic factors.

How Much Debt Can Be Discharged Through Personal Bankruptcy?

Through the personal bankruptcy process, the individual was able to discharge approximately 59% of her total debt, amounting to over $75,000 of her $120,000 obligation. Her revised repayment plan involved monthly payments of about $1,050 (converted from ₩1.4 million) for 36 months. This outcome was determined by the court after a thorough review of her income, assets, and the total debt owed. Personal bankruptcy, similar to Chapter 7 or Chapter 13 in the U.S. system, is designed to help individuals facing financial hardship by allowing them to repay a manageable portion of their debts over time, with the remainder being legally discharged. Transparency and accuracy in reporting all financial information are critical for a successful outcome.

When Should You Consider Filing for Personal Bankruptcy?

If you're facing a situation where business failure has left you with substantial debt, and you're relying on family for financial support, it might be time to explore legal debt relief options. If you find yourself trapped in a cycle of borrowing to pay off existing loans, this is a clear indicator that your financial situation is deteriorating. In such circumstances, continuing to struggle alone may not be the best strategy. Personal bankruptcy offers a legal framework to restructure your finances and provides an opportunity for a fresh start. Making a decision now that improves your financial outlook a year from now is crucial. Consulting with a legal professional can help you determine if this path is the right one for your specific circumstances.

What Are the Key Considerations During Personal Bankruptcy Proceedings?

Navigating personal bankruptcy requires careful attention to several details. Firstly, it's essential to provide complete and accurate information regarding all your debts, income, and assets. Failure to disclose any information could lead to the denial of your discharge. Secondly, adhering strictly to the repayment plan is crucial; missing payments can result in the termination of your bankruptcy proceedings. Thirdly, be aware that voluntary termination of the process may incur significant tax penalties, similar to ordinary income tax rates. Given the complexity and personal nature of these cases, seeking advice from a qualified bankruptcy attorney is highly recommended to ensure the process is handled efficiently and to avoid potential pitfalls.

For more details, check the original source below.