Many women overlook a crucial aspect when preparing for maternity insurance: the importance of 'cash-back' coverage that extends beyond childbirth to include infertility treatments. These policies are designed to significantly alleviate the financial burden of actual childbirth expenses, offering tangible support during a critical life event. This guide breaks down how to secure comprehensive coverage for pregnancy, delivery, infertility care, postpartum recovery, and C-sections, all while managing premium costs and understanding optimal enrollment timing.

Why is 'Cash-Back' Coverage Key for Maternity Insurance in 2026?

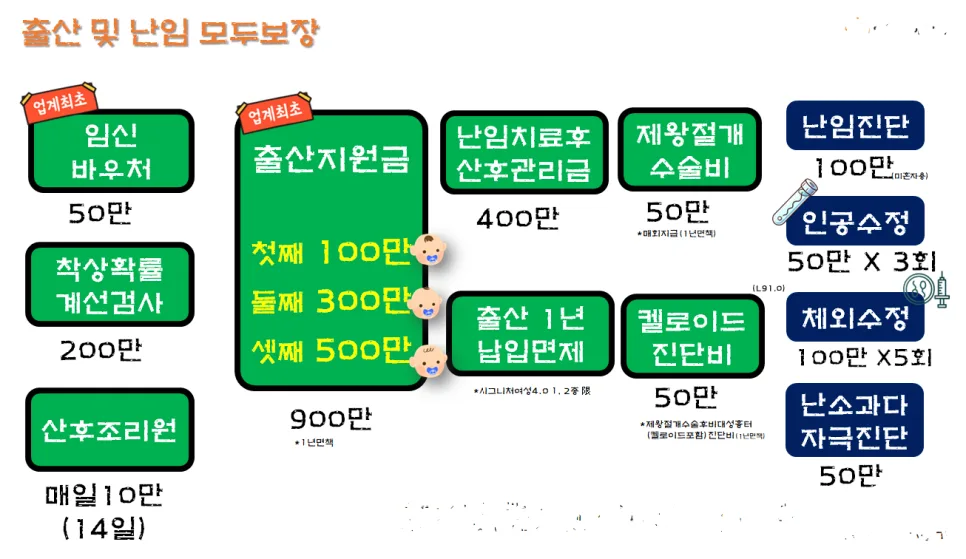

When exploring maternity insurance, the most common sentiment from prospective policyholders is, "While diverse and extensive coverage is good, what truly matters is the benefit I can actually receive as cash." The core of these policies lies in ⭐direct cash payouts⭐ rather than complex riders. This readily available cash is invaluable for managing unexpected expenses that often arise during childbirth. For instance, benefits like pregnancy congratulations money, delivery bonuses, C-section surgical fees, and postpartum care support directly offset real-world costs. These cash benefits provide a solid financial foundation for a woman's health journey, encompassing pregnancy, delivery, and beyond. For families planning multiple children, the tiered structure of delivery bonuses—increasing with each child—is particularly appealing. Furthermore, coverage for C-section scars demonstrates a thoughtful approach to comprehensive care.

What Makes Fertility-Inclusive Maternity Insurance Unique?

A notable trend in women's health insurance is the emergence of policies that offer coverage for infertility treatments. While historically focused solely on childbirth, current popular options now provide infertility diagnosis benefits, repeated coverage for procedures like artificial insemination and IVF, and additional support upon successful delivery after infertility treatment. This design treats the entire journey from 'infertility → childbirth' as a continuous process. With the average age of infertility diagnosis decreasing and treatment costs steadily rising, such comprehensive coverage is becoming increasingly vital. These policies offer psychological and financial stability to those facing infertility challenges, aiding their path to a successful pregnancy and delivery. For individuals undergoing repeated treatments, the reduction in financial strain is substantial.

Why Should You Prepare with a $30-$40 Monthly Premium Now?

While a monthly premium of $30-$40 might seem like a consideration, this insurance offers a significant advantage: after the initial coverage period (typically one year), it can be maintained for general women's health benefits even if you decide not to proceed with pregnancy plans. Crucially, the optimal time to secure this coverage with a minimal premium is 'now.' For those planning to marry or start a family within the next 1-3 years, the current period is most advantageous for enrollment. As age and health conditions change, premiums can increase, or enrollment may become more difficult. Therefore, securing this insurance isn't just a 'just in case' measure; it's a strategic decision that can only be made before certain life events occur.

When is the Best Time to Enroll in Maternity Insurance?

While enrolling after confirming pregnancy is possible, it often leads to increased premiums or limitations on certain benefits once the pregnancy is known. To minimize premium costs and ensure broader coverage, it's highly recommended to prepare before you start trying to conceive. Enrolling when your health is good and your age is lower provides the most favorable terms. This proactive approach ensures you have robust financial protection in place for one of life's most significant events, without facing the higher costs or restrictions that come later.

For more details, check the original source below.