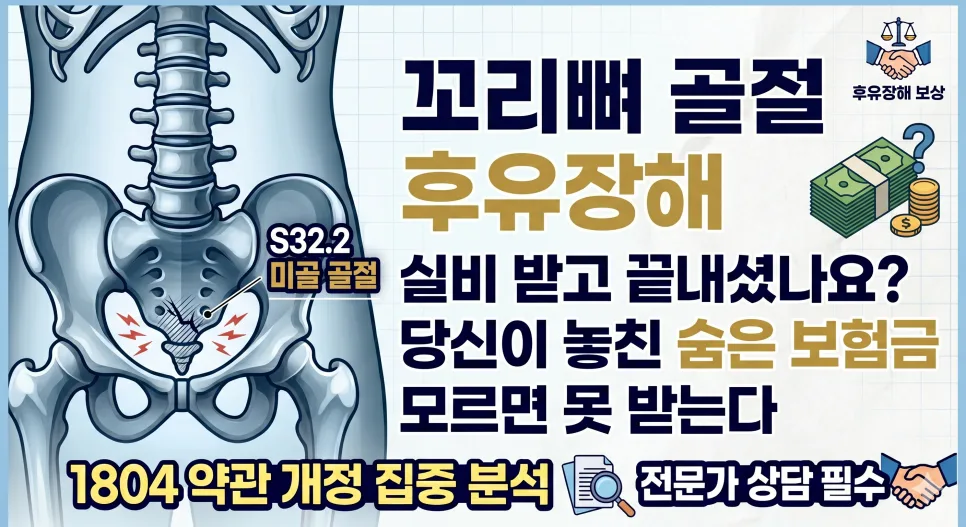

If you were insured before April 2018, you can claim up to 15% in permanent disability compensation for a tailbone fracture, even without surgery. This guide details defense strategies against insurer denials and evaluation standards. This is not financial advice. Consult a licensed financial advisor.

What Are the 2018 Pre-Policy Standards for Tailbone Fracture Disability?

Tailbone (coccyx) fractures are common from falls on ice or hard surfaces, but often treated conservatively, leading people to overlook potential disability compensation. For insurance policies purchased before April 2018, older terms often classified the coccyx as part of the spine. This allowed claims to be evaluated under 'spinal deformity' standards, potentially offering payouts of 15% for minor deformities or up to 30% for significant spinal deformities. Even without surgical intervention, if imaging evidence shows displacement or malunion leading to a visible deformity, you are generally eligible to claim a minimum of 15% compensation. These older policies provide a more favorable framework for tailbone fracture disability claims.

What Are Insurer Denial Tactics for Tailbone Fractures, and How to Counter Them?

Insurers often deny or reduce tailbone fracture disability claims using three main arguments. First, they may claim the sacrococcygeal joint has physiological non-union or degenerative changes, arguing the deformity isn't accident-related. To counter this, secure clear 'acute fracture' findings from immediate post-accident imaging and, if necessary, present comparative imaging showing changes over time to prove causation. Second, they might argue the coccyx isn't a primary weight-bearing spinal structure and thus doesn't cause permanent disability. Legally, if the policy terms classify the coccyx under spinal categories, arguing functional differences to reduce benefits violates the principle of interpreting policy terms against the insurer. Third, they may deny claims if surgery wasn't performed. However, policy interpretation prioritizes the existence of a disability over the method of treatment, making proof of deformity through imaging crucial. Effectively defending against these tactics requires thorough preparation and expert assistance.

How Are Tailbone Fracture Disabilities Evaluated in Liability and Auto Insurance Cases?

Calculating compensation for tailbone fractures resulting from liability or auto insurance incidents is more complex. Standard liability assessments, like the McBride Disability Rating Scale, lack a specific category for the coccyx, leading insurers to deny claims for loss of earning capacity. Practically, legal precedents often allow for indirect application of pelvic bone deformity standards or using the National Compensation Act's disability grades for deformities to increase the assessed damages. Furthermore, strategies to secure substantial compensation for pain and suffering, future medical costs, and related expenses like chronic pain from sitting (coccydynia) are essential. Because the applicable laws and evaluation criteria differ based on the incident's nature, a specialized review of your specific case is necessary.

What Are Key Considerations When Filing a Tailbone Fracture Disability Claim?

Successfully claiming tailbone fracture disability benefits involves more than just a medical diagnosis. By the time you reach the disability assessment stage (typically six months post-injury), your primary physician might hesitate to provide a diagnosis that aligns with policy standards or may be influenced by the insurer's medical consultations, potentially jeopardizing your rightful compensation. To effectively counter the insurer's complex reduction arguments, meticulously analyze subtle clues in imaging reports from the outset and clearly understand the advantages of pre- and post-policy revision terms. Crucially, confirm your policy's effective date to leverage the more favorable terms available before April 2018. Given that compensation outcomes vary significantly based on individual circumstances, consulting with a professional is the wisest approach to ensure your rights are protected.

For detailed consultation, please contact an expert.