Korea's National Growth Fund for 2026 offers a unique investment opportunity with up to 20% principal loss protection covered by the government and significant tax deductions of up to ₩18 million (approx. $13,000 USD). This guide breaks down the essential details for US investors interested in this government-backed financial product.

Why is Korea's National Growth Fund Gaining Attention?

Amidst rising inflation, interest in smart financial planning is surging, and the newly launched National Growth Fund by the Korean government is capturing significant attention. What makes this fund stand out is the government's commitment to covering up to 20% of any investment principal loss. This dramatically reduces the risk for investors, especially those hesitant about traditional stock or general fund investments. Furthermore, it provides substantial tax benefits, including annual income deductions of up to ₩18 million (approx. $13,000 USD) and separate taxation on dividend income, which can significantly ease the burden during year-end tax settlements. A portion of the total fund offering is specifically allocated for lower-income individuals, presenting a more favorable opportunity for those meeting certain income criteria.

How to Invest in Korea's National Growth Fund and Key Dates

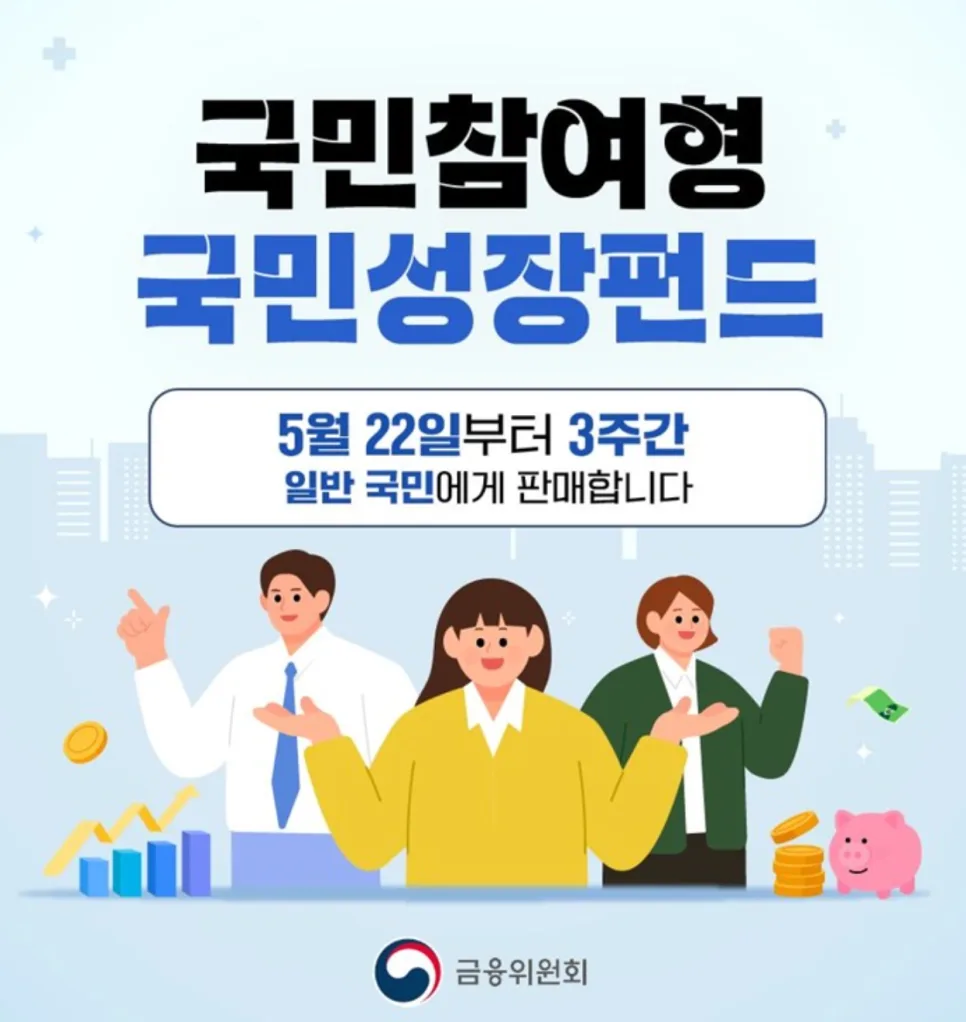

The National Growth Fund will be open for subscriptions for three weeks starting May 22, 2026. However, with a total fund limit of ₩600 billion (approx. $440 million USD), early closure is possible, making prompt action advisable for interested investors. Investment can be made through major Korean banks like Kookmin, Shinhan, and Woori, as well as securities firms such as Mirae Asset and KB Securities, via both online and offline channels. For those employed, mobile apps offer a convenient way to invest during breaks. To claim the tax benefits, you'll need to submit a 'Proof of Income (for ISA Subscription)' certificate, obtainable through the Korean tax authority's online portal (Hometax). Preparing this document in advance is crucial for verifying eligibility.

Crucial Considerations Before Investing in the National Growth Fund

Despite its attractive benefits, the National Growth Fund has specific conditions that require careful consideration. The most critical point is the inability to redeem funds for five years; it functions much like a fixed-term deposit. While the fund may be listed on an exchange for trading, selling it at its full value in the open market could be challenging. Consequently, this fund is not suitable for individuals who require access to their funds within one to two years for purposes like security deposits for housing or immediate living expenses. It is strongly recommended for investors who can commit their capital for a minimum of five years and have surplus funds available.

Pros and Cons of the National Growth Fund

The primary advantages of the National Growth Fund are the government's principal loss protection (up to 20%) and the substantial income deduction (up to ₩18 million, approx. $13,000 USD) coupled with separate dividend income taxation. These features enhance investment security and reduce tax liabilities, making it ideal for investors seeking both stability and tax efficiency. Investing in government-backed initiatives focused on advanced industries also presents potential for long-term growth. However, the significant drawback is the mandatory five-year lock-in period, which limits liquidity. If funds are needed unexpectedly, early withdrawal is not an option, posing a constraint for those with short-term financial needs. Therefore, a thorough assessment of one's investment profile and financial plan is essential before committing.

Common Mistakes When Investing in the National Growth Fund

A frequent error investors make is overlooking the mandatory five-year lock-in period. Focusing solely on the tax benefits or principal protection, they may not fully grasp that their funds will be inaccessible for half a decade. This can lead to difficulties if unforeseen financial needs arise. Another common mistake, particularly with the 'low-income' or 'subsidized' portions of the fund, is failing to accurately verify income requirements, resulting in disqualification. It is vital to meticulously review all terms and conditions, assess your personal income situation, and confirm your five-year financial plan before applying. Consulting with a financial advisor can help ensure this investment aligns with your individual circumstances.

For more details on the National Growth Fund, check the original source below.