Considering a mortgage that covers 90% or more of your home's price? In 2026, this high loan-to-value (LTV) ratio carries significant risks, especially with fluctuating interest rates and potential market downturns. Understanding these dangers and having a solid repayment plan is crucial for any prospective US homeowner.

Why Are 90%+ Mortgages Risky in Today's Market?

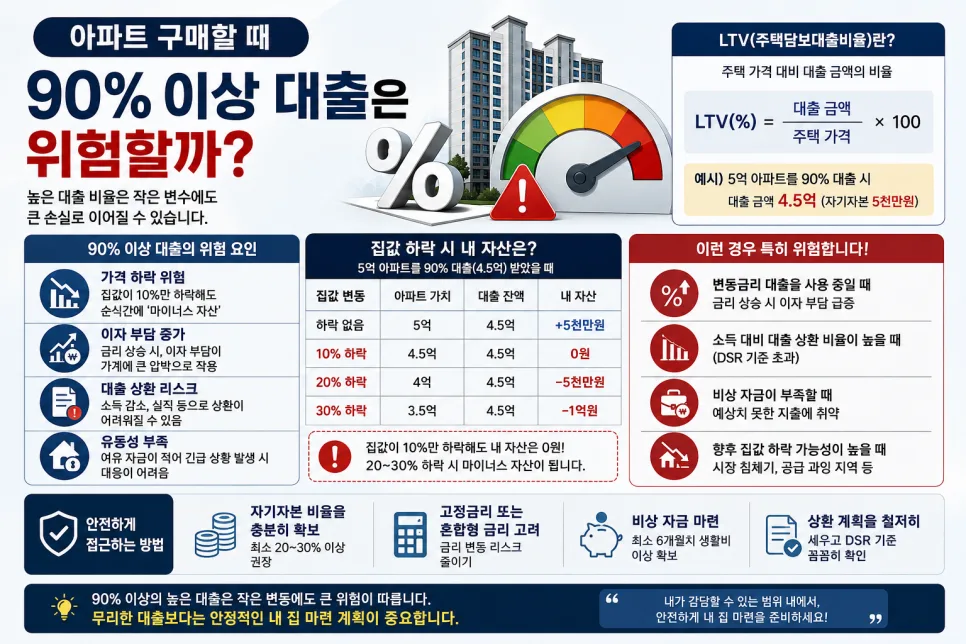

Taking out a mortgage for 90% or more of a home's value means you're putting down a very small down payment, often as little as 10%. This leaves you with very little equity in your home from the start. If property values decline even slightly, you could owe more on your mortgage than your home is worth, putting you in a negative equity position. This makes it difficult to sell or refinance your home later. Furthermore, a high monthly mortgage payment can strain your household budget, especially if interest rates rise or your income decreases unexpectedly. In the current economic climate of 2026, with potential for rate hikes and market volatility, these risks are amplified, making a high-LTV loan a precarious choice for many.

For example, consider a hypothetical buyer who purchased a $350,000 home with a 10% down payment ($35,000), taking out a $315,000 mortgage. If the housing market experiences a 5% downturn, their home's value drops to $332,500, but they still owe $315,000. If interest rates then increase, their monthly payments could jump significantly, potentially making it unaffordable. This scenario highlights how a small initial equity buffer can quickly turn into a major financial burden.

What Should You Consider With a 90%+ Mortgage?

If you're contemplating a mortgage with a high LTV, preparing for future financial uncertainties is paramount. Firstly, ensure you have a substantial emergency fund, ideally covering 6-12 months of living expenses, to cushion against unexpected job loss or income reduction. Secondly, be prepared for potential interest rate increases; explore fixed-rate mortgage options or understand how adjustable-rate mortgages (ARMs) might impact your payments over time. Thirdly, have a contingency plan for a potential decline in home values, understanding your options for selling or refinancing even in a down market. Lastly, create a detailed and realistic repayment schedule, factoring in potential increases in your monthly payments and exploring options for making extra payments to build equity faster. These preparations are vital for maintaining financial stability in a high-leverage situation.

Realistic Ways to Lower Your Mortgage Loan Ratio

Since a high loan-to-value ratio can be risky, actively working to reduce it is a smart financial move. The most straightforward approach is to increase your initial down payment. This could involve saving diligently for a longer period, seeking financial assistance from family members (like a gift for a down payment), or leveraging returns from investments. If immediate purchase is necessary, consider exploring lower-cost housing options or adjusting your desired location to find more affordable properties. Sometimes, delaying your home purchase slightly to accumulate more savings can significantly reduce your loan amount and associated risks, leading to a more manageable and secure homeownership experience.

Mistakes to Avoid When Buying a Home with a High Mortgage

When considering a home purchase with a high mortgage, such as 90% LTV, it's critical to avoid common pitfalls. A frequent mistake is overestimating your ability to repay, especially under rising interest rate scenarios. Always factor in potential increases in your monthly payments and ensure your budget can comfortably accommodate them, even with a slight decrease in income. Another common error is underestimating the risk of interest rate fluctuations; assuming rates will remain low indefinitely can lead to severe financial strain. Lastly, failing to consult with a qualified financial advisor or mortgage broker is a significant oversight. These professionals can provide personalized guidance, assess your financial situation accurately, and help you navigate the complexities of high-LTV mortgages, ensuring you make an informed decision that aligns with your long-term financial goals.

For more details, check the original source below.