For newlyweds in Korea, navigating housing finance can be complex, involving various loan options from rental deposits to home purchases. As of 2026, understanding the eligibility, limits, and interest rates for specialized loans like the 'Didimdol' (stepping stone) loan, 'Bogeumjari' (nest) loan, and dedicated new couple rental deposit loans is crucial. This guide breaks down these government-backed housing funds for American audiences interested in Korean financial products.

Understanding Korean Rental Deposit Loans for New Couples

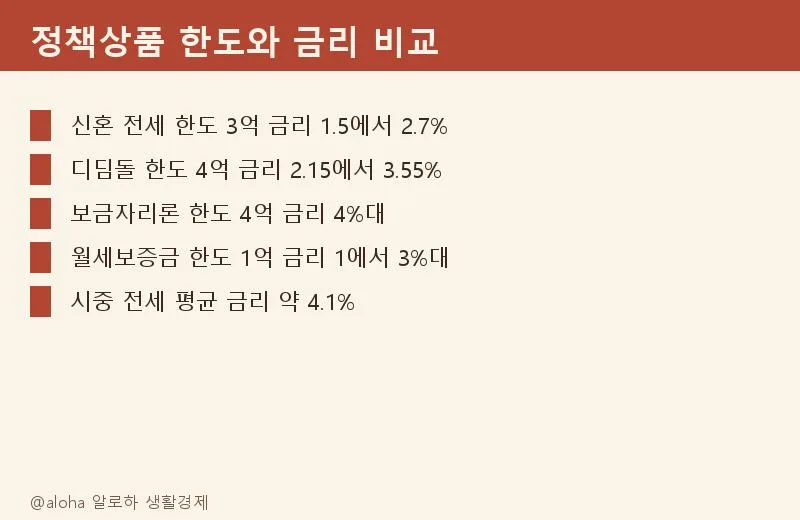

The new couple-exclusive rental deposit loan is a key program supported by the Korea Housing Finance Corporation (HF) and the Housing & Urban Guarantee Corporation (HUG). It allows eligible couples to borrow up to 300 million KRW (approx. $220,000 USD) in the Seoul metropolitan area, or 200 million KRW (approx. $145,000 USD) outside it, covering up to 80% of the rental deposit. Interest rates typically range from 1.5% to 2.7% per year, significantly lower than market rates, easing the financial burden for newlyweds. A friend of mine successfully used this loan by strategically timing their marriage registration, securing housing stability before their wedding. The key requirement is being within seven years of your marriage registration date.

Rental Deposit Loans vs. Apartment Purchase Loans in Korea

For securing a rental deposit, the Youth-Exclusive Guaranteed Monthly Rent Loan, also from the Korea Housing Finance Corporation, is an option. This product supports deposits up to 45 million KRW (approx. $33,000 USD) and monthly rent up to 600,000 KRW (approx. $440 USD) with interest rates between 1.0% and 2.0%. Standard bank loans for rental deposits typically offer up to 100 million KRW (approx. $73,000 USD) at rates around 3.8% or higher. For apartment rental deposits, utilizing guarantees from HF or HUG can secure more favorable loan terms and lower interest rates compared to general bank loans. As of late 2024, the interest rate difference between policy loans and market loans could exceed 1.5 percentage points, translating to thousands of dollars in savings annually. A couple I know, whose combined income exceeded the policy loan threshold, still managed to reduce their interest burden using these guarantee schemes.

Eligibility for the 'Didimdol' Home Purchase Loan

The 'Didimdol' loan is a primary government-backed mortgage product for first-time homebuyers. It's available to couples with a combined annual income of up to 60 million KRW (approx. $44,000 USD), or 85 million KRW (approx. $62,000 USD) for newlyweds or households with two or more children. Loan amounts can reach up to 250 million KRW (approx. $182,000 USD) for general households, and up to 400 million KRW (approx. $290,000 USD) for newlyweds and multi-child families. Interest rates are fixed between 2.15% and 3.55% per year, and the target property price must be 500 million KRW (approx. $365,000 USD) or less. When I purchased my first home seven years ago, this loan provided a fixed rate of 2.85% on a 180 million KRW (approx. $131,000 USD) loan, saving me significant interest compared to the prevailing market rates of over 5% at the time. This loan is particularly beneficial for purchasing homes in suburban areas or smaller cities rather than prime locations in Seoul.

Considering the 'Bogeumjari' Loan as an Alternative

The 'Bogeumjari' loan, offered by the Korea Housing Finance Corporation, serves as a strong alternative if you don't meet the 'Didimdol' loan criteria. It's accessible to couples with a combined annual income up to 70 million KRW (approx. $51,000 USD), or 85 million KRW (approx. $62,000 USD) for newlyweds or multi-child families. The maximum property price limit is 600 million KRW (approx. $438,000 USD). Similar to the 'Didimdol' loan, it's designed to help finance home purchases and offers competitive interest rates, though they might be slightly higher than 'Didimdol'. This loan is a popular choice for middle-income families looking to buy their first or second home in Korea, especially when market interest rates are high.

For more details, check the original source below.