Confused about IRP and ISA accounts? In 2026, understanding their differences is key for maximizing tax savings. While ISA accounts offer limited tax benefits on individual stock trades, they shine when investing in dividends or overseas ETFs listed on Korean exchanges. IRP accounts, on the other hand, provide significant tax credits and lower income tax rates upon retirement, making them powerful long-term savings vehicles.

What's the Difference Between IRP and ISA Accounts in 2026?

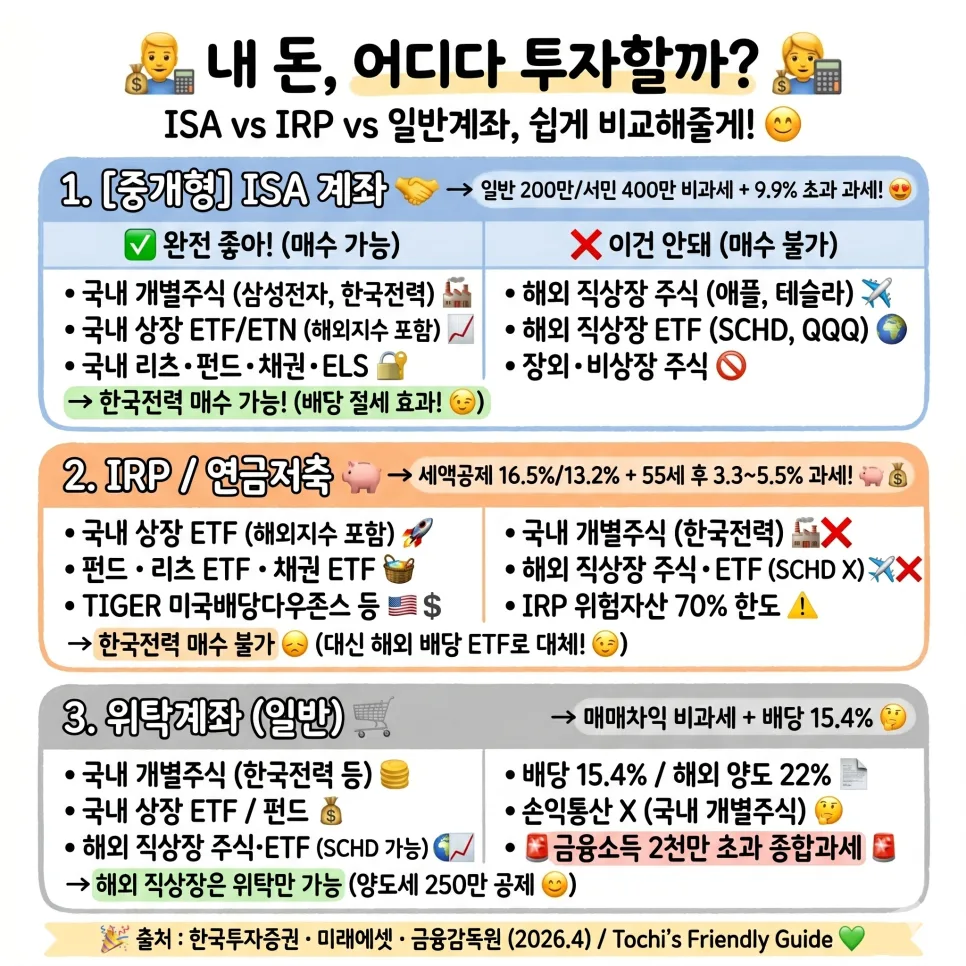

Many individuals utilize both ISA (Individual Savings Account) and IRP (Individual Retirement Pension) accounts but often misunderstand their distinct benefits. An ISA offers tax benefits on net profits up to ₩2 million (approx. $1,500 USD), with a 9.9% separate tax rate on amounts exceeding this. However, since individual stock trades are already tax-exempt in Korea, the ISA's advantage here is limited. Its real strength lies in tax savings on dividends from Korean stocks or investments in overseas ETFs listed on Korean exchanges. For instance, holding individual stocks like Korea Electric Power Corporation (KEPCO) for dividends could yield around ₩770,000 (approx. $570 USD) in tax savings over 10 years with an ISA. Therefore, if you plan to hold dividend stocks long-term, an ISA is a strong contender. Keep in mind that ISA benefits are contingent on fulfilling a minimum 3-year lock-up period.

How Do IRP and ISA Tax Benefits Differ for ETF Investments?

The tax implications for high-dividend ETFs vary significantly between IRP and ISA accounts when traded on Korean exchanges. Consider an annual profit of ₩1 million (approx. $740 USD) from an ETF, comprising ₩600,000 (approx. $440 USD) in capital gains and ₩400,000 (approx. $300 USD) in dividends. In a standard brokerage account, these dividends would incur a 6.16% tax. However, an ISA account offers tax exemption on these dividends. IRP and Pension Savings accounts defer taxes on investment gains until retirement, applying a lower tax rate of 3.3% to 5.5%. Additionally, they offer an annual tax credit of up to ₩990,000 (approx. $730 USD). While an ISA might appear more advantageous based solely on immediate returns, the long-term tax-free income and tax credits from an IRP or Pension Savings account often make them superior for overall wealth accumulation. However, if your total tax liability is low, an ISA might still be the more beneficial option.

What Products Can I Invest in with an IRP Account, and What Are the Limits?

You cannot directly purchase Korean individual stocks, such as KEPCO, within an IRP account. However, you can invest in Korean-listed ETFs, mutual funds, and certain bond or REIT-based products. Direct investments in foreign stocks or ETFs, as well as leveraged or inverse ETFs, are generally restricted. The combined annual tax credit limit for IRP and Pension Savings accounts is ₩9 million (approx. $6,660 USD). The tax credit rate is 16.5% for those with a total annual income below ₩55 million (approx. $40,700 USD) and 13.2% for those earning above this threshold. This means you can receive a maximum tax credit of up to ₩1.485 million (approx. $1,100 USD) on your contributions. Note that there are separate limits for the total annual contribution to all retirement accounts.

SCHD Direct Investment vs. Tracking ETF: Which is Better for Tax Savings?

If you wish to invest directly in the U.S.-listed ETF SCHD, you must use a standard brokerage account, as it cannot be purchased through ISA or IRP accounts. However, ETFs that track SCHD and are listed on Korean exchanges (e.g., TIGER US Dividend Growth ETF, KODEX US Dividend Growth ETF) can be bought within ISA and IRP accounts. This allows you to benefit from the lower retirement income tax rates (3.3% to 5.5%) applicable upon withdrawal from your pension accounts.

What is the Financial Income Comprehensive Tax Threshold for Brokerage Accounts?

If your total annual financial income (interest and dividends) exceeds ₩20 million (approx. $14,800 USD), you may be subject to the Financial Income Comprehensive Tax. To avoid this, consider diversifying your investments or utilizing tax-advantaged accounts like ISAs and pension accounts to leverage their tax-saving benefits. This strategy is crucial for managing your tax burden effectively in 2026.

For more details, check the original source below.