Securing robust hospital coverage within your baby insurance plan is crucial, especially for potential stays in incubators or intensive care units (ICUs). The difference in out-of-pocket expenses for parents can range from thousands of dollars depending on the coverage limits. Therefore, meticulously reviewing the scope of hospital benefits when purchasing baby insurance is essential for peace of mind and financial preparedness through 2026.

Why Is Baby Insurance Hospital Coverage So Important?

Many parents express regret after purchasing baby insurance, realizing their coverage payout is less than expected. The primary reason for this is often insufficient hospital coverage, which is a cornerstone of these policies. Newborns, unlike adults, have a higher likelihood of requiring extended hospital stays due to prematurity, low birth weight, or congenital conditions necessitating incubator or ICU care. Without adequate hospital coverage limits, parents are left to shoulder the costs of treatment and care beyond what basic health insurance might cover. This is why, when selecting baby insurance, it's vital to prioritize comprehensive coverage across different hospital stay scenarios, including short-term (1-30 days), long-term (1-180 days), ICU stays, and benefits for congenital conditions, rather than just adding numerous riders.

What Happens When Hospital Coverage Is Insufficient?

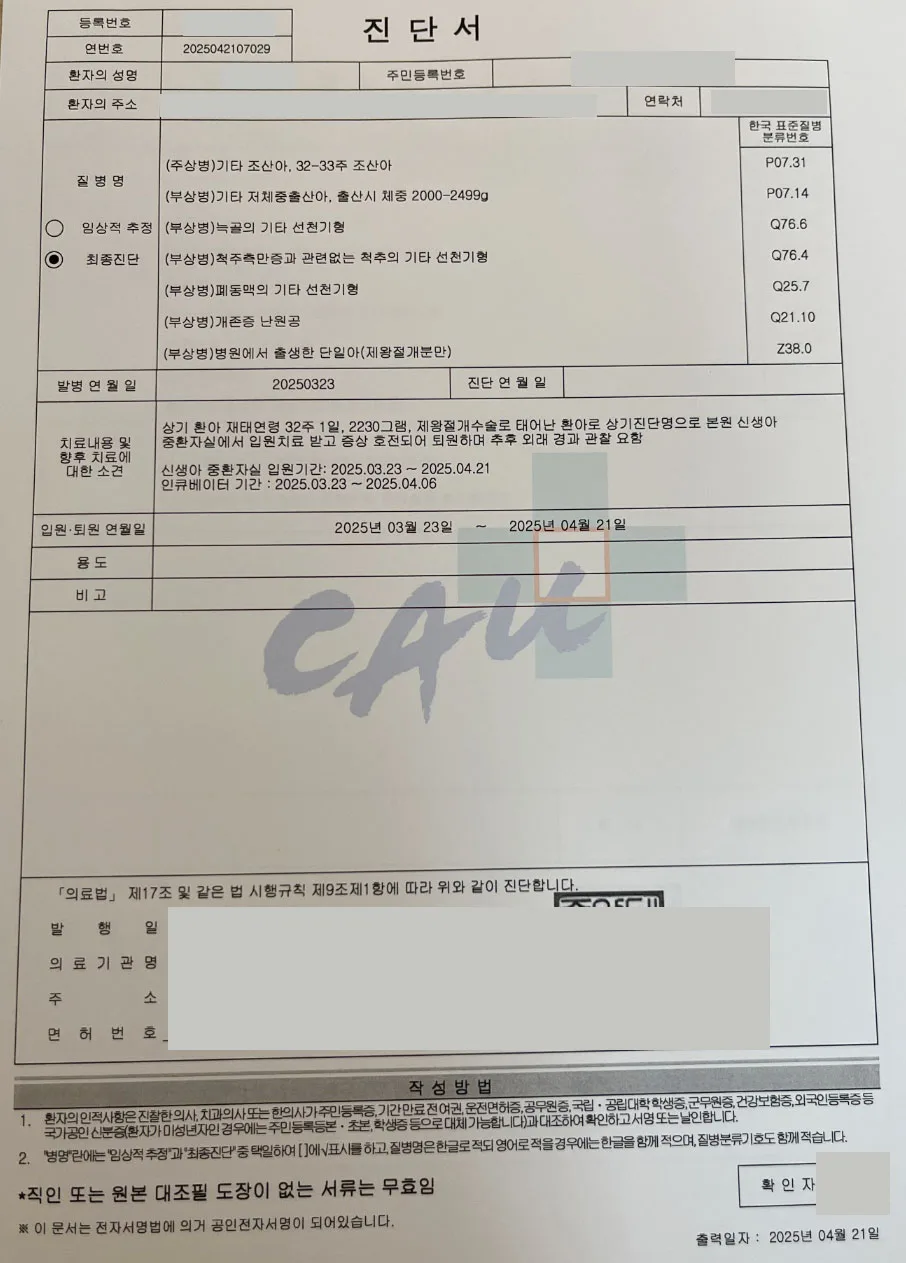

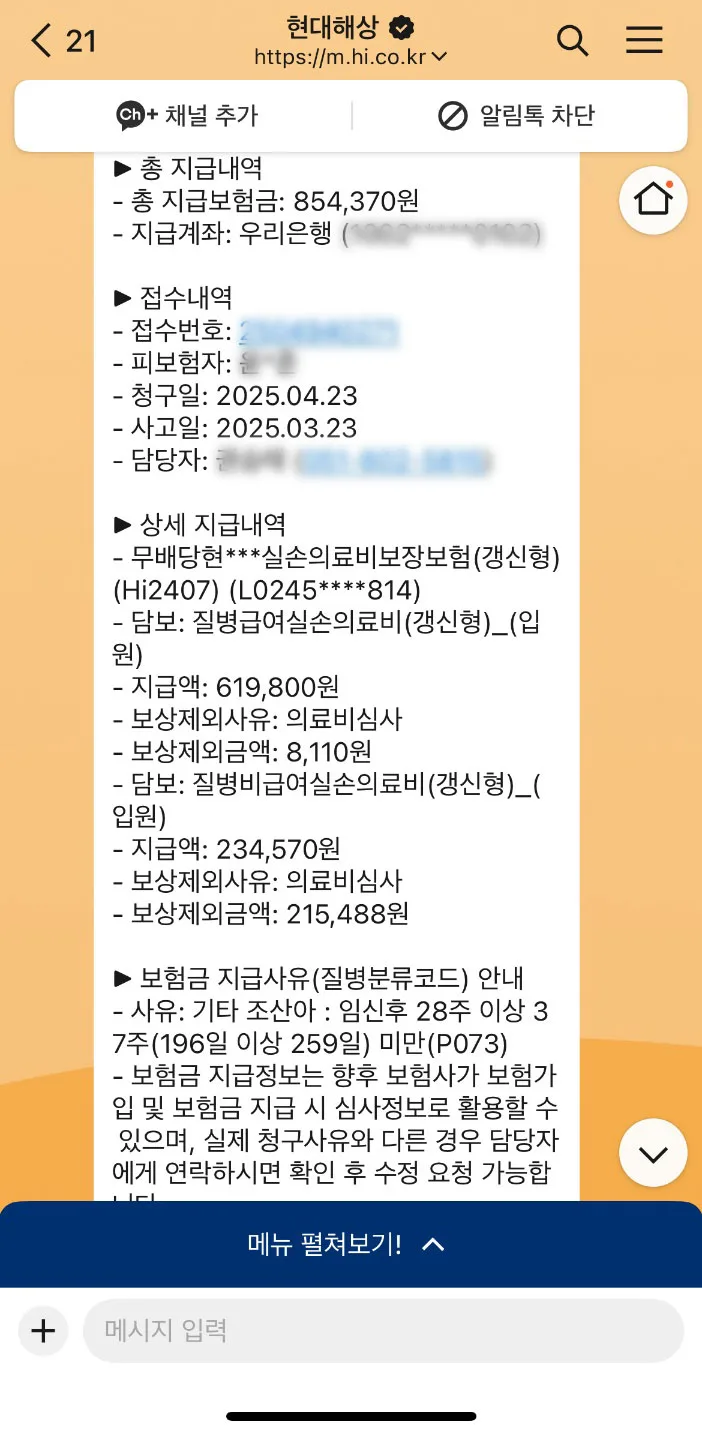

Consider the real-life case of a baby requiring prolonged treatment in an incubator and ICU due to prematurity and low birth weight. Despite clear medical necessity, insufficient hospital coverage limits meant that after the basic health insurance payout, parents had to cover a significant portion of the remaining treatment and care expenses. This situation highlights the critical gap when insurance provides coverage but not enough to truly alleviate financial burdens. Conversely, families