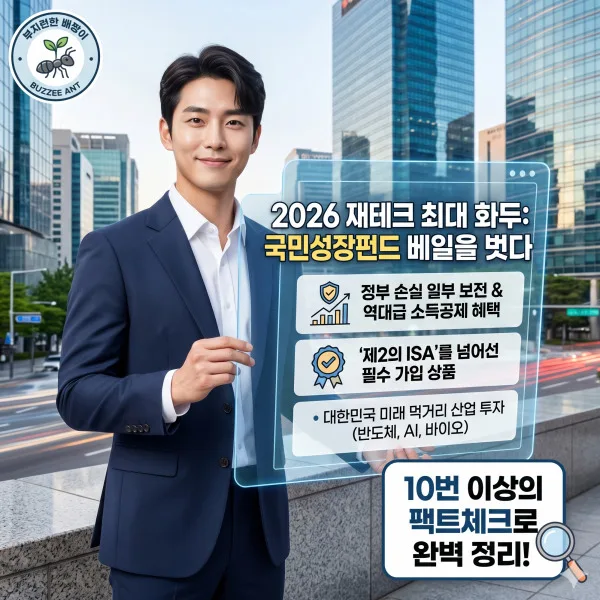

The 2026 National Growth Fund (Gukmin Seongjang Fund) offers a significant tax deduction of up to $18,000 for year-end tax settlements in Korea. This government-backed initiative invests in future industries like AI, semiconductors, and biotech, while providing loss protection for investors, making it a compelling financial product for 2026.

What is Korea's National Growth Fund and Why is it a Hot Topic for 2026?

Launching officially on May 22, 2026, the National Growth Fund is a policy-driven investment fund initiated by the Korean government. With a planned scale of 15 trillion KRW (approximately $11 billion USD) over five years, it aims to foster key future industries such as AI, semiconductors, and biotechnology. A standout feature is the government's subordinate investment, which offers investors loss protection of up to 20% of their investment. This fund is positioned not just as a financial product, but as an opportunity to grow assets while contributing to the nation's future industrial landscape. Many financial experts are recommending it as a must-have investment, potentially surpassing the appeal of existing savings accounts like the ISA (Individual Savings Account).

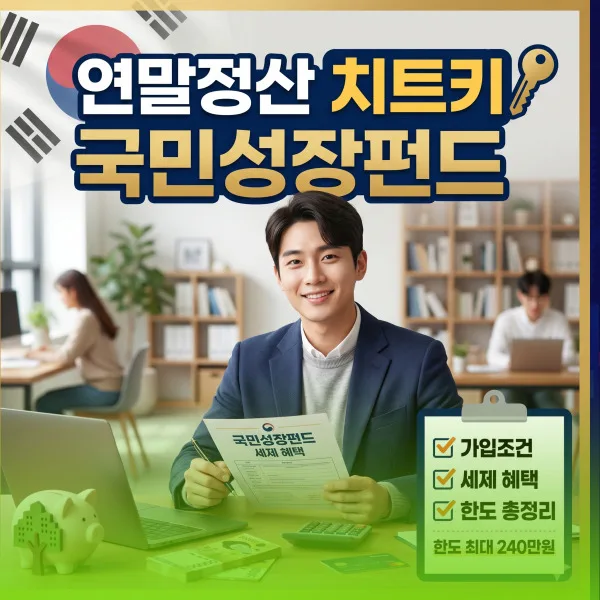

What Are the Eligibility Requirements and Contribution Limits for the National Growth Fund?

The National Growth Fund is designed for broad accessibility, open to all Korean residents aged 19 and over, including workers aged 15 and above. Individuals can contribute up to 100 million KRW (approximately $75,000 USD) annually, with a lifetime limit of 200 million KRW (approximately $150,000 USD) over five years. To fully benefit from the tax incentives, investments must be held for at least three years, with the most substantial benefits realized after a five-year term. Applications can be made at major commercial banks and securities firms, both online and in person. It's crucial to open a dedicated tax-incentivized account for this fund.

What Are the Top 5 Tax Benefits of the National Growth Fund for Year-End Settlements?

The National Growth Fund is generating buzz due to its exceptional tax benefits. Firstly, it offers progressive income tax deductions: 40% on investments up to 30 million KRW (approx. $22,500 USD), 20% on amounts between 30-50 million KRW (approx. $22,500-$37,500 USD), and 10% on amounts between 50-70 million KRW (approx. $37,500-$52,500 USD), potentially yielding a maximum deduction of 18 million KRW (approx. $13,500 USD). Secondly, dividends from the fund are taxed at a preferential rate of 9.9%, lower than the standard 15.4% rate. Thirdly, the government's subordinate investment offers up to 20% loss protection. Fourthly, individuals subject to comprehensive income tax can invest without increasing their tax burden. Finally, it allows for loss offsetting against gains from other stock-type funds, further reducing the overall tax liability.

What Industries Does the National Growth Fund Invest In, and What Are the Expected Returns?

The National Growth Fund strategically invests in industries poised for future growth in Korea. Significant capital is allocated to AI (Artificial Intelligence), advanced manufacturing and semiconductors, and the bio/vaccine infrastructure sectors. The fund's sub-funds, managed by private experts, aim to generate returns through equity investments in promising companies and financing for facility expansions. Given the government's focus on nurturing these strategic industries, the fund targets returns exceeding market averages over the long term. The government's loss protection mechanism also enhances its stability, making it an attractive option for steady, long-term asset growth.

What Should Investors Be Aware of Regarding the National Growth Fund's Investment Terms and Redemption Conditions?

It's crucial to understand that the National Growth Fund is primarily a 'non-redeemable' fund. This means investors generally cannot withdraw their funds before the maturity date, which is set at a minimum of three years and ideally five years. Therefore, it's essential to invest only with funds you can commit for the long term, typically three to five years. The total management fee is approximately 1.0% to 1.2% annually, with potential savings if subscribed to online (e-class) versions. Due to the specific nature of this investment and its tax implications, consulting with a financial advisor is highly recommended to ensure it aligns with your personal financial situation and investment goals.

English crawl path

Next English reads from this pilot cluster

Continue through the category hub, latest English stories, and related posts so this translated article is not an isolated URL.

Tags

💬Frequently Asked Questions

What should I check first in Korea's Growth Fund 2026: Max $18K Tax Deduction Guide?

Does this Finance article link back to the Korean source?

Where can I find similar English stories?

English discovery path

Explore more English K-culture stories

Keep browsing the indexed English pilot cluster so Google and readers can move between this story, the category hub, and fresh discovery pages.

Original Source

Read the Korean original