Navigating the complexities of health insurance premiums when you have significant dividend income can be tricky. In 2026, while tax rules for financial income are evolving, understanding how these earnings impact your National Health Insurance Service (NHIS) contributions is crucial. Exceeding certain thresholds can lead to unexpected premium hikes or loss of dependent status, even if you benefit from new tax breaks. This guide breaks down the key criteria to help you manage your financial income and health insurance effectively.

How Do 2026 Financial Income Taxes and Health Insurance Premiums Differ?

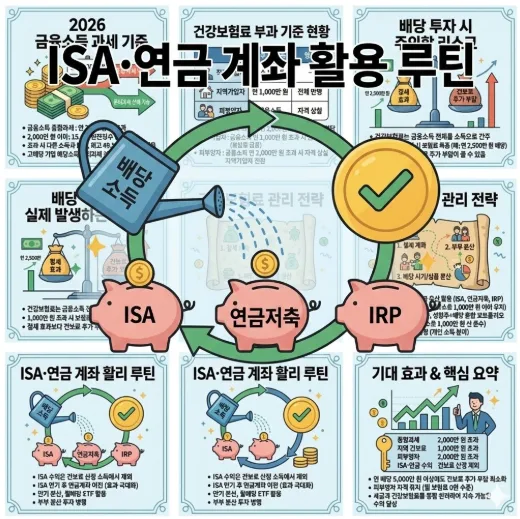

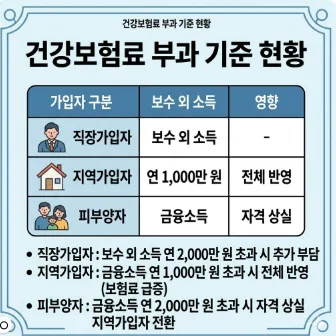

Starting in 2026, South Korea offers a new option for high-dividend stocks: a separate tax rate of up to 30%, potentially reducing the overall tax burden compared to the standard progressive tax system, which can reach 49.5% for income exceeding 20 million KRW (approximately $14,500 USD). However, this tax benefit doesn't directly translate to health insurance premiums. The NHIS calculates premiums based on your total income, not just the income taxed under the progressive system. For employees (직장가입자), earning over 20 million KRW (approx. $14,500 USD) from sources outside their salary can trigger additional income-based premiums. For self-employed individuals (지역가입자), exceeding 10 million KRW (approx. $7,250 USD) in financial income means the full amount is factored into your premium calculation, significantly increasing costs. For dependents (피부양자), exceeding 20 million KRW (approx. $14,500 USD) in financial income means losing dependent status and becoming a regional subscriber, incurring property-based premiums as well. Many individuals find that the tax savings from separate taxation are offset by higher insurance premiums, leading to a net loss.

What Strategies Can Prevent a Health Insurance Premium Shock?

Related Articles

The most effective way to avoid a health insurance premium shock is to maximize the use of tax-advantaged accounts like ISA (Individual Savings Accounts), pension savings accounts (연금저축), and IRP (Individual Retirement Pension). The earnings within these accounts are generally excluded from the income calculation for NHIS premiums. By strategically utilizing these accounts and rolling them over into pension accounts upon maturity, you can significantly reduce your long-term premium burden. Another key strategy is asset diversification between spouses. If each spouse's financial income remains below 10 million KRW (approx. $7,250 USD), they can maintain dependent status, avoiding the jump to regional subscriber premiums. When investing in dividends, it's crucial to diversify not only your investments but also the timing of your dividend payouts to avoid concentrating income in a single period. For instance, opting for monthly dividend ETFs or spreading investments across different companies can help smooth out income streams.

How Should Dividend Investors Manage Health Insurance Impacts?

For regional subscribers or dependents, exceeding just 10 million KRW (approx. $7,250 USD) in annual financial income can cause your entire financial income to be fully reflected in your premium calculation, leading to unexpectedly high costs. For example, receiving 25 million KRW (approx. $18,000 USD) in dividend income might be tax-efficient due to separate taxation, but the resulting increase in health insurance premiums could negate those savings. Therefore, dividend investors must consider both taxes and health insurance premiums when constructing their portfolios. Instead of solely focusing on high-dividend stocks, a mix of growth and dividend stocks, or utilizing monthly dividend ETFs, can help distribute income more evenly. For high-net-worth individuals, establishing a corporation to separate investment income from personal income is another option, but this requires careful consultation with financial professionals.

Diversifying your dividend income across different asset classes and payout schedules is key to managing your overall financial obligations.

What Are the Key Considerations for Health Insurance Management?

It's important to be aware that accounts like ISAs and pension accounts may have withdrawal restrictions or minimum holding periods, so careful financial planning is essential. Furthermore, electing separate taxation for dividend income requires a specific declaration during your annual income tax filing, and not all high-dividend stocks qualify for this separate taxation, so verifying individual stock requirements is necessary. Over-diversifying assets can sometimes reduce overall investment efficiency, so balancing expected returns with acceptable risk is crucial. Because premium calculation standards and their impact vary significantly based on individual income levels, asset size, and subscriber type, consulting with a financial expert to develop a personalized management strategy is highly recommended.

For more details, check the original source below.