In 2026, choosing the right mortgage repayment strategy can save you tens of thousands of dollars in interest. The principal-equal repayment method minimizes total interest paid but has higher initial payments, while the principal and interest-equal method offers consistent monthly payments for easier budgeting but results in more total interest. Leveraging updated policies on early repayment fees can further reduce your financial burden.

Mortgage Repayment: How Much Interest Can You Save? (2026 Update)

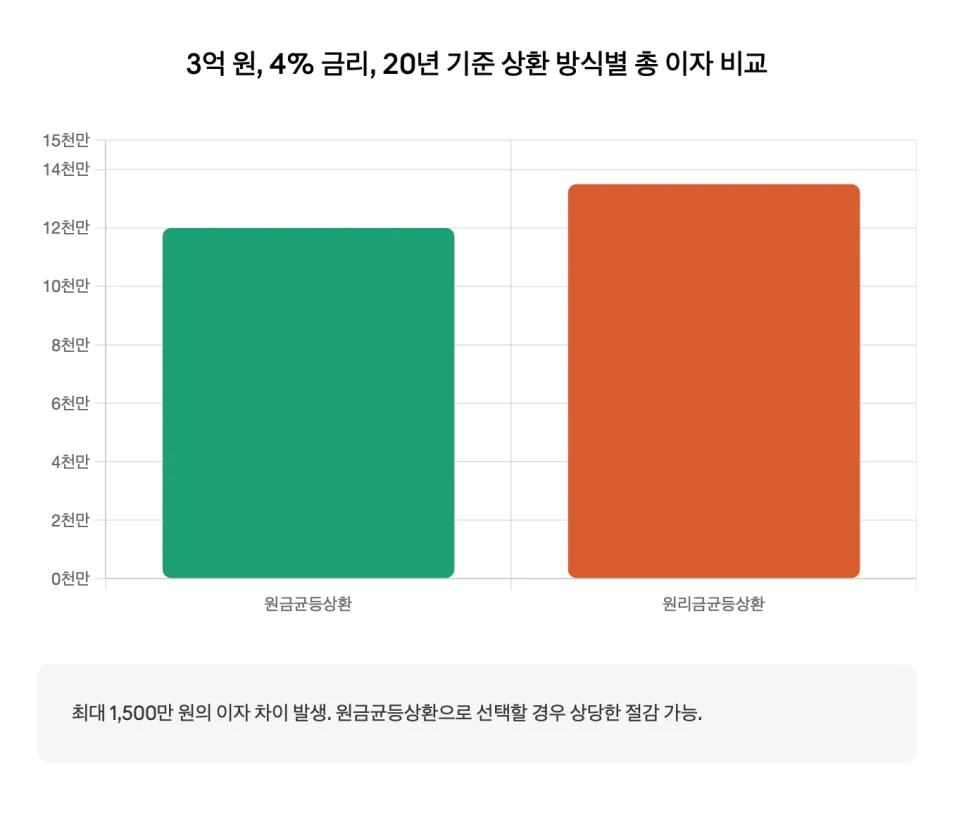

When taking out a mortgage, many focus solely on the interest rate, but the repayment method significantly impacts your total financial obligation. For a $300,000 loan at a 4% interest rate over 20 years, the total interest paid can differ by over $15,000 depending on your chosen strategy. Understanding these repayment structures is key to optimizing your interest payments in the current market. The principal-equal repayment method is particularly effective at minimizing total interest by rapidly reducing the outstanding loan balance. For instance, it can save you over $15,000 compared to the principal and interest-equal method under the same conditions. However, this method comes with higher initial monthly payments, which can be a strain on household budgets for those with less immediate cash flow.

What Are the Benefits of the Principal and Interest-Equal Repayment Method?

The principal and interest-equal repayment method, often referred to as a