Choosing between term life insurance and whole life insurance in 2026 depends heavily on your personal financial situation, family plans, and future goals. For single individuals under 30, affordable term life insurance is often recommended. However, if you have dependents or significant debt like a mortgage, whole life insurance might offer better long-term family financial security.

What's the Core Difference Between Term and Whole Life Insurance?

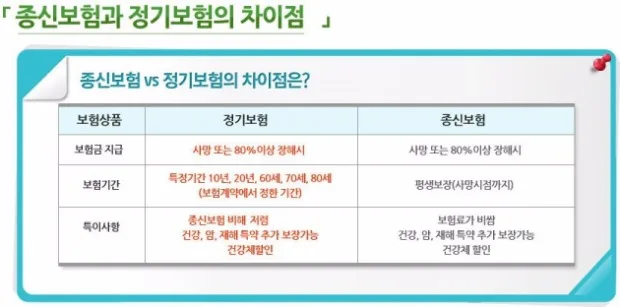

The primary distinction between term life insurance and whole life insurance lies in their coverage duration. Term life insurance provides coverage for a specified period, such as 20 or 30 years, while whole life insurance offers lifelong coverage, paying out whenever the insured event occurs. For example, a 20-year term policy pays a death benefit if you pass away within those 20 years. Whole life, conversely, guarantees a payout regardless of when death occurs. This difference in coverage directly impacts premiums; term life is generally more affordable due to its limited term, whereas whole life policies are more expensive because they offer permanent protection. For young adults just starting their careers, term life can be an attractive option, providing solid coverage for a set period at a manageable cost, allowing them to focus on other financial priorities like saving or investing.

When Is Term Life Insurance a Better Choice for Young Adults?

Term life insurance is particularly beneficial for young adults who are not yet financially established. Its main advantage is its affordability. Because coverage is limited to a specific term, the premiums are significantly lower than those for whole life insurance. This makes it an excellent option for young professionals who need to prioritize saving for a down payment, investing, or paying off student loans. For instance, a 20- or 30-year term policy can provide crucial coverage during the years you're raising children or paying off a mortgage. However, a key drawback is that coverage ends once the term expires. If you still need coverage later in life, you might face higher premiums or be unable to qualify due to age or health changes. Some term policies offer a return of premium option, where you get your premiums back if you outlive the term, but these often come with higher costs and may not fully recoup your investment after fees.

When Should You Consider Whole Life Insurance?

Whole life insurance offers lifelong coverage, acting as a safety net for your beneficiaries, covering expenses like final costs, outstanding debts, or providing ongoing financial support. For individuals who are married, have children, or hold significant debts such as a mortgage, whole life insurance can be a crucial tool to ensure their family's financial stability after their passing. Some whole life policies also include features like cash value accumulation, which can be borrowed against or used for future needs, and can even be converted into a retirement income stream. However, whole life insurance comes with higher premiums compared to term life. For young adults, the initial cost can be a significant burden. It's crucial to ensure that the premium payments fit comfortably within your current budget. If the cost is prohibitive, a strategy could be to start with a robust term policy and consider converting it to a whole life policy later as your income grows and financial responsibilities increase.

What Factors Should Young Adults Consider When Choosing Life Insurance?

When selecting life insurance as a young adult, it's essential to conduct a thorough assessment of your personal circumstances and future aspirations. If you're under 30, single, and have no dependents, term life insurance is often the most practical choice, offering affordable coverage for a defined period. This allows you to manage your finances effectively while still having protection. Conversely, if you have family responsibilities, such as supporting children or a spouse, or if you have substantial debts like a mortgage, whole life insurance might be a more suitable option to guarantee long-term financial security for your loved ones. A critical consideration is your ability to afford the premiums. Committing to overly expensive coverage can strain your budget and hinder other financial goals. It's wise to choose a policy with premiums that align with your income. Adjusting the coverage amount or term length can also help manage costs. Consulting with a financial advisor can provide personalized guidance to help you select the best policy for your unique situation.

What Are the Essential Things to Check Before Buying Life Insurance?

Regardless of the type of life insurance you choose, it's crucial to meticulously review several key details before finalizing your policy. First, understand the contestability period (often 1-2 years), during which the insurer can investigate claims more thoroughly and potentially deny coverage if material misrepresentations were made on the application. Second, check for any waiver of premium or paid-up additions riders, which can offer additional benefits or flexibility. Third, if you opt for a renewable term policy, carefully examine the renewal terms; premiums typically increase significantly upon renewal. Finally, scrutinize the scope of coverage. Ensure you understand exactly what causes of death are covered and if there are any exclusions, such as for high-risk activities or pre-existing conditions. Thoroughly understanding these specifics will help prevent future disputes and ensure your policy meets your needs.

For more details, check the original source below.