with well-structured baby insurance, featuring comprehensive benefits for short-term stays (1-30 days), extended stays (1-180 days), ICU care, and congenital conditions, received substantial payouts, minimizing their out-of-pocket expenses. The difference in policy design directly impacts the financial relief provided during critical times.

Key Checkpoints for Baby Insurance Hospital Coverage

To ensure your baby insurance provides adequate hospital coverage, focus on these four critical checkpoints. First, verify the duration of the illness hospitalization benefit: does it cover 1-30 days, or extend to 1-180 days for longer stays? Second, confirm the inclusion of specific riders for ICU and incubator stays, which are vital for critical care. Third, assess the scope of coverage for hospitalizations related to congenital conditions. Finally, ensure the overall hospitalization benefit limit is sufficient to cover potential costs. Properly evaluating these points will help you distinguish between a robust policy and one with potential shortcomings. Since modifying coverage after birth can be difficult and costly, it's crucial to get it right from the start.

Are There Downsides to Mid-Term Cancellation of Baby Insurance?

Baby insurance is most advantageous when purchased before the baby's birth. Post-birth, enrollment may be restricted, or premiums could increase significantly. Therefore, it's essential to secure the most comprehensive hospital coverage possible during the initial enrollment period. If you believe your current policy's hospital benefits are insufficient, exploring policy remodeling might be an option, but this should be done cautiously after thorough consultation with a financial advisor. Canceling a policy prematurely can lead to the loss of paid premiums and potential difficulties in re-enrolling later, possibly at a higher cost due to age or health changes.

For more details, check the original source below.