Unlock your financial potential with a 5-step wealth-building plan designed for individuals aged 36-56, aiming to reach $1 million by age 60. The next 5-8 years represent a critical window for accumulating significant assets, and this guide provides actionable strategies to achieve financial freedom.

Why is the 36-56 Age Range the 'Golden Time' for Wealth Building?

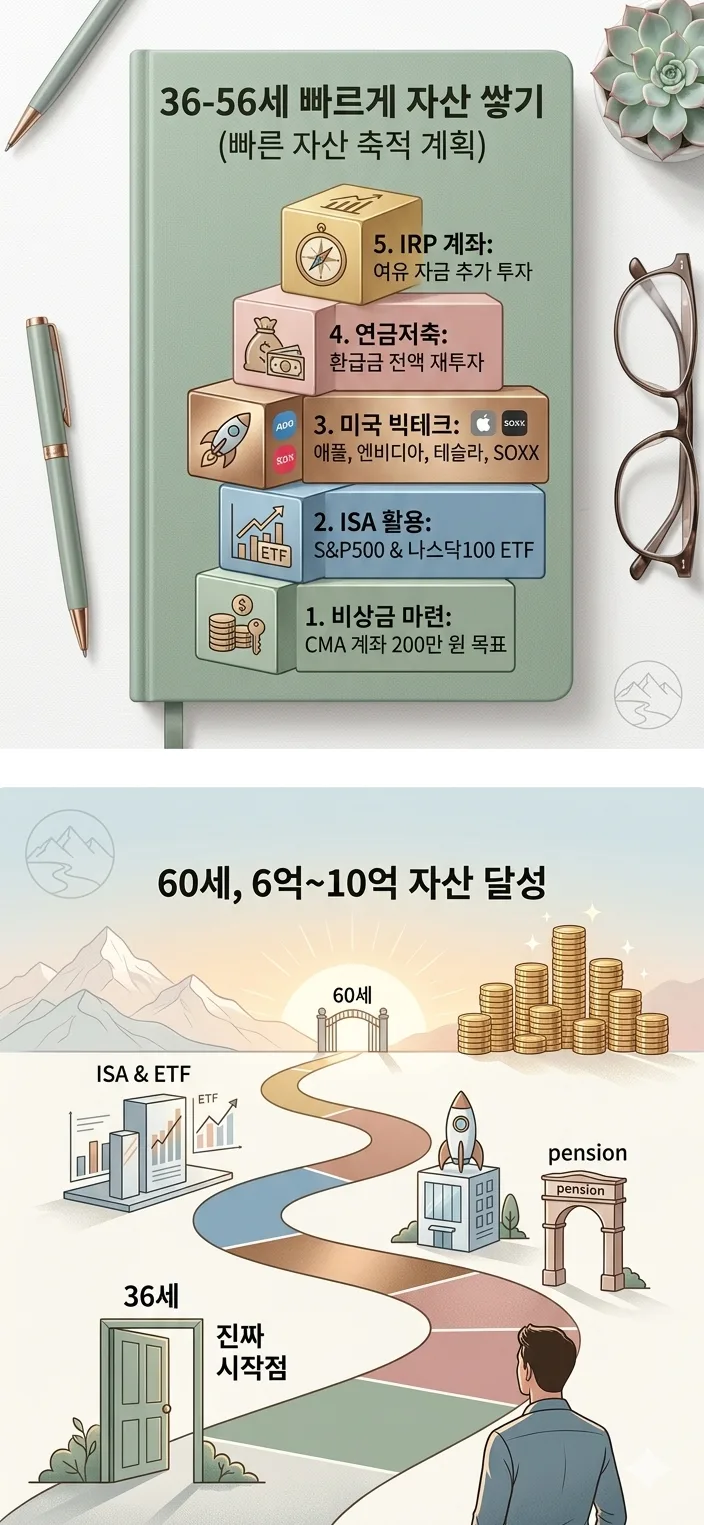

The period from your mid-30s to mid-50s is widely recognized as the prime time for substantial wealth accumulation. This phase, often called the 'golden time,' offers a crucial opportunity to build a strong financial future. By implementing effective wealth management strategies now, you can realistically aim for $600,000 to $1 million by the time you turn 60. This guide simplifies complex financial planning into five actionable steps, empowering you to start building your wealth today. Even a small step, like setting up an emergency fund, can lead to significant future financial security.

How Much Should Your Emergency Fund Be, and How Do You Build It?

The first step in any solid financial plan is establishing a robust safety net. We recommend setting an emergency fund goal of $2,000 (approximately ₩200 만원). Aim to save $150 (approximately ₩15 만원) monthly into a Cash Management Account (CMA). CMA accounts typically offer higher interest rates than standard savings accounts and provide easy access to your funds, making them ideal for emergency savings. Once you reach your $2,000 target, it's wise to shift your focus from merely increasing your emergency fund to prioritizing investment for long-term asset growth.

How to Maximize Tax Benefits with an ISA Account for Short-Term Investments?

If you have short-term investment goals within a 3-5 year timeframe, an Individual Savings Account (ISA) is an excellent tool. In Korea, ISAs allow you to manage various financial products like savings, funds, ETFs, and stocks within a single account, offering tax benefits on your earnings. Consider investing $500 (approximately ₩50 만원) monthly into index-tracking ETFs such as those following the S&P 500 or Nasdaq 100. A key advantage of ISAs is the ability to roll over matured funds into a pension savings account every three years, extending tax benefits and supporting long-term financial planning.

What Are the Principles for Constructing a Long-Term Growth Portfolio?

For stable asset growth over a decade or more, focus on investing in high-quality assets that lead the market. Consider assets with strong growth potential, particularly in the U.S. market, such as leading tech companies or ETFs tracking long-term growth sectors. A strategy of investing $450 (approximately ₩45 만원) monthly into top-tier U.S. stocks like Apple, Nvidia, or Tesla, or into tech-focused ETFs like QQQ or SOXX, can yield significant long-term returns. This diversified approach helps mitigate market volatility and enhances potential growth.

How to Maximize Compound Interest with Pension Savings and IRP Accounts?

Pension savings accounts are crucial for retirement planning, offering significant tax benefits. Contributing $150 (approximately ₩15 만원) monthly can provide tax credits during your annual tax filing. It's vital to reinvest any tax refunds received from these contributions to maximize the power of compound interest. Reinvested funds grow exponentially over time, significantly boosting your asset accumulation. If you've maxed out your pension savings contributions, consider an Individual Retirement Pension (IRP) account for additional asset growth opportunities, especially if you've exceeded the standard pension savings limit.

For more details, check the original source below.