Considering the Korean Growth Fund (국민성장펀드) in 2026? Key benefits include government-backed loss protection up to 20% and significant tax savings. However, be aware of the 5-year lock-up period, making it a commitment for long-term investors with surplus funds.

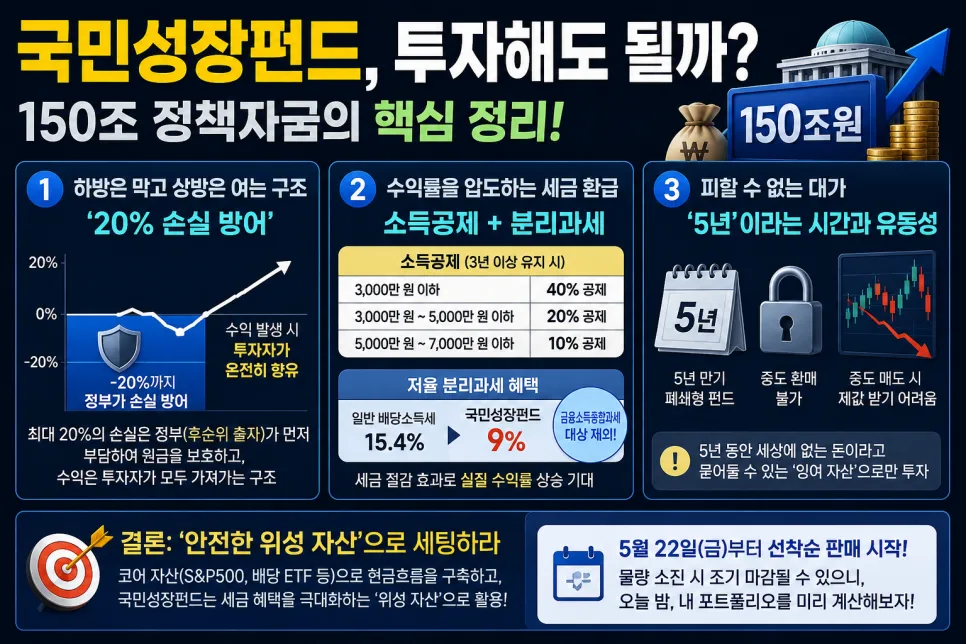

How Does the Korean Growth Fund's 20% Loss Protection Work?

A major draw of the Korean Growth Fund is its government backing, which acts as a junior investor. This means if the fund experiences losses, the government's capital absorbs up to 20% of the deficit first. This structure significantly reduces your personal risk of losing your initial investment and helps stabilize your overall portfolio. Importantly, any profits generated by the fund are fully retained by the investor. This downside protection is particularly appealing in uncertain market conditions, offering a sense of security for those seeking stable investment growth.

What Are the Tax Benefits of Investing in the Korean Growth Fund?

As a policy-driven fund, the Korean Growth Fund offers substantial tax advantages designed to boost investor returns. If you hold the fund for three years or more, you can claim income deductions of up to 40% on your contributions. For example, contributions up to approximately $22,000 (30 million KRW) are eligible for the full 40% deduction, leading to significant year-end tax refunds. Furthermore, dividends earned from the fund are taxed at a preferential rate of 9%, much lower than the standard 15.4% income tax rate. These dividends are also exempt from comprehensive income tax assessments, making the fund a highly attractive option for long-term wealth accumulation and tax efficiency.

Understanding the 5-Year Lock-Up for the Korean Growth Fund

The attractive benefits of the Korean Growth Fund come with a significant trade-off: a 5-year maturity period with no option for early withdrawal. If you need access to your funds before the 5-year mark, you must sell your shares on the stock exchange. This process carries a risk, as low trading volume could prevent you from selling at full market value. Therefore, it's crucial to only invest funds you can afford to have tied up for the entire 5-year term. This fund is best suited for investors whose primary goal is long-term capital appreciation and who have a clear understanding of their cash flow needs over the next half-decade.

Common Mistakes When Investing in the Korean Growth Fund

A frequent pitfall for investors is succumbing to FOMO (Fear Of Missing Out) and investing impulsively without considering their personal financial situation or the fund's liquidity constraints. The allure of government backing and high tax benefits can overshadow the critical 5-year lock-up period. Many investors later find themselves in a bind when unexpected expenses arise. Before investing, it's essential to determine the appropriate allocation for this fund within your overall investment portfolio and confirm that you won't need this capital for at least five years. Carefully calculating your contribution amount to maximize income deduction benefits without overcommitting is also a wise strategy.

For more details, check the original source below.