For US investors considering Korean market opportunities, the Korean Growth Fund in 2026 offers significant tax deductions (up to 40%), a 20% loss offset by government funds, and a special 9.9% dividend tax rate. However, be aware of the mandatory 5-year lock-up period and a relatively high management fee of 1.2%.

Who Benefits Most from the Korean Growth Fund in 2026?

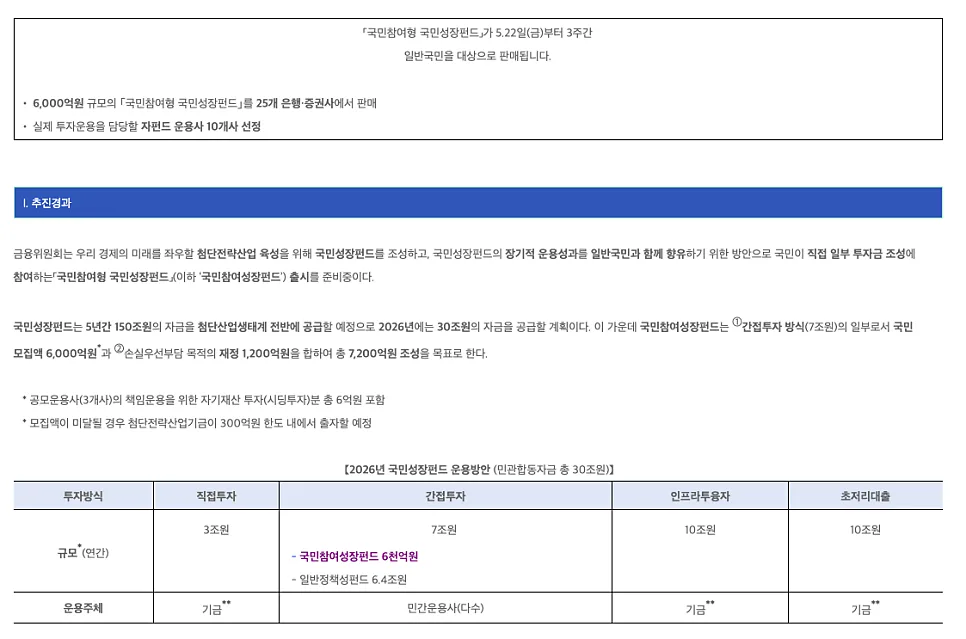

The Korean Growth Fund is a policy-driven investment vehicle, backed by the Korean government, aimed at fostering growth in key industries like biotech, semiconductors, and AI, with a particular focus on small and medium-sized enterprises listed on the KOSDAQ. For 2026, the fund plans to raise 600 billion KRW (approximately $450 million USD) from the public, with an individual investment limit of 100 million KRW (around $75,000 USD). Unlike investments in established KOSPI stocks, this fund targets the KOSDAQ and venture capital sectors, aligning with national economic development goals. High-income earners in Korea, particularly those in higher tax brackets, stand to gain the most. For instance, an individual with a taxable income exceeding 88 million KRW (approx. $66,000 USD), placing them in the 35% tax bracket, could see a tax savings of approximately 4.32 million KRW (around $3,200 USD) on a 70 million KRW (approx. $52,000 USD) investment. This substantial tax deduction makes the fund an attractive option for those with disposable income and a long-term investment horizon.

Understanding the 20% Loss Offset and 9.9% Dividend Tax Benefit

Related Articles

A key feature of the Korean Growth Fund is its risk mitigation mechanism. The fund is structured with 600 billion KRW (approx. $450 million USD) in capital, supplemented by an additional 120 billion KRW (approx. $90 million USD) from government funds acting as a subordinated layer. In the event of fund losses, these government funds absorb the initial impact, effectively providing a safety net that covers up to 20% of the invested principal. This is particularly reassuring given the inherent volatility associated with investing in KOSDAQ and venture companies. Furthermore, dividends generated from investments within the fund, when held in a dedicated Korean Growth Fund account, are taxed at a preferential rate of 9.9%, significantly lower than the standard 15.4% capital gains tax in Korea. However, it's important to note that dividend-paying companies within the KOSDAQ and venture space are not abundant, so the practical impact of this benefit might be limited for some investors.

Navigating the 5-Year Lock-Up and High Management Fees

The most significant consideration for potential investors in the Korean Growth Fund is the mandatory 5-year lock-up period. This means your invested capital will be inaccessible for withdrawal for at least five years, which could be a constraint for individuals with short-to-medium term financial goals such as purchasing a home or funding education. While it may be possible to transfer ownership on the stock exchange after the fund's listing, low trading volumes could make finding a buyer difficult. Moreover, selling within three years of investment might require returning any tax benefits already received. Another point to consider is the management fee, which stands at 1.2% annually. In today's market, where many low-cost index funds and ETFs are available, this fee is relatively high compared to newer, more cost-effective investment options. Investors should carefully assess whether the fund's potential performance can justify this fee over the long term. Therefore, investing in the Korean Growth Fund should only be considered by those with a genuine long-term investment strategy and funds they can afford to keep locked up for at least five years.

This is not financial advice. Consult a licensed financial advisor.