In 2026, a special investment account in Korea offers a reduced dividend tax rate of 9%, down from the standard 15.4%. This benefit, available through a dedicated account, not only lowers your tax burden but can also help you avoid higher income tax brackets and potentially reduce health insurance premiums. This guide breaks down how these savings work for US-based investors interested in Korean financial products.

What Are the Real Tax Savings with Korea's 9% Dividend Tax?

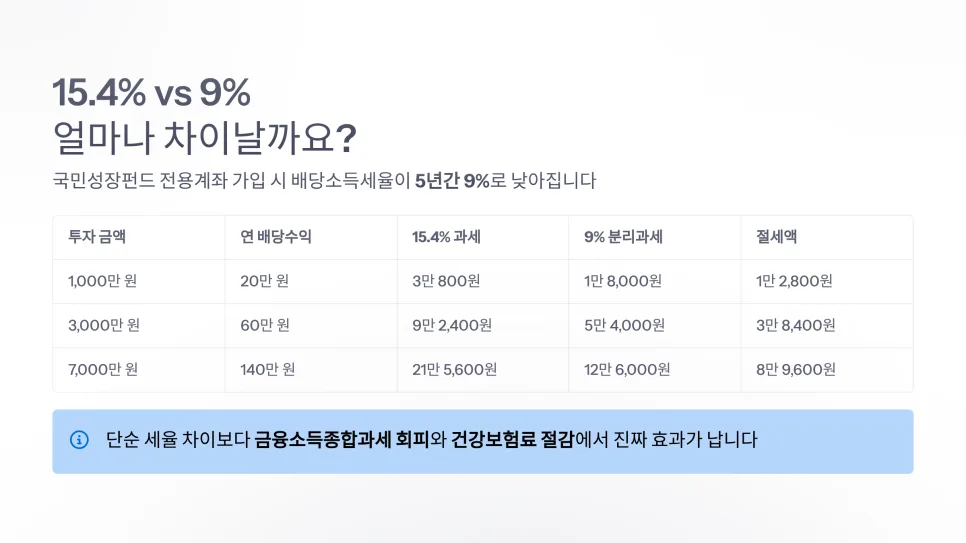

Typically, dividends from most financial products in Korea are taxed at 15.4% (14% income tax + 1.4% local tax). However, by investing through a special account for the "National Growth Fund" (a concept similar to a US-based tax-advantaged savings plan), this rate drops to 9% for five years. For example, if you invest $7,000 USD (approx. 10 million KRW) and earn a 2% annual dividend, the standard tax would be about $22 USD. With the 9% rate, the tax falls to $13 USD, saving you approximately $9 USD annually. As your investment and returns grow, so do these tax savings. For US investors, understanding these nuances is key to maximizing returns on international investments.

How Does This Exclude You from Comprehensive Income Tax?

One of the most significant advantages of this 9% separate taxation is that it can help you avoid the comprehensive income tax bracket. In Korea, if your total annual interest and dividend income exceeds $15,000 USD (approx. 20 million KRW), you may be subject to higher tax rates, potentially up to 49.5%, on that income. However, dividends earned through the National Growth Fund's dedicated account are taxed at a flat 9% and are not added to your other income for comprehensive tax calculations. This is particularly beneficial for investors who have substantial other income sources, effectively capping their tax liability on these specific dividends.

What Are the Advantages for Health Insurance Premiums?

This separate taxation can also positively impact your health insurance costs, especially for individuals classified as 'local subscribers' (similar to self-employed or non-wage earners in the US). Their health insurance premiums are often calculated based on income and assets. Income exceeding $7,000 USD (approx. 10 million KRW) from financial sources can be included in this calculation. By having the National Growth Fund dividends taxed separately at 9%, this income is excluded from the health insurance premium base, potentially lowering your monthly payments. It's important to note that this effect is less pronounced for 'workplace subscribers' (similar to traditional employees) whose premiums are primarily based on salary.

What Should You Watch Out For to Maximize These Tax Benefits?

To fully leverage the 9% separate dividend tax benefit, pay close attention to a few key details. First, you MUST open a "dedicated account" specifically for this fund; standard investment accounts will not qualify for the reduced rate. Second, this 9% tax benefit is limited to a five-year period from your account opening date. Plan accordingly for when this period ends. Finally, consider your overall investment goals. While this fund offers tax advantages on dividends, ensure it aligns with whether your primary objective is dividend income or capital gains from selling the investment. This is not financial advice. Consult a licensed financial advisor before making any investment decisions.

English crawl path

Next English reads from this pilot cluster

Continue through the category hub, latest English stories, and related posts so this translated article is not an isolated URL.

Tags

💬Frequently Asked Questions

What should I check first in Korean Investment Tax Savings 2026: 9% Dividend Tax Guide?

Does this Finance article link back to the Korean source?

Where can I find similar English stories?

English discovery path

Explore more English K-culture stories

Keep browsing the indexed English pilot cluster so Google and readers can move between this story, the category hub, and fresh discovery pages.

Original Source

Read the Korean original