Investing in stocks using family members' names can seem like a smart tax strategy, but it carries significant risks, especially concerning the concept of 'joint ownership' liability and the legal dangers of nominee accounts. Understanding these potential pitfalls is crucial before establishing a corporate entity or transferring assets.

What is Joint Ownership Liability in Family Corporate Investments?

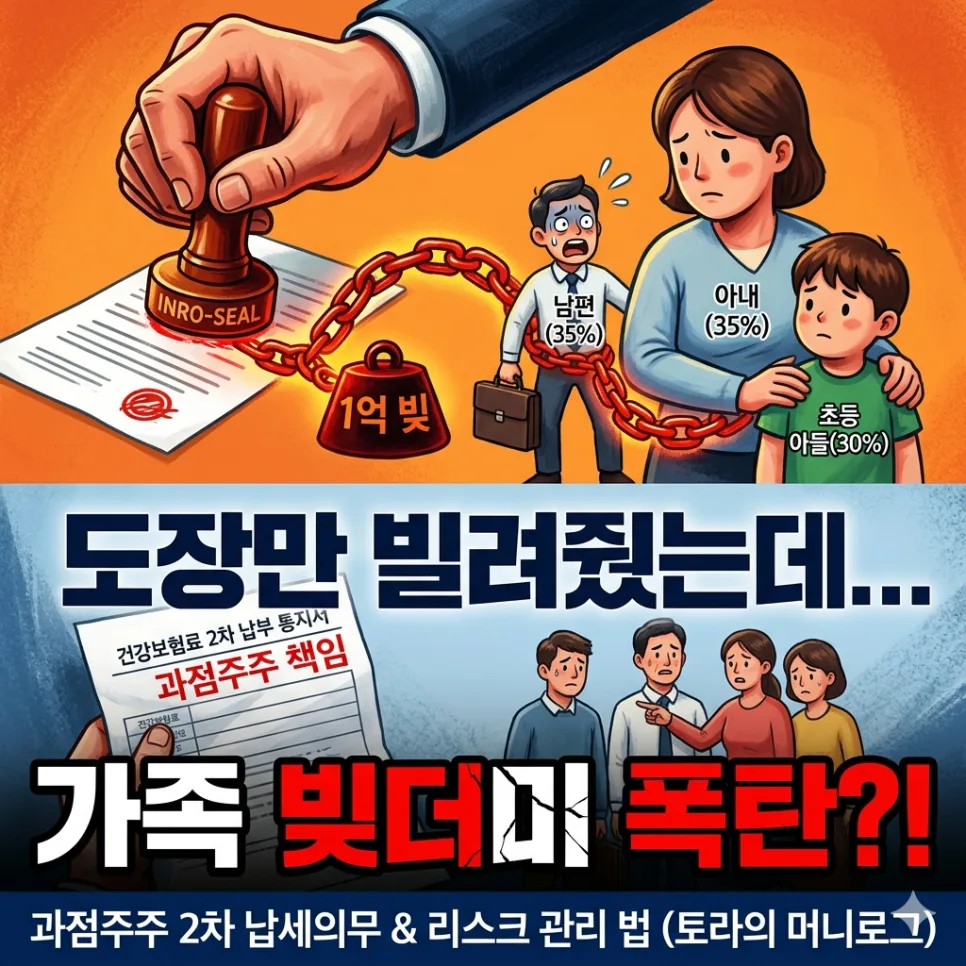

While setting up a corporation under family members' names might offer tax advantages or leverage, overlooking the 'joint ownership' liability (과점주주, gwajeomjuju) can lead to unexpected debt. In Korea, a joint owner is defined as someone who effectively exercises control over more than 50% of a company's shares. If the corporation defaults on taxes or mandatory insurance payments, these individuals can be held secondarily liable for the outstanding debt. For instance, a case involved a family corporation where the husband held 35%, the wife 35%, and their elementary school son 30%. When the husband defaulted on over $70,000 in health insurance premiums, both the wife and son were pursued for the debt due to their effective control. This highlights that family involvement in ownership means sharing not just profits, but also potential liabilities. Therefore, carefully consider these legal responsibilities when adding family members as shareholders.

Related Articles

Why Is Proving Nominee Account Status So Difficult?

While some might suggest you can avoid secondary tax liability by proving you were merely a nominee (holding shares on behalf of someone else), the reality is far more complex. Tax authorities operate on the principle of substance over form, meaning they look at who truly benefits from and controls the assets. Even if you weren't actively involved in management or receiving dividends, having your signature on shareholder meeting minutes or submitting your personal seal certificate (similar to a notarized signature) can be interpreted by courts as exercising effective control. South Korea's tax authorities have sophisticated systems for tracking financial transactions, making it difficult to rely solely on claims of 'unfairness' without concrete numerical evidence. It's essential to simulate worst-case scenarios, such as being listed on the board or shareholder registry, before using family members' names for investments.

What Are the Risks of Asset Division and Debt Collection in Divorce with Family Accounts?

Divorce does not automatically extinguish debts owed to third parties. Many mistakenly believe that once a couple separates, their financial obligations to others disappear. However, this is not legally the case. If assets are transferred to a family member's name during a divorce settlement, creditors can file a lawsuit to challenge the transfer as a fraudulent act (사해행위, sahaehaengwi). When a business faces financial difficulties, the first priority should be protecting the family's home and essential assets, not reckless expansion. If personal guarantees are extended for business loans or family members' names are involved, business failure can directly lead to household bankruptcy. For industries sensitive to economic fluctuations, it's crucial to always assess downside risks first and structure operations within the limited liability framework of a corporation to manage risk effectively.

What Precautions Should Be Taken for Stock Investments Under Family Names?

Continuing investments for the sake of family well-being is common, but simplifying legal procedures or casually lending names under the guise of 'family' can lead to significant risks. The most critical step is rigorously managing personal seals and digital certificates (like joint certificates). Even between spouses, handing over a blank check for personal finances and credit is extremely dangerous and should never be done lightly. Furthermore, when designing the ownership structure, always verify the potential for joint ownership liability. Finally, it is imperative to maintain a clear separation between business and personal finances. The moment business loans require personal guarantees or family members' names are involved, business failure can directly translate into family bankruptcy. In investing, learning how to protect what you have is as important as learning how to generate profits.

English crawl path

Next English reads from this pilot cluster

Continue through the category hub, latest English stories, and related posts so this translated article is not an isolated URL.

Tags

💬Frequently Asked Questions

What should I check first in Family Stock Investment Risks 2026: Joint Ownership & Tax Pitfalls?

Does this Finance article link back to the Korean source?

Where can I find similar English stories?

English discovery path

Explore more English K-culture stories

Keep browsing the indexed English pilot cluster so Google and readers can move between this story, the category hub, and fresh discovery pages.

Original Source

Read the Korean original