The arrival of Lecanemab, a groundbreaking Alzheimer's treatment, brings renewed hope for dementia care. However, this medical advancement also highlights the significant financial burden of treatment and long-term care. As we look towards 2026, understanding the necessity and benefits of dementia insurance is crucial for securing your future financial well-being.

Lecanemab: A New Era in Dementia Treatment?

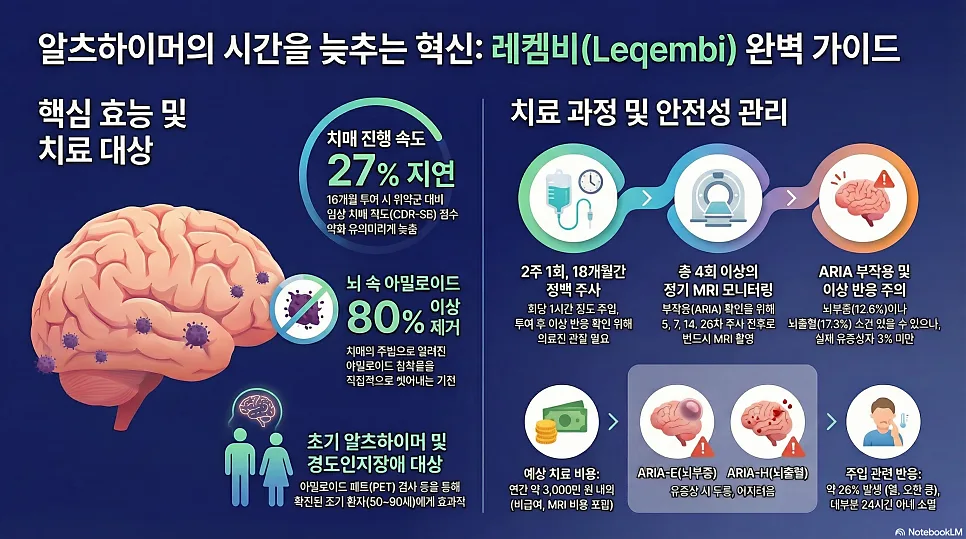

Lecanemab, marketed as Leqembi, represents a significant leap forward in Alzheimer's therapy. Unlike previous treatments that primarily managed symptoms, Leqembi targets the underlying pathology by removing amyloid-beta plaques, a key hallmark of Alzheimer's disease. Clinical trials have shown that Leqembi can slow the progression of cognitive decline in early-stage Alzheimer's patients. This mechanism offers a more proactive approach to managing the disease, providing a glimmer of hope for patients and their families. However, the introduction of such advanced therapies often comes with substantial costs, including regular infusions, monitoring, and ongoing care, making financial preparedness a critical consideration.

Understanding the Financial Burden of Dementia Care

Dementia care extends far beyond the cost of medication. For treatments like Leqembi, which require regular administration and monitoring, patients can expect ongoing expenses for infusions, diagnostic tests like MRIs, and physician consultations. Beyond direct medical costs, the long-term nature of dementia necessitates significant expenditure on professional caregiving, home modifications, and daily living assistance. Many families find that the costs associated with long-term care and daily support are even more substantial than the direct medical treatment expenses. Therefore, a comprehensive financial strategy is essential to manage these multifaceted costs effectively.

Why Dementia Insurance is Crucial Now

Dementia is a condition that often requires extensive and prolonged care, placing a significant strain on both patients and their families. While medical advancements like Leqembi offer promising treatment avenues, they also underscore the growing financial implications of managing the disease over time. Modern dementia insurance policies are evolving to address these challenges, offering enhanced coverage for early-stage cognitive impairment (mild cognitive impairment or MCI), substantial lump-sum payouts for severe dementia diagnoses, and robust benefits for long-term care and nursing services. For individuals with a family history of dementia or those proactively planning for retirement, securing insurance while healthy is paramount. Insurance premiums increase significantly with age and pre-existing conditions, making early enrollment a financially prudent decision.

What Does Modern Dementia Insurance Cover?

Contemporary dementia insurance policies are designed to provide comprehensive financial protection against the escalating costs associated with dementia. Key coverage areas often include diagnosis benefits for mild cognitive impairment (MCI) and severe dementia, which can provide a crucial financial cushion for early intervention and ongoing care. Furthermore, these policies frequently offer substantial benefits for long-term care services, including professional nursing, in-home caregiving, and support for assisted living facilities. Some plans also include provisions for specialized equipment and home modifications to ensure patient safety and comfort. By addressing these diverse needs, dementia insurance aims to alleviate the financial pressure on families, allowing them to focus on providing the best possible care for their loved ones.

For more details, check the original source below.