The 2026 Newborn Special Loan offers low-interest financing for families with newborns, providing up to $300,000 for home purchases or $180,000 for rental security deposits. Eligibility requires a household income under $95,000 annually (or $150,000 for dual-income households) and a child born or adopted within the last two years. This program aims to ease the financial burden of housing for new parents in Korea.

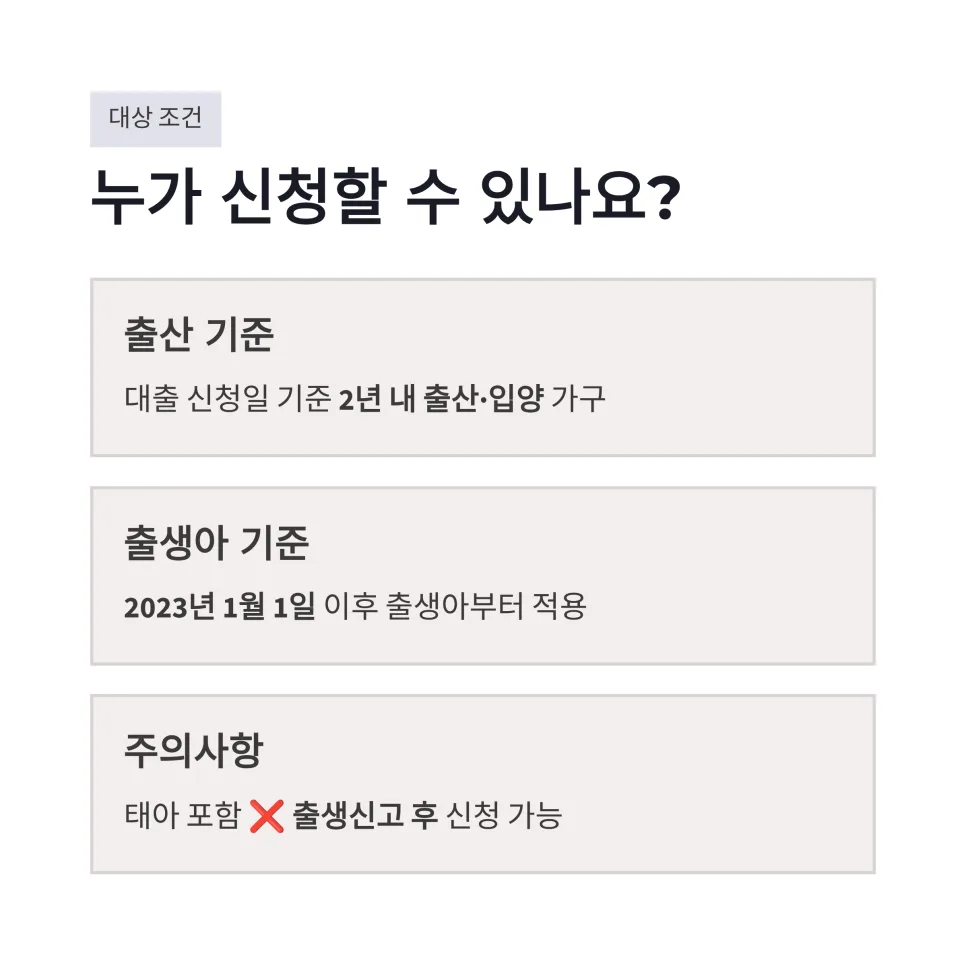

Who Qualifies for the 2026 Newborn Special Loan?

To qualify for the 2026 Newborn Special Loan, your household must have welcomed a new child through birth or adoption within the two years preceding your loan application. This means children born on or after January 1, 2024, are eligible. Importantly, expectant parents cannot apply based on a pregnancy alone; the child must have been officially registered. The primary income requirement is a combined annual household income of no more than $95,000 (approximately ₩130 million). For dual-income households, this limit can extend up to $150,000 (approximately ₩200 million), with the crucial caveat that neither individual income exceeds $95,000. Additionally, asset limits apply: a net worth of $380,000 (approximately ₩511 million) or less for home purchase loans, and $255,000 (approximately ₩345 million) or less for rental deposit loans. Carefully reviewing these detailed criteria is the first step to increasing your chances of loan approval.

Newborn Loan vs. Rental Deposit Loan: Which is Right for You?

The Newborn Special Loan program is divided into two main categories: the "Newborn Special Loan for Home Purchase" (similar to a "Dimldol Loan") and the "Newborn Special Loan for Rental Deposits" (akin to a "Beotimok Loan"). These loans differ in their purpose, eligibility, and the types of housing they support, so selecting the right one for your specific situation is crucial. The Home Purchase loan is for households that are currently without a home or own just one property (which can be refinanced), with loan limits determined by a Loan-to-Value (LTV) ratio of 70% and a Debt-to-Income (DTI) ratio of 60%. First-time homebuyers might qualify for an increased LTV of up to 80%. The Rental Deposit loan is exclusively for renters who are the primary household head and can cover up to 80% of the rental security deposit, with a maximum loan amount of $180,000 (approximately ₩240 million). It's highly recommended to estimate your potential loan amount before signing any contracts.

2026 Newborn Special Loan: Interest Rates & Limits Explained

Understanding the interest rates and loan limits for the Newborn Special Loan can be confusing. For 2026, the key figures are a maximum loan of $300,000 (approximately ₩400 million) for home purchases and $180,000 (approximately ₩240 million) for rental deposits, with dual-income household limits up to $150,000 (approximately ₩200 million). It's important to note that contracts signed before June 27, 2025, might have different criteria, so always verify your contract date. The primary advantage of this loan is its preferential interest rate, significantly lower than market rates, which greatly reduces the initial housing cost burden for new parents. The Home Purchase loan offers a special rate for up to 5 years, and the Rental Deposit loan for up to 4 years, providing substantial interest savings. However, the program's stringent requirements regarding income, assets, home prices, deposit amounts, and existing debts are notable drawbacks. As this is a government-backed policy loan, expect a thorough vetting process, making thorough preparation essential before applying.

Key Considerations for Your Newborn Special Loan Application

When applying for the Newborn Special Loan, the first step is to clearly determine whether you qualify for the Home Purchase or Rental Deposit loan. Next, meticulously review the income and asset requirements and gather all necessary documentation in advance. You can submit your application online through the "Gigeum-e-deun-deun" (기금e든든) system or visit a designated partner bank in person. Required documents typically include a family relations certificate, resident registration, income verification, proof of home purchase or rental agreement, and birth or adoption certificates. Depending on your specific circumstances, additional documents may be requested. This is not financial advice. Consult a licensed financial advisor before making any decisions.