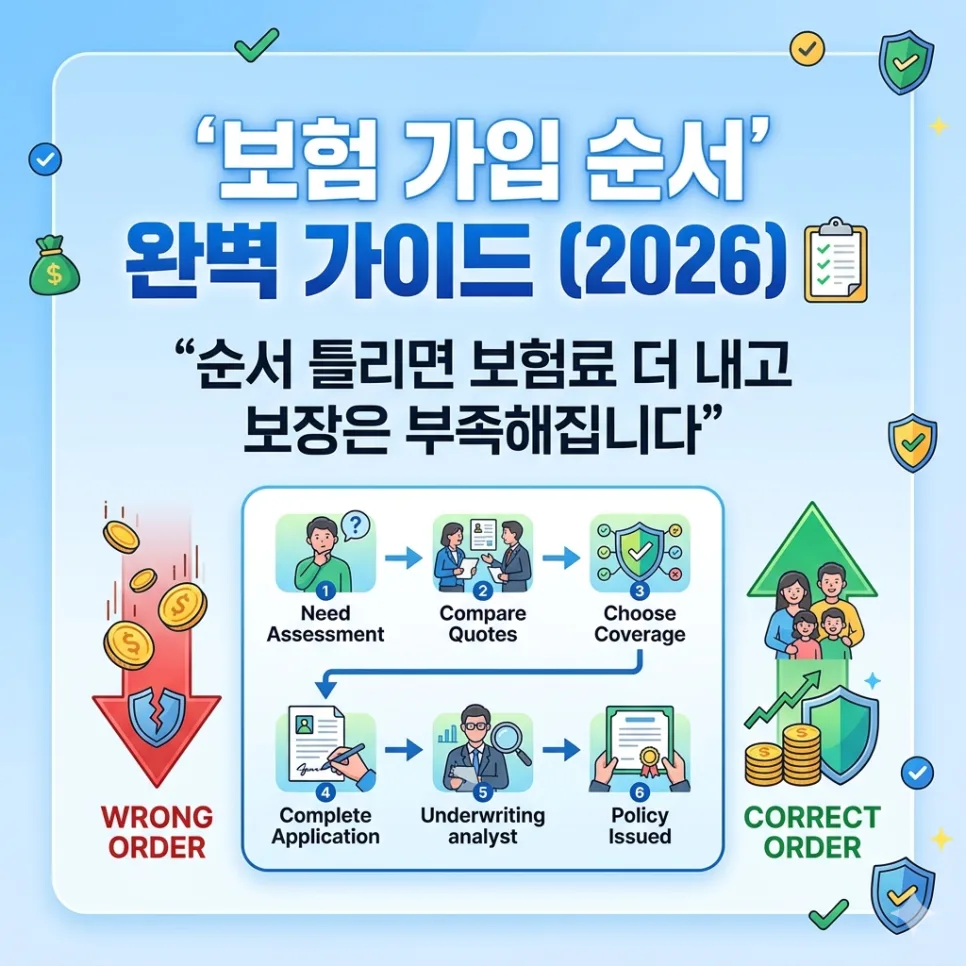

Many people miss the crucial order when buying insurance, leading to wasted premiums and gaps in essential coverage. The efficiency of your entire insurance plan hinges on which policies you prioritize. For 2026, a smart strategy remains: start with medical expense insurance, followed by critical illness coverage, and then driver's insurance. This approach ensures you're covered for immediate risks before focusing on long-term savings.

What's the Top Priority for Insurance in 2026?

The absolute first and most essential insurance to secure is medical expense insurance, often called '실비보험' (Silbi Insurance) in Korea. This policy covers actual medical costs incurred, significantly reducing your out-of-pocket expenses for any illness or accident. Countless individuals share stories of how this coverage saved them from severe financial hardship during unexpected hospital stays. It forms the bedrock of any insurance plan, alleviating anxiety about medical bills. Without it, even minor illnesses can lead to substantial financial strain, making it the highest priority.

What Core Coverage Should You Get After Medical Insurance?

Once you've secured basic medical expense coverage, the next step is to prepare for significant financial outlays associated with critical illnesses. Conditions like cancer, stroke, or heart disease can require extensive treatment periods and incur high medical costs. Critical illness insurance provides a lump sum payment upon diagnosis, which is invaluable for covering treatment, rehabilitation, and living expenses during recovery. Many have successfully navigated serious diagnoses and focused on healing thanks to the financial cushion provided by this type of coverage. Therefore, after establishing your medical expense insurance, robust critical illness protection is vital.

What Insurance is Essential for Drivers?

If you drive, preparing for potential legal liabilities arising from traffic accidents is crucial. Standard auto insurance alone may not fully cover all legal responsibilities, such as fines, settlement costs, or attorney fees. Driver's insurance (운전자보험) complements auto insurance by covering these specific areas. It can help with fines, facilitate settlements with victims, and cover legal defense costs. There are numerous accounts of individuals navigating severe accident situations and mitigating legal and financial burdens with the help of driver's insurance. Thus, alongside your auto policy, securing driver's insurance is a wise move for anyone on the road.

What Common Mistakes Should You Avoid When Buying Insurance?

A frequent error people make is prioritizing savings or annuity-type insurance over essential protection policies. Focusing solely on future wealth accumulation without addressing immediate risks can leave you financially vulnerable if illness or an accident strikes. Other common mistakes include duplicating coverage you don't need or paying high premiums for inadequate benefits. These errors can undermine your entire insurance strategy, leading to inefficient spending. Therefore, always structure your insurance portfolio with 'protection' as the primary goal, and consider savings or annuity products only after securing necessary coverage. Tailoring your policy to your specific needs is key to effective financial planning.

For more detailed insurance strategies, check the original source below.