By September 2026, converting your existing Korean housing subscription savings account to the comprehensive type offers expanded opportunities for both public and private housing applications, a 40% income tax deduction on up to ₩3 million (approx. $2,200) in annual contributions, and a potential interest rate reduction of up to 0.5% on the Didimdol loan. This conversion is a limited-time opportunity for existing account holders to maximize their homeownership benefits.

Why Convert Your Existing Housing Subscription Account to a Comprehensive Savings Plan by 2026?

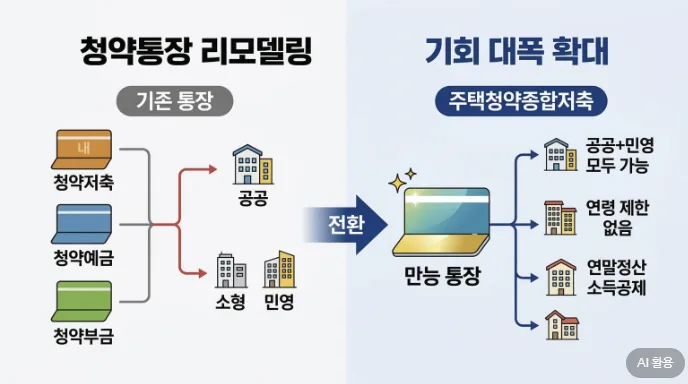

Historically, applying for public and private housing in Korea required separate subscription accounts, creating an inconvenient system for aspiring homeowners. The introduction of the comprehensive housing subscription savings account (주택청약종합저축) unified these options, allowing applicants to apply for all types of housing with a single account. Crucially, the window to convert existing, older account types (like 청약예금, 부금, or 저축) into this comprehensive plan is closing in September 2026. Failing to convert means potentially missing out on broader housing market access and missing out on significant tax and loan benefits. Existing contributions and subscription periods are recognized upon conversion, ensuring no loss of priority in the application process.

What Are the Specific Benefits of Converting to a Comprehensive Housing Subscription Savings Account?

The most significant advantage of converting to a comprehensive housing subscription savings account is the expanded eligibility for housing applications. While older accounts were restricted to either public or private housing, the comprehensive plan allows applications for both. For eligible individuals—typically heads of households with an annual income below ₩70 million (approx. $50,000 USD) and a total household income below ₩100 million (approx. $72,000 USD)—contributions up to ₩3 million (approx. $2,200 USD) per year are eligible for a 40% income tax deduction. This can translate to a tax refund of up to approximately ₩720,000 (approx. $520 USD) during year-end tax settlements. Furthermore, holders can receive preferential interest rates on the 'Didimdol Loan' (내집마련 디딤돌 대출), a government-backed mortgage for first-time homebuyers. Depending on the duration of the comprehensive account, interest rates can be reduced by 0.3% for 5+ years of membership, 0.4% for 10+ years, and up to 0.5% for 15+ years.

When Is the Deadline for Conversion, and What Should You Be Aware Of?

The deadline to convert your existing housing subscription account to the comprehensive type is September 2026. After this date, no further conversions will be permitted. The conversion process can be initiated by visiting a bank in person with your identification or conveniently done online through your bank's mobile application. It's important to note that accounts with a prior successful housing application (i.e., you've already won a housing lottery) are ineligible for conversion. The new eligibility and benefits take effect from the date of conversion, so ensure your circumstances meet the requirements at that time. For precise details tailored to your situation, consulting directly with your financial institution is highly recommended.

Don't miss out—convert your account today!