You pay your insurance premiums diligently, only to be told your claim is denied when you need it most. Simply having insurance doesn't guarantee payouts; you must understand the policy's terms and conditions, especially exclusion clauses. In 2026, understanding the top 5 reasons for claim denial can help you reduce your risk. This guide breaks down common pitfalls like disclosure violations, exclusion periods, and policy exclusions.

Top 5 Reasons for Insurance Claim Denials in 2026?

Insurance claim denials are more common than you might think. They often stem from a combination of factors, including failure to disclose information during application, policy exclusion periods, non-covered items, missed premium payments, and unclear causal links between an event and the policy terms. With potential changes to some insurance policies and regulations in 2026, it's crucial to grasp the specifics of your policy at the time of application. Personal experience shows that even minor undisclosed symptoms can lead to significant issues later. Therefore, transparency during the application process and a thorough review of your policy terms before filing a claim are essential habits.

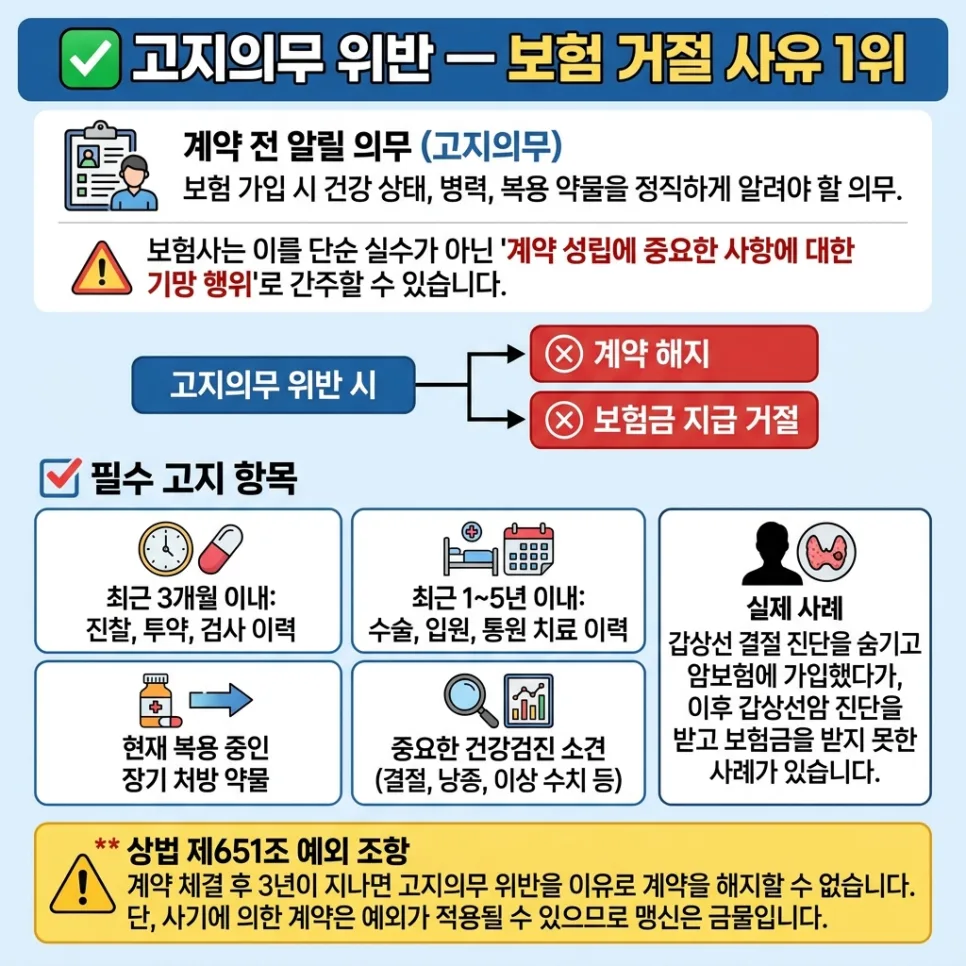

Is Failure to Disclose Information at Application the Biggest Cause of Claim Denial?

