Navigating the Shindongtan Foret Xi real estate market in 2026 requires understanding new loan regulations, especially when purchasing a unit with an existing tenant. This expert analysis breaks down how to handle the final payment (잔금 처리) and crucial considerations for buyers, particularly those planning to occupy the unit themselves. Secure your cash flow strategy and occupancy timeline effectively.

What Are the 2026 Mortgage Loan Regulations After June 27th?

Effective June 27, 2026, new household debt management measures will impact the Korean real estate market, particularly in the Seoul metropolitan area. The core change is a standardized mortgage loan limit of up to ₩600 million (approximately $450,000 USD) for home purchases in regulated zones, regardless of the property's price or the borrower's income. This applies to loans for purchasing homes. Furthermore, obtaining a mortgage for a second home purchase is now completely prohibited for individuals who already own multiple properties. For existing homeowners looking to purchase an additional property, there's a strict requirement to sell their current home within six months of the new purchase. Failure to comply with the mandatory residency requirement (moving into the property within six months of loan disbursement) can lead to the recall of the loan and a three-year restriction on future mortgage applications. Loans for living expenses (생활 안정자금) are capped at ₩100 million (approx. $75,000 USD), and 'gap investment' (갭 투자) is being curtailed through a ban on jeonse (lump-sum deposit) loans tied to ownership transfer. The stress debt-to-income (DSR) ratio floor has also been raised to 3% in regulated areas, tightening lending conditions overall.

How to Handle Final Payment for Shindongtan Foret Xi Units with Existing Tenants?

Related Articles

Shindongtan Foret Xi is located in Hwaseong City, Gyeonggi Province, which falls under the Seoul metropolitan area's influence and is subject to these new regulations. If a unit is currently occupied by a tenant who has registered their residency, the new buyer cannot register their own residency there during the tenancy. This directly conflicts with the requirement to establish residency within six months (practically, within three months) when obtaining a mortgage for properties in regulated areas. Consequently, when purchasing a Shindongtan Foret Xi unit with an existing tenant, buyers must assume the tenant's existing lease deposit (보증금) and pay the remaining balance of the purchase price entirely in cash. Utilizing a mortgage for the final payment in such scenarios is practically impossible due to the residency restrictions. This means buyers need substantial liquid assets readily available, a direct consequence of the tightened lending rules effective from June 27, 2026.

What Are the Features and Caveats of Recommended Shindongtan Foret Xi Units?

