The upcoming National Growth Fund (국민성장펀드) in South Korea, slated for a June 2026 launch, aims to channel investment into strategic industries like AI and biotech. This policy fund offers significant tax deductions, with potential income tax breaks of up to 40% for investors. Here’s a comprehensive guide to its features, eligibility, and investment outlook for US audiences interested in Korean financial products.

What is the National Growth Fund? (Launching 2026)

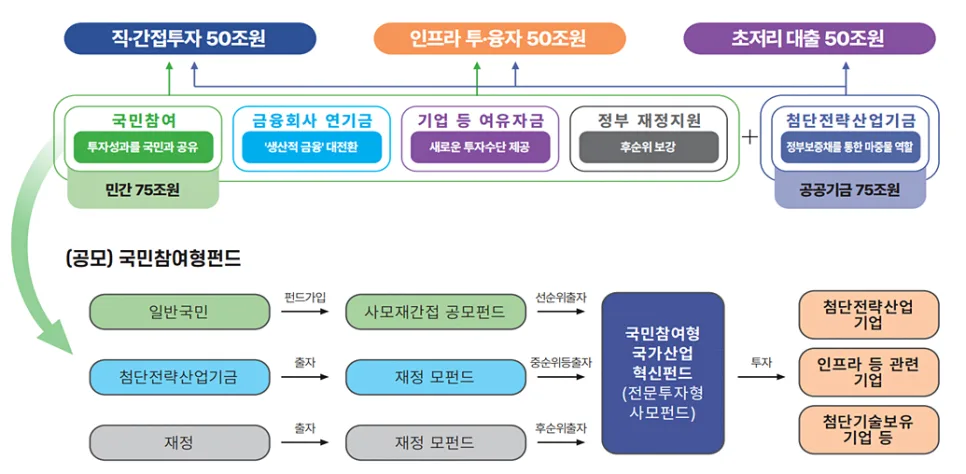

The National Growth Fund is a government-backed policy initiative designed to provide long-term capital for high-growth strategic industries in Korea, including semiconductors, AI, secondary batteries (like those for EVs), and biotechnology. A key component is the 'National Participation National Growth Fund' (국민참여형 국민성장펀드), which will be open to general public investment within a larger 150 trillion KRW (approx. $110 billion USD) framework. This fund aims to build a foundation for future industry investment led by the state and allow everyday investors to share in the growth potential of these sectors. It operates as an indirect investment vehicle, allowing participation across various growth industries rather than direct stock picking. It's crucial to understand that despite the 'National' moniker and policy backing, this is an investment product, not a guaranteed deposit like a savings account. Investors must be aware of the potential for both profits and losses.

When Can You Invest in the National Growth Fund?

Based on current information, the National Participation National Growth Fund is expected to launch around June 2026. Official statements from financial authorities indicate a similar timeframe, with plans for annual fundraising of approximately 600 billion KRW (around $440 million USD). While some anticipate a May launch, the exact date when sales will officially begin through banks and securities firms will be confirmed by the financial authorities. It's wise to plan your investment strategy around this anticipated launch. Keep an eye on official announcements from the Financial Services Commission (FSC) or the Financial Supervisory Service (FSS) for the precise sales start date.

How to Invest and Eligibility for the National Growth Fund

Once sales commence, investment in the National Growth Fund will likely be accessible through major Korean banks and securities firms via their mobile apps, websites, or physical branches. Similar to investing in other mutual funds or Individual Savings Accounts (ISAs) in Korea, you'll need to complete identity verification, review product descriptions, and acknowledge the investment risks before proceeding. Typically, you'll need a valid Korean bank account, identification, and digital authentication methods like a joint certificate or mobile verification. Note that not all financial institutions may offer the fund under identical terms; differences in available hours, minimum investment amounts, fees, and account opening procedures might exist. Therefore, thoroughly reviewing the specific financial institution's product disclosure statement is essential before investing. Current discussions suggest eligibility may extend to individuals aged 19 and above, or those aged 15 and above with earned income. A key condition for tax benefits is likely a minimum investment period of three years, making this fund more suitable for long-term investors with disposable income.

The Core Appeal: 40% Tax Deduction and Real Savings

The most attractive feature of the National Growth Fund is its potential tax deduction benefit. The proposed tax support plan outlines tiered deduction rates based on investment amount: up to 40% for investments of 30 million KRW (approx. $22,000 USD) or less, 20% for amounts between 30 million and 50 million KRW (approx. $22,000 - $36,500 USD), and 10% for amounts exceeding 50 million KRW up to 70 million KRW (approx. $36,500 - $51,000 USD). For example, investing 30 million KRW could potentially lead to a tax deduction of up to 12 million KRW (approx. $8,800 USD). However, it's vital to understand that a tax deduction doesn't directly translate to a tax refund of the same amount. Deductions reduce your taxable income, meaning the actual tax savings depend on your individual income tax bracket. Someone in a higher tax bracket will see a greater reduction in their tax liability than someone in a lower bracket. Therefore, calculating your potential tax savings based on your personal income and tax rate is crucial to gauge the true financial benefit.

Is the National Growth Fund Principal Protected? Understanding Loss Potential

A common misconception surrounding the National Growth Fund is the idea of principal protection. While government funds may be allocated as a subordinated layer to absorb some initial losses, this does not equate to a full guarantee of your invested capital. Unlike bank deposits protected under the depositor protection laws, this fund is not guaranteed. If the performance of the companies or industries the fund invests in falls short of expectations, there is still a possibility of losing your principal investment. Therefore, approaching this fund solely on the basis of government backing would be unwise. It's essential to recognize that this is a medium- to long-term investment product with inherent risks. It is best suited for investors who can tolerate risk and have established long-term investment goals.

For more details, check the original source below.