Expecting parents in the US can explore high-yield savings options like Hana Bank's 'I-Kium' (아이키움) savings account, which offers preferential interest rates of up to 5% for expectant mothers. This account is designed to help individuals, particularly those planning for a new child, build their savings effectively. For instance, the author secured a 4.4% annual interest rate, with potential to reach 5% by meeting specific conditions, making it a competitive choice in the current savings landscape.

How Can Expecting Parents Get Up to 5% Interest with the Hana Bank 'I-Kium' Savings Account?

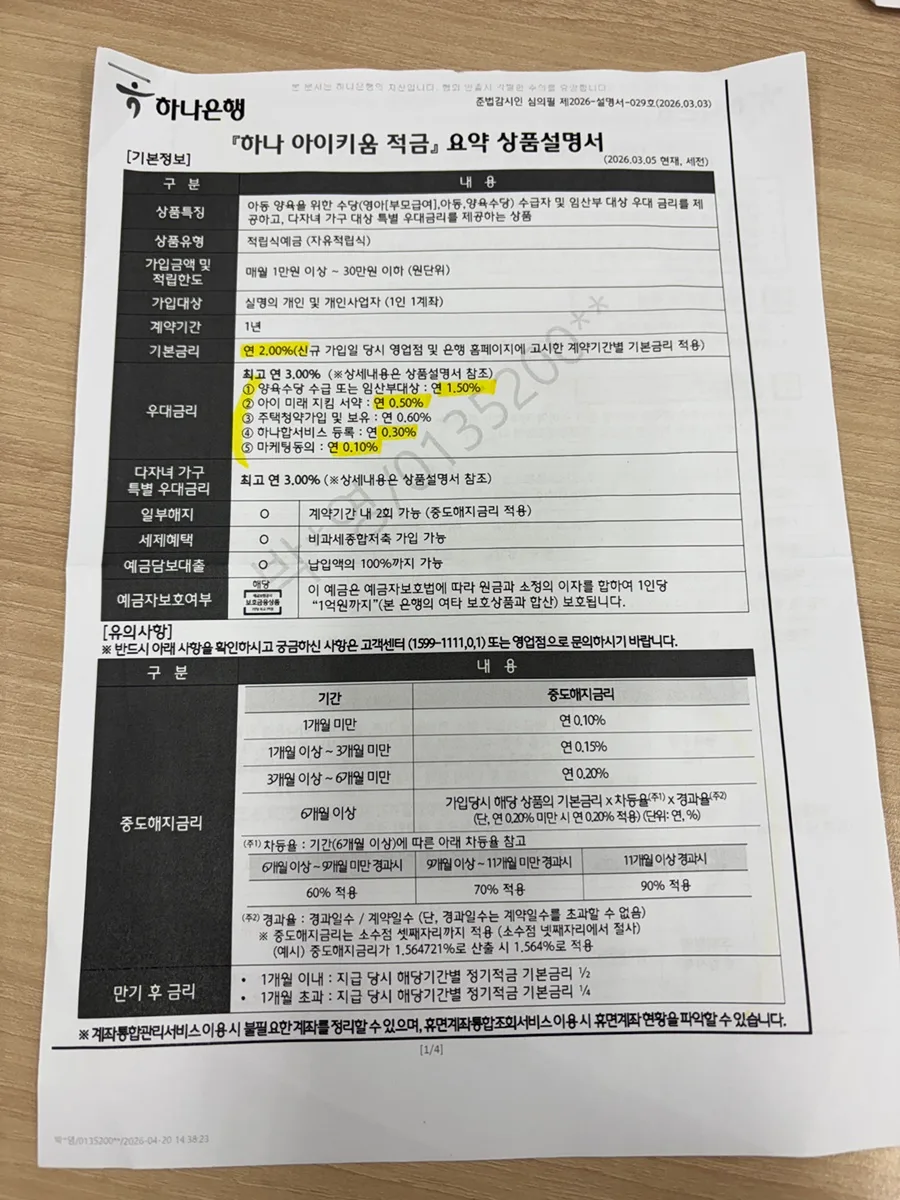

In a financial climate where general savings account interest rates are often modest, Hana Bank's 'I-Kium' savings account stands out by offering a significant preferential rate for expectant mothers. This account combines a base interest rate with additional benefits for those who are pregnant or planning to start a family, potentially reaching an annual yield of 5%. The author personally experienced this, securing a 4.4% rate due to holding a separate housing subscription account (a common savings vehicle in Korea, similar to a dedicated home savings plan in the US). They confirmed that meeting all conditions could indeed lead to a 5% annual return. Therefore, for individuals who are pregnant or planning for childbirth, it's crucial to thoroughly review your personal eligibility and the specific preferential rate conditions to maximize your interest earnings. This savings account can be opened as either a flexible or fixed deposit account with a 12-month term, allowing for monthly contributions up to approximately $220-$250 USD (₩300,000 KRW), making it suitable for those looking to steadily build a nest egg over a short period.

Who is Eligible for the 'I-Kium' Savings Account and What Are the Conditions?

The 'I-Kium' savings account is open to all customers, including expectant mothers, but achieving the highest interest rates requires meeting specific criteria. While the base rate is accessible to everyone, the preferential 5% annual yield is tied to conditions such as being pregnant or fulfilling other bonus requirements. For example, holding a Korean housing subscription account (청약통장) can impact the final interest rate, as it did for the author, potentially reducing the rate slightly if not structured correctly for maximum benefit. It's essential to consult with a Hana Bank representative to understand how your individual financial situation, including existing accounts or specific life events, affects your eligibility for the highest rates. The account term is 12 months, and monthly deposits can be made flexibly or as a fixed amount, capped at around $250 USD (₩300,000 KRW) per month. This structure is ideal for short-term savings goals, such as preparing for the expenses associated with a new child.

What Are the Key Differences Between 'I-Kium' and Other Savings Accounts?

The primary distinction of the 'I-Kium' savings account lies in its targeted preferential interest rates, particularly for expectant mothers, offering a higher yield than many standard savings or fixed deposit accounts. While typical US savings accounts might offer APYs between 4-5% currently, the 'I-Kium' aims to provide a competitive edge through its bonus structure. For instance, a standard savings account might offer a flat rate, whereas 'I-Kium' provides a tiered approach. The author's experience highlights that holding a Korean housing subscription account, a product not common in the US, can influence the final rate. This Korean product is designed to encourage consistent saving for family-related expenses, offering a tangible benefit for a specific demographic. The account term is fixed at 12 months, with monthly deposit limits around $250 USD (₩300,000 KRW), making it a focused savings tool rather than a flexible, long-term investment.

What Should You Consider Before Opening the 'I-Kium' Savings Account?

Before opening the 'I-Kium' savings account, it's crucial to verify the exact preferential interest rates applicable to your specific situation. The maximum 5% annual rate is contingent upon meeting certain conditions, and it's vital to consult with a Hana Bank representative to confirm your eligibility. Factors such as holding other financial products, like a housing subscription account (청약통장), could potentially affect the final rate applied, as seen in the author's case where it resulted in a 4.4% rate instead of the full 5%. It's also important to note that this is a 12-month term account, and while it offers benefits for maintaining the balance until maturity, early withdrawal may result in a lower interest rate or incur taxes. Therefore, it's advisable to use funds you won't need access to for the full year. While this account presents a great opportunity for those expecting a child to save effectively, thorough pre-application checks are essential. For personalized financial advice, consulting with a financial advisor is recommended, as individual circumstances can vary significantly.

For more details, check the original source below.