Purchasing a home for $500,000 at market price in 2026 might seem straightforward, but unexpected closing costs, renovation expenses, and other fees can make it a financial pitfall. Understanding and securing a 'safety margin' is crucial to navigate these risks and ensure a sound investment.

What Are the Hidden Costs of Buying a $500K Home?

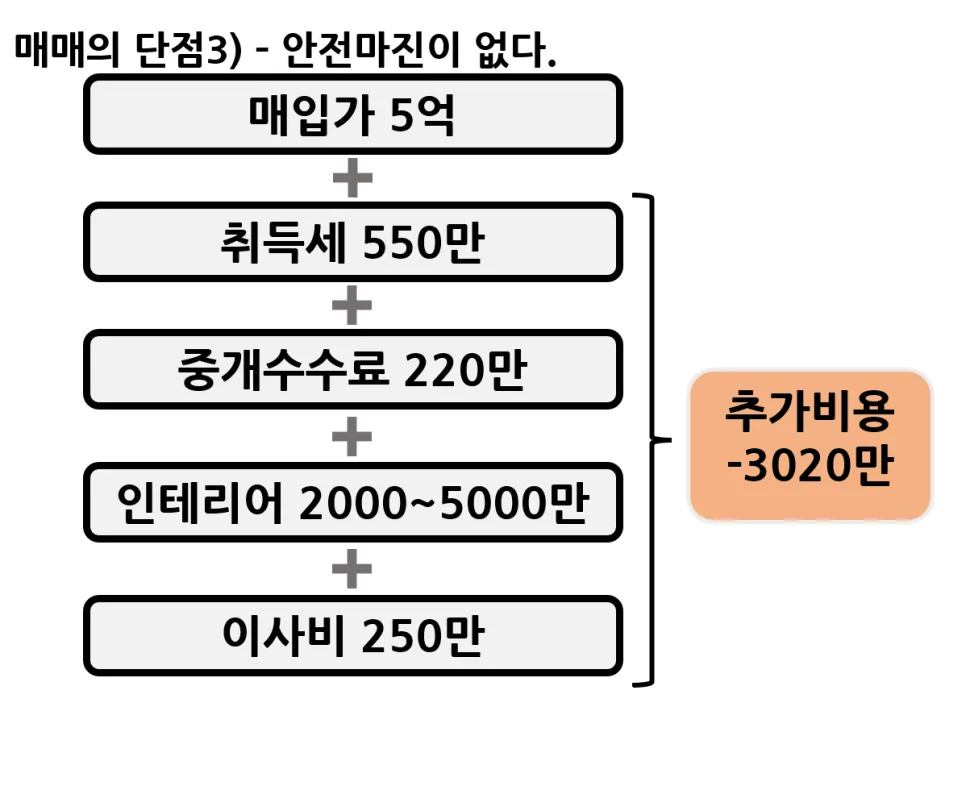

Beyond the sticker price of $500,000, several mandatory expenses add up significantly. In the US, these include closing costs such as title insurance, appraisal fees, loan origination fees, and recording fees, which can range from 2% to 5% of the loan amount. For a $500K home, this could mean an additional $10,000 to $25,000. Property taxes, which vary by state and locality, will also be an ongoing expense. If you're buying an older home, expect renovation costs to add anywhere from $20,000 to $50,000 or more for essential updates. Moving expenses can easily add another $1,000 to $3,000. Factoring in these essential costs, you could be looking at an additional $30,000 to $80,000+ on top of the purchase price, representing about 6% to 16% of the home's value.

How Is the Real Loss Calculated When Home Prices Drop?

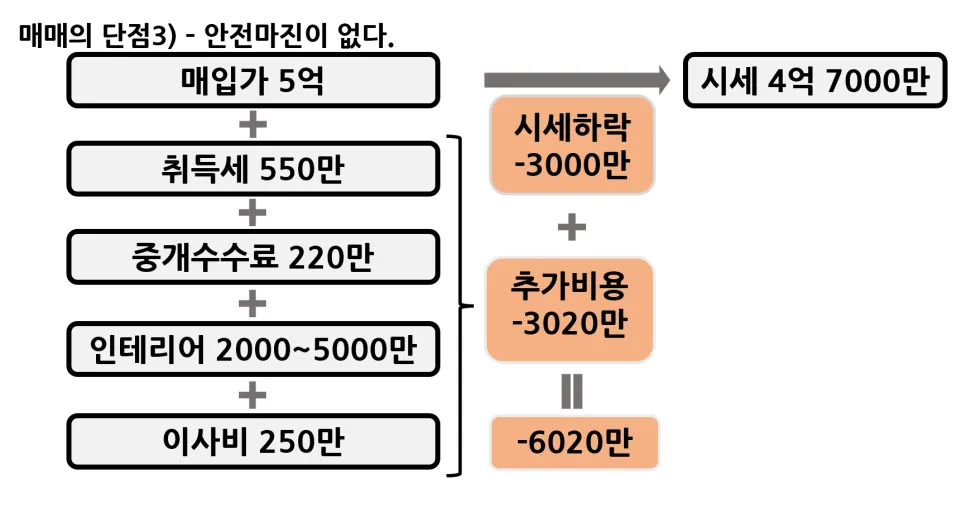

When home prices decline, your actual financial loss is amplified by the initial expenses incurred. For instance, if you purchase a $500,000 home and its market value drops by $30,000 to $470,000, your immediate paper loss is $30,000. However, your true financial deficit includes the closing costs and renovation expenses you've already paid. If those initial costs amounted to $30,000, your total real loss becomes $60,000 ($30,000 market drop + $30,000 initial expenses). This substantial loss can significantly impact your net worth, especially if you need to sell the property in a down market. It underscores the importance of calculating your break-even point, considering all upfront expenditures.

What Strategies Can Secure a Safety Margin When Buying Property?

Buying a property at market value leaves you vulnerable to market downturns and personal financial emergencies. To mitigate this, securing a 'safety margin' is essential. This means acquiring the asset for less than its current market value, effectively locking in an immediate profit or buffer. In the US real estate market, this can be achieved by actively seeking out distressed properties, foreclosures, or motivated sellers willing to accept lower offers. Learning to analyze auction properties or negotiating aggressively on fixer-uppers can help you acquire a home at 10-15% below market value. This margin acts as a crucial cushion against market volatility and unexpected expenses.

What Is a Must-Check Checklist Before Buying a Home?

Before committing to a home purchase, a thorough checklist is vital for a successful transaction. First, ensure you have sufficient funds for all anticipated closing costs, including taxes, fees, and moving expenses, typically around 6-16% of the purchase price. Obtain detailed renovation quotes and budget accordingly, especially for older properties. Assess your financial resilience: can your household budget absorb a 10% drop in home value or a 1-2% increase in mortgage interest rates without severe strain? Research methods for acquiring property below market value, such as understanding local auction dynamics or identifying off-market deals. Finally, confirm your ability to manage increased mortgage payments if interest rates rise, ensuring long-term financial stability and avoiding potential foreclosure.

For more details, check the original source below.