In South Korea, the 'purchase reservation deposit' for private rental housing is often not legally protected like a standard rental deposit. This means if the housing provider goes bankrupt, you might not get your money back. As of 2026, be aware that loans for these deposits can be subject to strict Debt Service Ratio (DSR) and Loan-to-Value (LTV) regulations, potentially leading to unexpected lump-sum repayment demands when converting to a sale.

Why Are Purchase Reservation Deposits Unprotected in Korea?

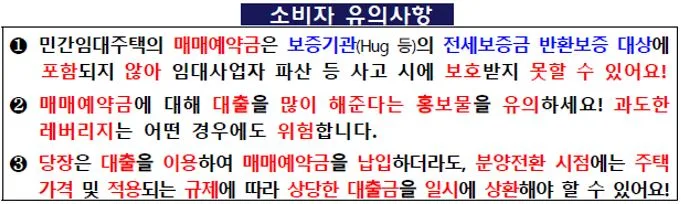

Some private rental housing developers require a 'purchase reservation deposit' (매매예약금) before the mandatory rental period ends, with the intention of converting the property to sale later. However, this transaction is often treated as a private agreement between individuals, not a protected rental deposit. This distinction is critical: if the housing provider faces bankruptcy, you likely won't receive preferential treatment under Korean tenant protection laws (임대차보호법) to recover your funds. Furthermore, these deposits are not covered by government-backed guarantees like the Korea Housing & Urban Guarantee Corporation (HUG) for jeonse (lump-sum deposit) returns. Real-world experiences show these 'side agreements' often fall into a legal gray area, leaving contract holders vulnerable to financial loss.

What Are the Risks with Loans for Purchase Reservation Deposits?

Online promotions frequently advertise financial institutions offering loans covering up to 90% of both rental deposits and purchase reservation deposits combined. While this might seem appealing, using such high leverage can expose you to significant financial risk if housing prices fluctuate. Even if you secure a large loan initially, converting to a mortgage upon sale conversion can trigger substantial lump-sum repayment obligations due to strict DSR and LTV regulations. These regulations limit the total debt you can service based on your income and the property's value, potentially leading to severe liquidity and credit crises for borrowers who haven't planned for this.

Key Considerations for Korean Purchase Reservation Deposit Contracts

It's crucial to understand that a purchase reservation deposit is fundamentally different from a standard rental deposit. While rental deposits offer some legal protection under Korean law, purchase reservation deposits do not. Therefore, during contract signing, you must clarify whether the amount paid is considered part of the rental deposit or a separate purchase reservation fee. Be wary of excessive loan offers and carefully assess the feasibility and repayment capacity of any loan. Remember, the private rental housing system is designed for long-term housing stability, not as a vehicle for speculation.

Common Mistakes When Dealing with Purchase Reservation Deposits

The most frequent mistake is confusing the purchase reservation deposit with a rental deposit and assuming it has legal protection. Many individuals also fall prey to aggressive marketing tactics, such as 'up to 90% loan' offers, leading them to take on excessive debt. A critical oversight is underestimating the impact of DSR and LTV regulations, which can result in unexpected lump-sum repayment demands at the point of sale conversion. Failing to recognize these risks can lead not only to financial losses but also to a damaged credit score. Thoroughly understanding relevant laws and financial regulations before signing any contract is essential.

For more details, check the original source below.