In 2026, choosing the right health insurance plan involves comparing coverage tiers, deductibles, and out-of-pocket expenses across different generations of plans. The latest generation (often referred to as '4th generation') may offer lower premiums but can adjust based on your actual medical usage, making personal healthcare habits a key factor in determining the best value.

Why Understanding Health Insurance Plan Generations Matters

Health insurance plans are structured differently based on when you enroll, typically categorized into 'generations.' The most recent plans, often called '4th generation,' tend to have lower initial premiums. However, a key feature is that their premiums can fluctuate based on how much you use non-essential medical services (like physical therapy or certain injections). For example, if you frequently utilize these types of treatments, your 4th generation plan's premium could increase significantly. Therefore, it's crucial to analyze your expected healthcare needs and spending patterns to decide which generation offers the best long-term financial benefit. Consider the case of a busy professional, 'John,' who initially opted for a 4th generation plan to save money upfront. After an injury led to frequent physical therapy sessions and other non-essential treatments, his monthly costs unexpectedly rose, prompting him to re-evaluate his coverage options.

Why Deductibles and Coverage Limits Trump Premiums

While many shoppers focus on the monthly premium, the actual out-of-pocket costs you'll face when receiving medical care—your deductible and the scope of coverage for non-essential treatments—are far more critical. A plan with a lower monthly premium might seem attractive, but if it has a high deductible or excludes common non-essential services (like specialized physical therapy, MRIs, or specific injections), your actual medical expenses could be much higher. It's essential to thoroughly review the policy details to understand your deductible amounts and precisely which services are covered or excluded. For instance, understanding the co-insurance percentages for various treatments is vital. A plan might have a low deductible but a high co-insurance rate, meaning you still pay a significant portion of the bill for certain procedures.

Understanding Premium Adjustments in Renewable Plans

Most health insurance plans operate on a renewable basis, meaning your premium isn't fixed for the entire policy term. Instead, it can be adjusted periodically, typically annually or every three years. Factors influencing these adjustments include your age, the overall claims history of all policyholders (known as the loss ratio), and general increases in healthcare costs. If you choose a plan solely based on its low initial premium, be prepared for potential increases as you age or if healthcare costs rise. It's wise to consider not just the current cost but also the projected long-term premium trajectory to ensure the plan remains affordable throughout your life.

Why You Should Reconsider Canceling Existing Health Insurance

Switching from an older health insurance plan to a newer one can seem appealing, especially if the new plan offers a lower monthly premium. However, this decision requires careful consideration. Older plans, particularly those from earlier generations, might include benefits or coverage options that are no longer available in current policies. For example, some older plans might have lower deductibles or broader coverage for specific treatments that are now restricted or excluded in newer plans. Simply comparing monthly costs without examining the detailed benefits could lead to a situation where you lose valuable coverage. It's crucial to assess your current health status, anticipated future medical needs, and the specific benefits of your existing plan before making a switch.

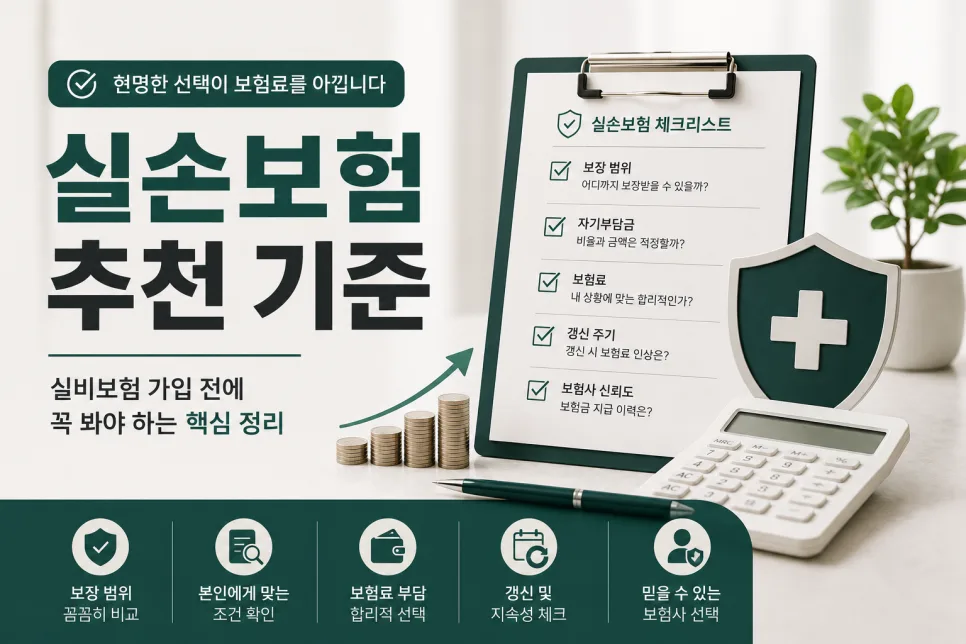

Review our checklist before choosing a health insurance plan.