Many Americans dreaming of homeownership are looking for ways to secure low mortgage rates. In 2026, Korea's Didimdol Loan (디딤돌대출) offers rates as low as 2%, making it an attractive option for eligible individuals. This guide breaks down the income and asset requirements, loan limits, and special conditions to help you qualify for this government-backed home financing. We'll cover everything from eligibility criteria to maximizing your benefits, ensuring you have the information needed for a successful home purchase.

Who Qualifies for the 2026 Didimdol Loan? (Income & Asset Requirements)

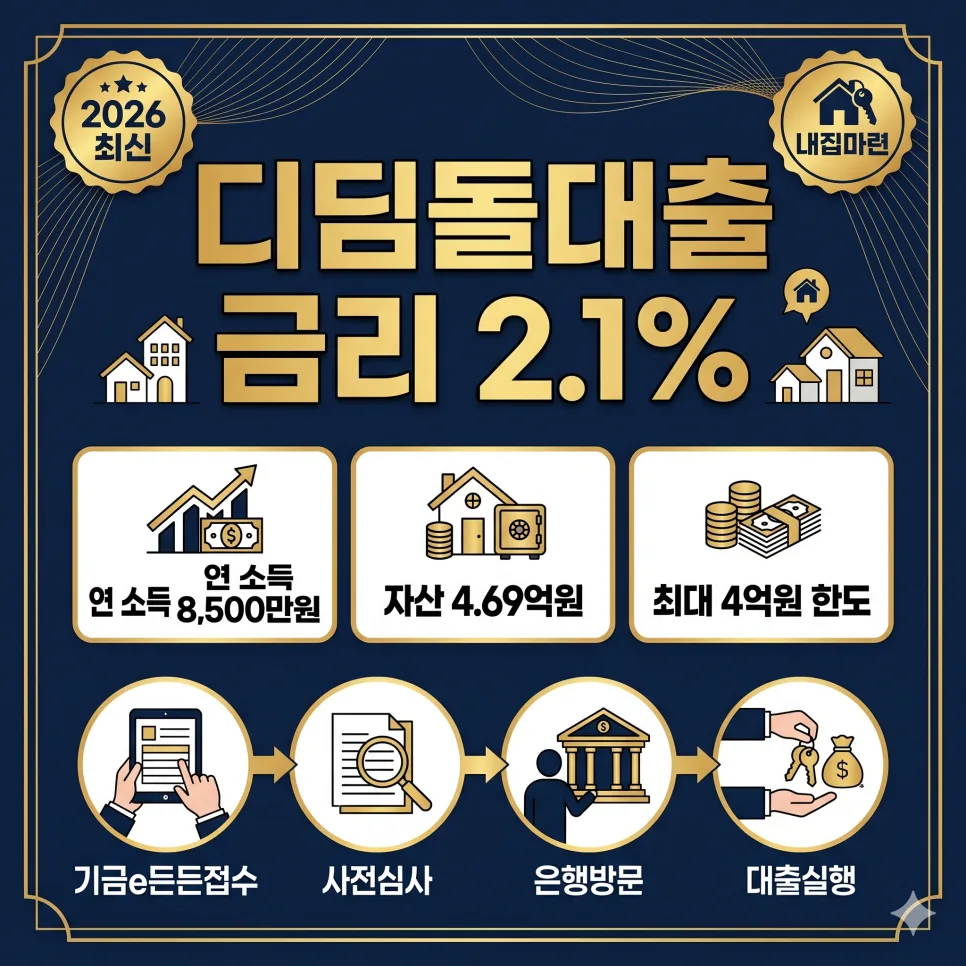

The Didimdol Loan is a flagship policy finance product designed to stabilize housing for low-to-middle-income households in Korea. Generally, it's available to unhoused heads of households earning under 60 million KRW (approximately $45,000 USD) annually. However, this income threshold is relaxed for specific groups: first-time homebuyers can earn up to 70 million KRW (approx. $52,000 USD), while newlywed couples and families with two or more children can have incomes up to 85 million KRW (approx. $63,000 USD). Additionally, applicants and their spouses must have a combined net asset value not exceeding 469 million KRW (approx. $350,000 USD), a figure subject to adjustment based on inflation. The target housing must be under 85 square meters (approx. 915 sq ft) and valued at 500 million KRW (approx. $370,000 USD) or less. For newlyweds and families with multiple children, this property value limit extends to 600 million KRW (approx. $445,000 USD). Meeting these criteria allows access to fixed interest rates ranging from 2.1% to 3.3%.

Maximize Your Loan: Up to $445K & Rate Reduction Tips

The standard Didimdol Loan limit is 250 million KRW (approx. $185,000 USD). However, this can be increased for certain applicants. First-time homebuyers can qualify for up to 300 million KRW (approx. $222,000 USD), while newlyweds and families with multiple children can access up to 400 million KRW (approx. $296,000 USD). To further reduce your interest rate, consider these options: paying into a housing subscription savings account for over five years can earn a 0.3%p discount. Additionally, using an electronic contract for the property purchase can provide another 0.1%p reduction. These discounts, when combined, can significantly lower your monthly payments, making homeownership more affordable. For example, a 0.4%p reduction on a 300 million KRW loan over 30 years could save you thousands of dollars in interest.

Understanding Residency Obligations & Penalties

A critical condition of the Didimdol Loan is the requirement to reside in the purchased property. Borrowers must move into the home within one month of the loan's disbursement and maintain residency for at least one year. Failure to comply with this real-residency obligation will result in the immediate repayment of the entire loan amount. This stipulation is in place to ensure the loan's purpose of supporting owner-occupiers is met. Therefore, it's crucial to carefully assess your ability to meet these residency requirements before applying. If you anticipate needing to rent out the property immediately or have other circumstances that would prevent you from living there, this loan may not be suitable for your situation.

Why Didimdol Loan is a Top Choice for Homebuyers

The Didimdol Loan stands out due to its exceptionally low fixed interest rates, which are significantly lower than typical market rates for conventional mortgages in the US. This government backing provides a safety net and ensures affordability, especially for young families and first-time buyers. The tiered income requirements and increased loan limits for specific demographics demonstrate a commitment to inclusive housing support. While the residency requirement is strict, it aligns with the goal of promoting stable communities. For those who qualify, the long-term savings on interest payments can be substantial, making it a powerful tool for building equity and achieving the dream of homeownership. This program is a prime example of how government initiatives can make a significant impact on the housing market.

For more details, check the original source below.