For Koreans born in the 1980s (often called the '80s generation'), closing the wealth gap and achieving homeownership in 2026 requires understanding shifts in the real estate market, securing liquidity, and timing investments strategically. Relying solely on past experiences won't cut it in today's dynamic financial landscape.

Korean '80s Generation Wealth Gap: Beware of Listing Price Traps (2026)

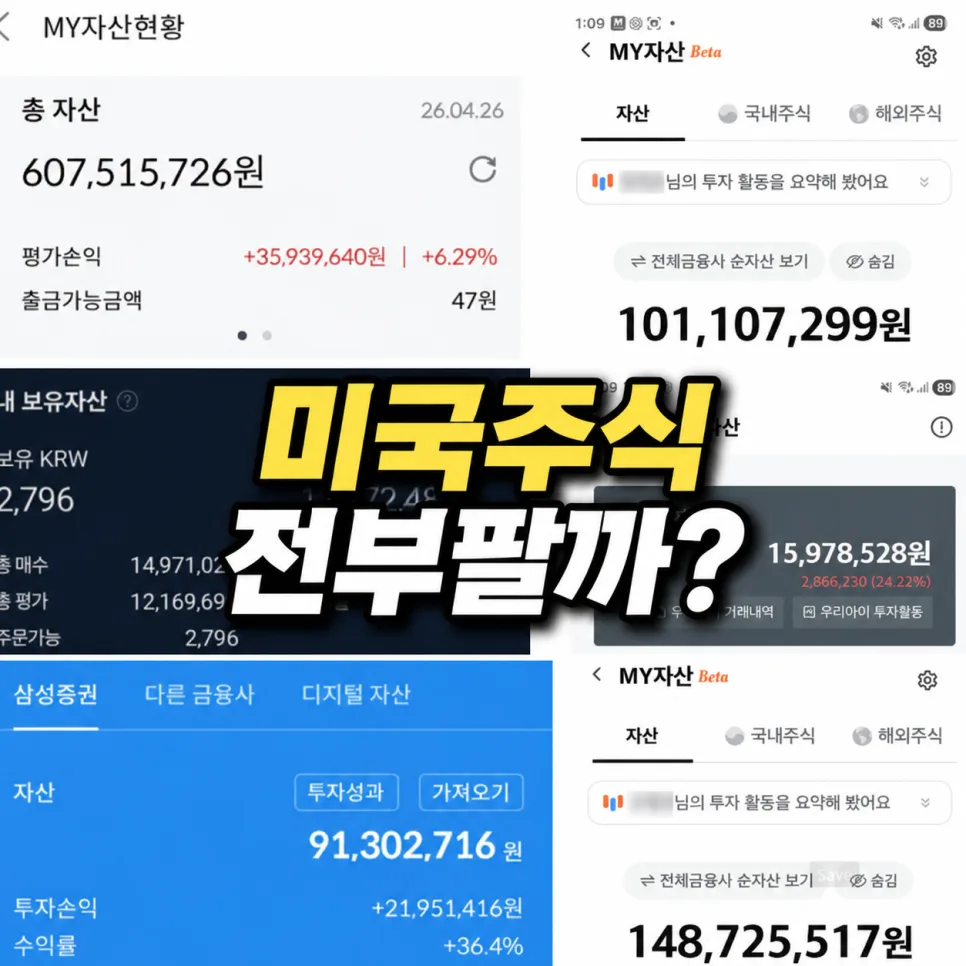

You'll often see headlines about Seoul apartments surpassing ₩1.5 billion (approx. $1.1 million USD), but these statistics can be misleading. Unlike stocks, real estate transactions are less frequent, making it hard to generate precise data. This often leads to sellers listing properties at prices 8% or more above actual sale prices, creating a false sense of continuous market growth. Based on direct observation, the gap between asking prices and actual transaction prices is significant, so don't blindly trust rising listing prices. This perceived price hike can create an illusion of overall market appreciation, but it's crucial to remember the difference from real transaction values. Always compare listing prices with actual sales data to make informed decisions.

Post-Tax Exemption Real Estate Shifts & The Importance of Liquidity

Related Articles

The expiration of the capital gains tax deferral for multiple property owners may encourage them to sell, potentially leading to decreased transaction volume and market contraction. This signals that the real estate market will become even more sensitive to policy changes. For the '80s generation, who may have experienced wealth disparities due to past 'all-in' investment strategies, it's crucial to recognize that securing asset liquidity is now key to wealth growth. In an era of rapid change, similar to the AI revolution, managing assets solely through fixed real estate can be inflexible. In practice, you might find yourself unable to sell even if property values rise, leaving your capital tied up. Therefore, always consider asset liquidity when investing. Highly liquid assets allow for swift adaptation to market shifts, which is advantageous for long-term wealth accumulation.

Lease vs. Rent: Which is Better for Wealth Growth?

For young professionals or newlyweds, a 'Jeonse' (lump-sum security deposit lease) might seem like the only option. However, Jeonse is more about preserving capital than growing it, and it's a system unique to Korea. By tying up a large sum, Jeonse is inefficient for wealth accumulation. It's more beneficial to live in a rented apartment (paying monthly rent) and invest the money that would have been used for a Jeonse deposit. This approach offers more opportunities to grow your assets effectively. From experience, utilizing funds that would otherwise be locked in Jeonse has led to higher returns. Therefore, understand that the true meaning behind 'earning money by living in Jeonse' is closer to 'protecting your money,' and consider exploring investment opportunities by transitioning to a monthly rental system.

Is a Housing Subscription Account Still a Valid 'Future Ticket'?

While the number of housing subscription account holders is declining, I believe these accounts remain a crucial 'future ticket.' There's a high probability that the public housing market will expand in 3-4 years, and a subscription account will be essential for entry. If you're a newlywed or a young adult, there's no need to cancel your existing account. Although there are criticisms about the fairness of the current point-based system, there's a good chance the system will be improved, potentially increasing the weight of winning bids. Therefore, consistently saving through a housing subscription account for public housing or lower-priced apartments is a realistic path to homeownership. The secret to successful investing often lies in understanding 'when' to act. Those who bravely bought during market downturns, like in 2013 when prices were low and others were hesitant, have ultimately seen significant returns.

For more details, check the original source below.