The critical factor many overlook in understanding attached buildings, fixtures, and appurtenances in Korean auction properties is the potential for unexpected additional costs post-acquisition. Failing to accurately determine if an attached building is included in the winning bid can lead to tens of millions of won in losses or costly legal battles.

What Are Attached Buildings and Why Do They Matter in Auctions?

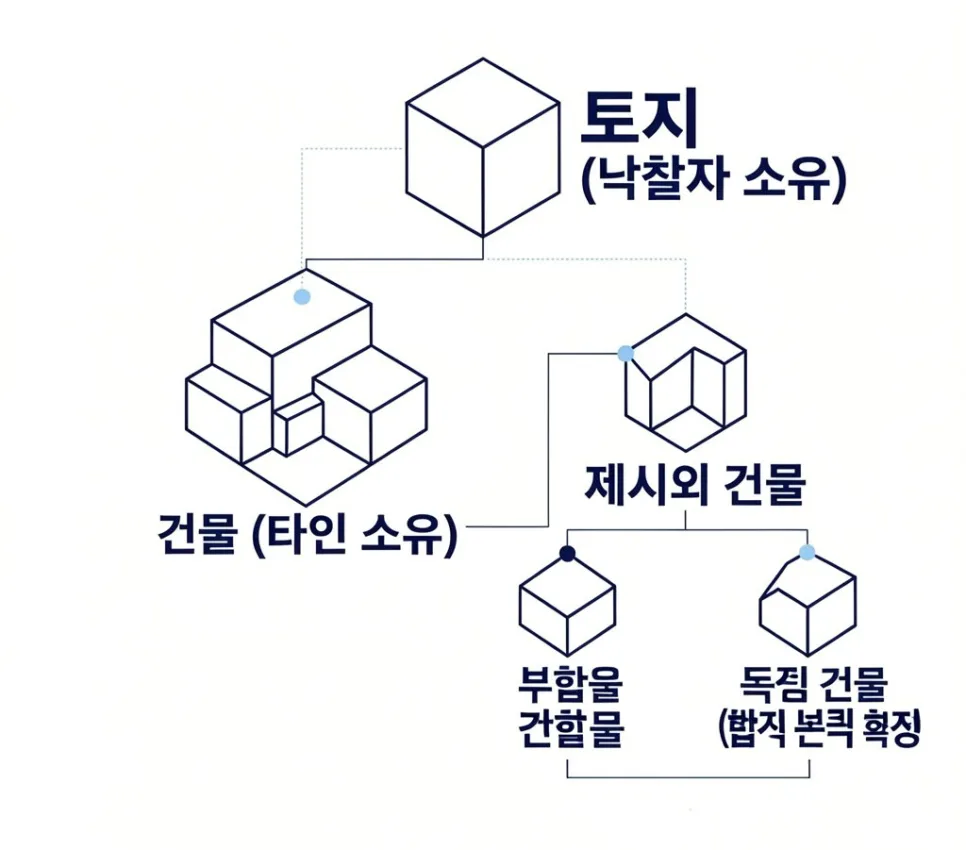

An attached building refers to a structure that exists on the auction property site but is not officially registered on documents like the deed or building register. It's often noted in the auction appraisal as 'attached building present.' Examples include an unregistered warehouse in a yard, an extension built with panels next to a factory, or a container office arbitrarily installed by a tenant. Whether this building is included in the winning bid determines the buyer's ownership scope and additional cost burden, making it a key factor for successful auction investment. It's crucial to distinguish between 'fixtures' (부합물), which are physically inseparable from the main building, and 'independent buildings' (독립 건물), which pose potential ownership disputes.

What's the Difference Between Fixtures and Independent Buildings?

Related Articles

Fixtures (부합물) refer to items completely integrated with the main building or land, making them inseparable or significantly diminishing in value if separated. If an attached building is recognized as a fixture, the winning bidder automatically acquires ownership, even if it wasn't included in the appraisal value – a potential bonus. For instance, an extended warehouse connected structurally, electrically, and via plumbing to the main building is likely considered a fixture. Appurtenances (종물) or independent buildings present a different scenario. Appurtenances are items that, while separable, aid the main building's economic utility (e.g., temporary sheds, container offices). Independent buildings are structures built separately, both structurally and in ownership terms. Owning the land but not the independent building on it can lead to complex disputes, such as surface rights (법정지상권), creating significant legal risks.

Attached Buildings: Fixtures vs. Independent Structures

Clearly distinguishing between fixtures and independent buildings is crucial as it directly impacts auction outcomes. Fixtures are physically and functionally integrated, difficult to separate without value loss, while independent structures are structurally and ownership-wise distinct, allowing for easier separation or relocation. Consequently, fixtures can be a bonus for the buyer, whereas independent buildings pose a high risk of ownership disputes and litigation. A common example: an extended panel warehouse might be a fixture, while a temporary structure built by a tenant or an unregistered shed could be classified as an independent building.

Practical Criteria for Identifying Attached Buildings

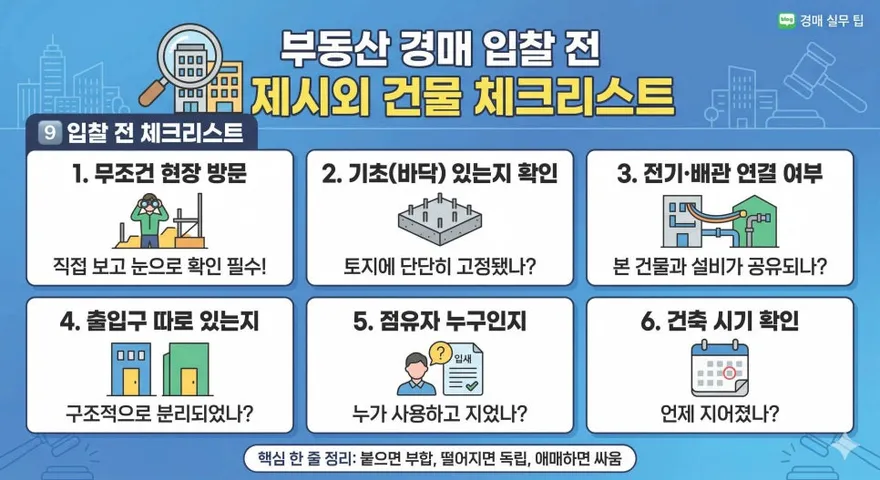

When assessing attached buildings on-site, applying three practical criteria is more effective than navigating complex legal jargon. First, consider 'How attached is it?' The degree of physical integration with the main building is a key indicator for fixture potential. Second, determine 'Who built it?' Buildings arbitrarily constructed by tenants are more likely to be independent structures, posing ownership risks. Third, evaluate 'Can it be moved?' Structures easily dismantled or relocated suggest they are not integral fixtures. These three points help determine if a structure is a fixture or an independent building.

What to Check in the Appraisal Report for Attached Buildings

Before bidding, confirming the 'attached building present' notation in the appraisal report is essential. More importantly, you must verify if this attached building was included in the overall appraised value or if it was assessed separately due to potential ownership complexities. This due diligence helps anticipate potential additional costs after winning the bid. For instance, if an attached building is noted but not appraised, it might imply it's an independent structure, requiring separate negotiation or legal clarification post-auction. Understanding these nuances can prevent significant financial setbacks and legal entanglements, ensuring a smoother investment process.