A critical aspect of the 2026 gift tax regulations that many overlook is the reduction in the spousal gift deduction and increased scrutiny on loans used for gifts. To navigate these changes legally and effectively, it's essential to understand the latest tax law trends and implement smart tax-saving strategies.

What's Driving the 2026 Gift Tax Regulation Changes?

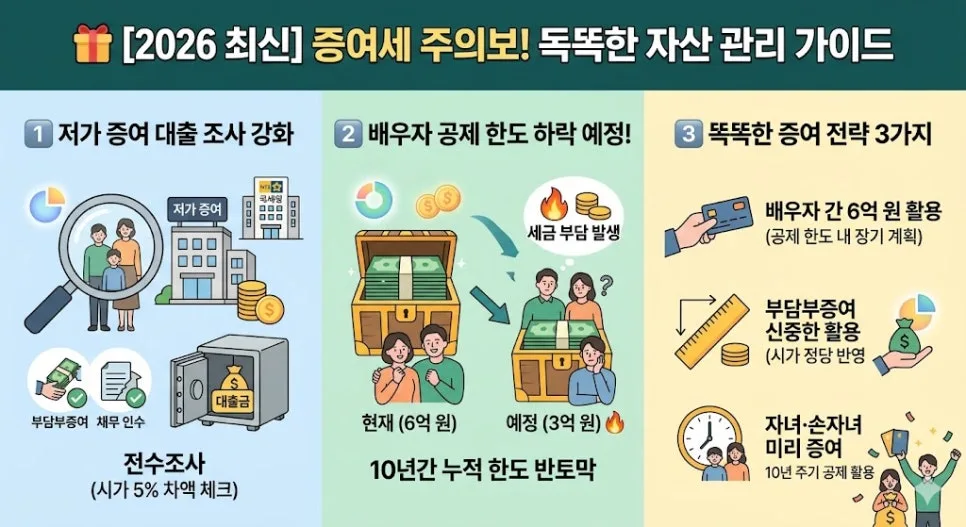

The government is tightening its grip on gift tax regulations, with a particular focus on reducing spousal benefits and intensifying investigations into low-value gifts. These changes are becoming more concrete as 2026 approaches, causing confusion for many. The National Tax Service (NTS) has initiated thorough investigations into cases where parents gift real estate or other assets to their children at significantly below market value, especially when loans are involved in the funding. This scrutiny can lead not only to the recovery of gift tax on the difference but also to investigations into the source of funds for loan repayments, potentially resulting in unexpected tax burdens. Therefore, it's crucial to consider these regulatory shifts when planning any gifts.

Will the Spousal Gift Deduction Limit Drop from $600K to $300K in 2026?

One of the most significant issues is the potential reduction of the spousal gift deduction limit from a cumulative $600,000 over 10 years to $300,000. If this tax law amendment passes, it could be implemented as early as 2027. This means the tax-free gift amount between spouses would be halved, potentially creating a new gift tax liability on amounts exceeding $300,000. Due to these anticipated changes, many high-net-worth individuals are rushing to complete their gifting before the law takes effect. Until the end of 2026, the existing $600,000 deduction is still available, making it important to plan your gifting strategy carefully with long-term asset management and estate planning in mind.

What Are Smart Tax-Saving Strategies Before the 2026 Tax Law Changes?

The period leading up to the potential reduction in the spousal gift deduction limit in 2026 presents a final window for legal tax savings. Firstly, take full advantage of the current $600,000 spousal gift deduction. Pre-transferring assets can help reduce future estate tax burdens. However, remember that assets gifted within 10 years of death may be added back to the estate, so plan accordingly for the long term. Secondly, be cautious with gifts involving assumption of debt (부담부증여). Instead of gifting at a significantly undervalued price, it's crucial to reflect the fair market value (appraised value) and consult with a tax professional. Thirdly, consider gifting to children and grandchildren in advance. Adults can receive up to $50,000 (approx. $7,000 USD) and minors up to $20,000 (approx. $1,400 USD) every 10 years without gift tax. Utilizing these allowances can be beneficial for long-term asset transfer.

What Should You Watch Out For in Low-Value Gift Scrutiny Involving Loans?

The NTS is actively investigating instances where parents gift assets like real estate to their children at prices significantly below market value, especially when loans are used to fund the transaction. A low-value gift is generally defined as a transaction where the difference between the market value and the actual transaction price is 5% of the market value or more, or exceeds $300,000 (approx. $21,000 USD). The difference can be subject to gift tax. This is particularly scrutinized in cases of assumed debt gifts (부담부증여) or debt assumption structures where children might appear to be taking on the parent's debt, but it's essentially a low-value gift. If the child cannot adequately prove their ability to repay the loan, the investigation can extend beyond gift tax recovery to include an examination of the source of funds for loan repayment, potentially leading to a much larger tax liability than anticipated. If considering a low-value gift, ensure you have clear documentation for loan repayment capacity and consult with a tax advisor.

For more details, check the original source below.