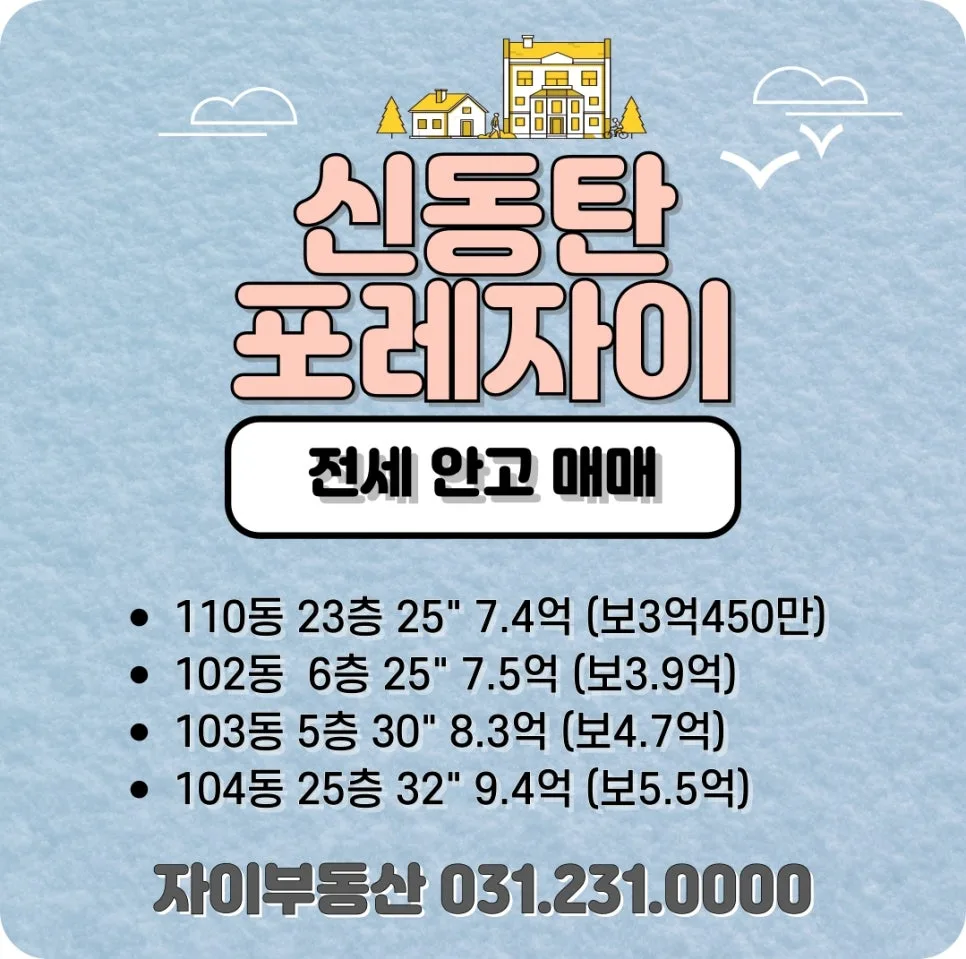

The KB real estate appraisal for Shindongtan Foret Xi indicates a median price of approximately ₩740 million (around $555,000 USD) for a 25-pyeong unit (approx. 825 sq ft), ₩840 million (approx. $630,000 USD) for a 30-pyeong unit (approx. 990 sq ft), and ₩900 million (approx. $675,000 USD) for a 32-pyeong unit (approx. 1056 sq ft). Recent actual sales prices may be slightly higher. For instance, unit 110-2301 (25-pyeong) is listed at ₩740 million ($555,000 USD) and offers the open views characteristic of top-floor units. However, be aware that top floors can experience higher cooling costs in the summer due to radiant heat. Unit 102-601 (25-pyeong) at ₩750 million ($562,500 USD) boasts excellent access to schools and the complex's amenities, ideal for families with young children. Its availability is two months before the lease ends, requiring careful timing for the final payment to ensure self-occupancy. Unit 103-501 (30-pyeong) is priced at ₩830 million ($622,500 USD) and includes premium interior upgrades. However, the tenant's move-out date needs coordination, meaning the occupancy date isn't fixed, which is a crucial point to note. Lastly, unit 104-2501 (32-pyeong, Type B) is listed at ₩940 million ($705,000 USD) with panoramic views, but the current tenant's lease extends until February 2028, requiring a significant waiting period before self-occupancy. The purchase price relative to the current lease deposit also needs careful evaluation.

What Are the Downsides of Top-Floor Units During Summer?

Top-floor units, while often prized for their expansive views and sense of privacy, come with a distinct drawback during the hot summer months: increased cooling costs. Due to direct exposure to sunlight and heat absorption through the roof, these units can become significantly warmer than lower floors. This necessitates more frequent and intensive use of air conditioning systems, leading to higher electricity bills. While the enhanced natural light and unobstructed vistas are appealing, potential buyers should factor in these increased operational expenses when evaluating a top-floor property, especially in warmer climates or during peak summer seasons. This is a common consideration for penthouse or top-tier apartment living across many markets.

How Do the New Regulations Prevent 'Gap Investment'?

The recent regulations specifically target 'gap investment' (갭 투자), a strategy where investors purchase property by leveraging a large portion of the tenant's security deposit (jeonse) to cover the price difference, often with minimal personal capital. By banning jeonse loans that are conditional on ownership transfer and tightening overall mortgage availability, the government aims to curb speculative investment. This forces investors to rely more on their own capital or traditional mortgages, making it harder to finance purchases solely through tenant deposits. The goal is to stabilize the market by reducing the number of purely speculative transactions and ensuring that property ownership is backed by more substantial financial commitment, thereby preventing asset bubbles and promoting genuine homeownership.

For more details, check the original source below.