In the US, an income tax refund occurs when you've paid more in taxes throughout the year than your actual tax liability. This commonly applies to freelancers, those with side hustles, or individuals who had taxes withheld incorrectly. For 2026, maximizing your refund means meticulously claiming all eligible deductions and understanding the filing process.

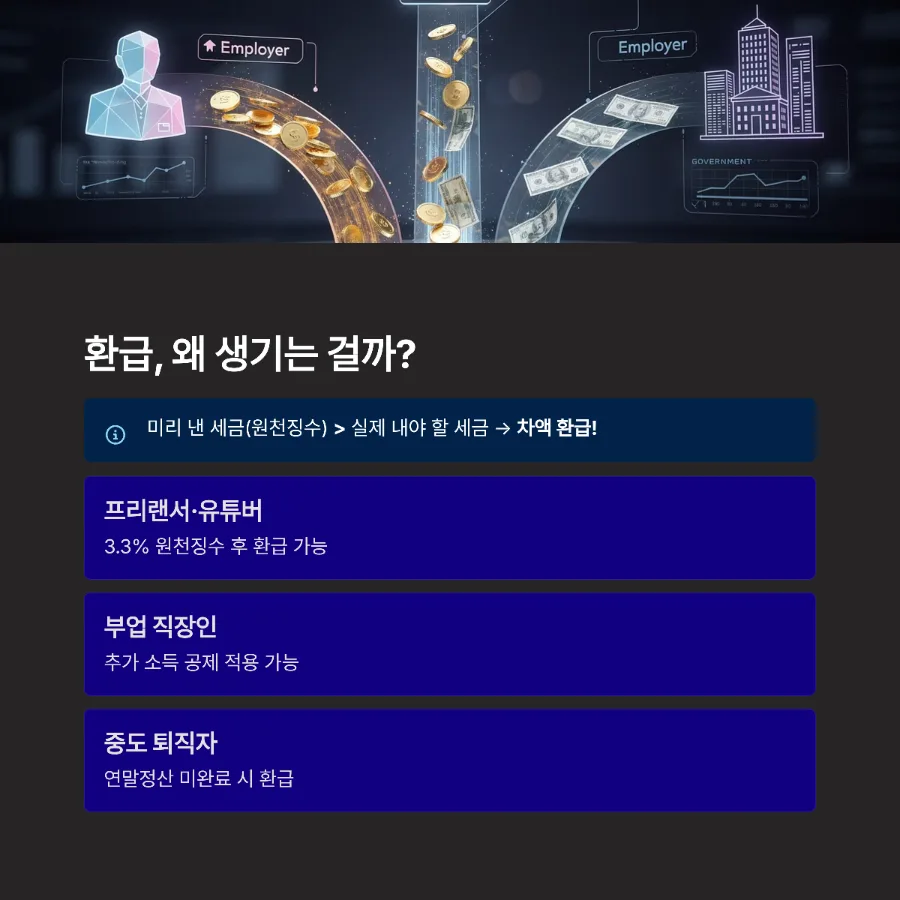

Why Do You Get an Income Tax Refund in the US?

An income tax refund is essentially the government returning overpaid taxes. In the U.S. system, taxes are often withheld from paychecks based on estimated annual income and tax brackets. If your actual income for the year is lower than estimated, or if you qualify for various tax credits and deductions, you might have overpaid. Freelancers, for instance, often have a flat 3.3% withheld from payments, which may not reflect their final tax rate after accounting for business expenses, deductions, and credits. Similarly, if you changed jobs mid-year and didn't adjust your W-4 form correctly, or if you have multiple income streams, you could end up overpaying. The annual tax filing process (typically due April 15th) is when these calculations are finalized, and any overpayment is refunded to you.

What Are the Key Deductions to Maximize Your Refund?

To significantly boost your tax refund, it's crucial to claim every eligible deduction and credit. For individuals, this includes deductions for health insurance premiums, life insurance, and other eligible insurance payments, often capped annually. Medical expenses can be deducted if they exceed a certain percentage (typically 7.5%) of your Adjusted Gross Income (AGI). Educational expenses for yourself, your dependents, or even certain family members can be deducted, including tuition, fees, and books, up to specific limits. Charitable donations to qualified organizations are also deductible, with limits based on your AGI. Furthermore, your use of credit cards, debit cards, and cash for everyday purchases can lead to deductions, especially if you utilize tax-advantaged accounts or specific spending categories. For homeowners, mortgage interest and property taxes can be significant deductions. If you're a freelancer or small business owner, meticulously tracking and deducting business-related expenses—such as home office costs, supplies, software subscriptions, travel, and professional development—is vital for reducing your taxable income and increasing your refund.

What Are the Steps for Filing Your Income Tax Refund Using the IRS System?

The primary way to file your U.S. federal income tax return and claim a refund is through the Internal Revenue Service (IRS) system, often via tax software or a tax professional. First, gather all necessary documents: W-2 forms from employers, 1099 forms for freelance or other income, receipts for deductible expenses, and records of any estimated tax payments made. You can file electronically using tax preparation software (like TurboTax, H&R Block, etc.) or hire a Certified Public Accountant (CPA) or Enrolled Agent. The software or professional will guide you through inputting your income, deductions, and credits. If you're filing a simple return, you might qualify for IRS Free File, which offers free online tax preparation services. Once all information is entered, the system calculates your tax liability and determines if you are due a refund. You can then choose to receive your refund via direct deposit (the fastest method) or a paper check. Ensure your bank account and routing numbers are accurate for direct deposit to avoid delays.

What Should You Watch Out For When Claiming a Tax Refund?

When claiming a tax refund, accuracy and timeliness are key. Double-check that all personal information, especially your Social Security number and bank account details for direct deposit, is entered correctly to prevent processing delays or returned payments. Be aware of the filing deadline (typically April 15th) and file an extension if necessary, though extensions to file are not extensions to pay any taxes owed. Keep meticulous records of all income statements and supporting documents for deductions and credits for at least three years (sometimes longer), as the IRS may request them for audits. Avoid inflating deductions or credits, as this can lead to penalties, interest, and even criminal charges. Even if your refund amount is small, it's still your money, so ensure you file to claim it. If your tax situation is complex, or you're unsure about eligibility for certain deductions or credits, consulting with a qualified tax professional is highly recommended to ensure you receive the maximum refund you're entitled to without issues.

English crawl path

Next English reads from this pilot cluster

Continue through the category hub, latest English stories, and related posts so this translated article is not an isolated URL.

Tags

💬Frequently Asked Questions

What should I check first in How to Get Your 2026 US Income Tax Refund: Deductions & Filing Guide?

Does this Finance article link back to the Korean source?

Where can I find similar English stories?

English discovery path

Explore more English K-culture stories

Keep browsing the indexed English pilot cluster so Google and readers can move between this story, the category hub, and fresh discovery pages.

Original Source

Read the Korean original