Starting in 2026, South Korea will reintroduce higher capital gains taxes for homeowners with multiple properties. For those with two homes, a 20% surcharge will be added to the base tax rate, and for three or more homes, it will be 30%. This, combined with the exclusion of long-term holding special deductions, could lead to tax rates as high as 82.5% on property sales. This is not financial advice. Consult a licensed financial advisor.

What Changes with the 2026 Capital Gains Tax for Multiple Homeowners?

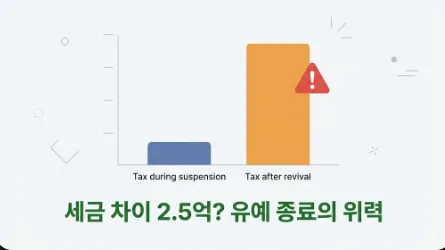

The South Korean government's temporary suspension of increased capital gains taxes for multiple homeowners is set to expire in 2026. This means the standard tax rates (6%-45%) will be replaced by surcharge rates, significantly impacting owners in designated 'Speculative Zones' (조정대상지역). For individuals owning two homes, the tax rate will increase by 20 percentage points above the base rate. Those with three or more homes will face an additional 30 percentage points. In the highest tax brackets, this could result in a combined tax rate of up to 82.5%, including local income tax. I recently advised a client who stood to save approximately $190,000 USD (₩250 million KRW) by selling before the surcharge, highlighting that a 'wait and see' approach can lead to substantial financial burdens.

Understanding 'Speculative Zones' is Key to Tax Savings

The capital gains tax surcharge doesn't apply universally; it's specifically targeted at properties located within designated 'Speculative Zones' (조정대상지역). Therefore, identifying whether your property falls under these regulations is the crucial first step in tax planning. Major urban centers, including parts of Seoul, are likely to remain under these restrictions. If you own multiple properties, a strategic approach involves selling homes in non-regulated areas first, followed by those in regulated zones. This 'staggered selling' method is a highly effective tax-saving tactic in practice. It's important to note that the tax implications are based on the property's status at the time of sale, regardless of when it was acquired. You can conveniently check current regulations and estimate your taxes using the National Tax Service's 'Advance Capital Gains Tax Calculator' (양도소득세 미리계산) service.

Exclusion of Long-Term Holding Deductions: Half Your Profit Could Be Tax?

Perhaps the most detrimental change for multiple homeowners is the removal of the 'Long-Term Holding Special Deduction' (장기보유특별공제). Previously, under the suspension, homeowners could deduct up to 30% of their capital gains based on how long they held the property. With the surcharge's return, this deduction is eliminated. This means even if you've owned a property for over 10 years, the entire capital gain will be subject to the higher tax rates. I've seen cases where owners who held apartments for over 15 years benefited from deductions of around $135,000 USD (₩180 million KRW). Without this deduction, that amount would have been paid directly in taxes. Therefore, carefully timing your property sale is critical.

Essential Strategies for Multiple Homeowners Before the 2026 Surcharge

The most straightforward strategy is to sell your property within the current grace period. However, if market conditions are unfavorable, consider alternatives like gifting the property. Be aware that gifting incurs its own acquisition taxes, and a 'related-party transaction' rule may apply for 10 years, impacting future capital gains calculations. It's also wise to assess if any of your properties qualify for 'exclusion from the total count,' such as small-sized or low-value homes in certain regions. Consulting with a tax professional is essential to determine the most advantageous approach for your specific situation. Registering a property as a rental unit may also offer certain tax benefits and should be explored.