Violating the 'duty to disclose' during the insurance application process is one of the most frequent reasons for claim denial. This occurs when you provide inaccurate information about your health status, past medical history, or current medications, or omit crucial details. Insurers may consider this a misrepresentation or concealment of material facts, leading to contract termination or claim denial. Specifically, you must accurately report recent medical examinations, treatments, prescriptions, hospitalizations, and significant findings from health check-ups. For example, if you don't disclose a thyroid nodule found during a check-up and later get diagnosed with thyroid cancer, your claim could be denied. While the law generally protects against policy termination for disclosure violations after three years, intentional fraud can lead to exceptions, so caution is advised.

What Are Exclusion and Reduction Periods, and When Are Claims Limited?

Most insurance policies have an 'exclusion period' or 'reduction period' immediately after enrollment, during which payouts are limited or unavailable. For instance, many cancer insurance policies have a 90-day exclusion period from the policy's start date, meaning cancers diagnosed within this timeframe are not covered. Some life insurance policies might only pay 50% of the death benefit if the insured passes away within the first two years. These periods vary significantly by policy type and insurer. It's vital to consult your policy documents to understand the exact duration and scope of these limitations. For example, the 5th generation of Korean private health insurance (effective May 6, 2026) has adjusted co-payment rates for non-covered services and excluded certain treatments like physical therapy and non-covered injections, making it crucial to know which generation of policy you hold.

What Are Non-Covered Exclusions in Policy Terms?

Every insurance policy has specific exclusions listed in its terms and conditions. Failing to review these can lead to claim rejections. For example, with private health insurance, 'arbitrary non-covered services' not recognized by the health insurance review agency are typically not covered. Dental and traditional Korean medicine treatments are generally only covered for their 'covered' (급여) components, with non-covered (비급여) services excluded. Mental health conditions often have limited coverage, with non-covered aspects rarely paid out. Over-treatment (e.g., excessive physical therapy or cataract surgery claims) and accidents occurring while engaging in high-risk activities or failing to report changes in occupation can also lead to claim denial. The 5th generation of Korean private health insurance, effective May 6, 2026, increased co-payments for non-critical non-covered services from 30% to 50% and excluded certain treatments, reinforcing the need to verify your policy's generation.

How Can You Prevent Insurance Lapses Due to Unpaid Premiums?

If you fail to pay your insurance premiums for two consecutive months, your policy can lapse, rendering you unable to claim benefits. While lapsed policies can often be reinstated within a specific period (usually three months) through a 'reinstatement application,' the premium rate and policy terms at the time of reinstatement may apply. Common reasons for non-payment include insufficient funds in your auto-debit account or expired credit card information. Regularly check your auto-debit account balance and promptly update your payment information with the insurer if your card details change. If you receive a missed payment notification, address it immediately. Missing renewal deadlines can also make reinstatement more difficult, so it's important to manage your premium payments carefully.

How to Prove Causation for Insurance Claim Denials?

To receive an insurance payout, you must demonstrate a clear causal link between the incident (accident or illness) and the policy's coverage terms. For instance, if you didn't disclose taking medication for high blood pressure, a claim for a broken bone from a traffic accident might still be paid. However, if a pre-existing condition is deemed to be a significant contributing factor to a new illness, the insurer may deny or partially pay the claim. If your claim is denied, first request a written explanation from the insurer detailing the reason and relevant policy clauses. You can then submit additional medical records from your primary physician to establish causation, file a dispute with the Financial Supervisory Service, or consult a claims adjuster for a review. Given that claim outcomes can vary based on individual circumstances, seeking professional advice is recommended.

English crawl path

Next English reads from this pilot cluster

Continue through the category hub, latest English stories, and related posts so this translated article is not an isolated URL.

Tags

💬Frequently Asked Questions

What constitutes a disclosure violation when applying for insurance?

What is the exclusion period in insurance, and when are claims limited?

What should I do if my insurance claim is denied?

English discovery path

Explore more English K-culture stories

Keep browsing the indexed English pilot cluster so Google and readers can move between this story, the category hub, and fresh discovery pages.

Original Source

Read the Korean original