As of 2026, the optimal time to purchase annuity insurance is determined not by age, but by an individual's income stability and long-term retention capability. While early enrollment generally maximizes compound interest effects, making excessive payments can lead to early termination and potential financial loss.

When is the Best Time to Enroll in Annuity Insurance? 2026 Analysis

Annuity insurance is a financial product designed for long-term retirement planning, and the enrollment timing significantly impacts its returns. Enrolling early allows for a longer payment period, reducing the burden of monthly payments and maximizing the compound interest effect. For example, starting monthly contributions of $75 (approx. ₩100,000) in your 20s can lead to substantial retirement income by your 60s. Conversely, achieving the same retirement income goal in your 40s or 50s would require significantly higher monthly payments or might be difficult to attain. However, simply enrolling early isn't always the best strategy. Annuity insurance often requires a minimum 10-year commitment to fully benefit from tax advantages. Therefore, it's crucial to enroll only when you have a stable financial situation that allows for consistent payments. Many experts emphasize 'retention capability' as a more critical factor than the enrollment timing itself.

What Should Be Considered When Enrolling in Annuity Insurance by Age Group?

Considerations for enrolling in annuity insurance vary by age group. Individuals in their 20s and 30s benefit from a longer payment period, allowing for lower monthly contributions and long-term compound growth. Starting even small, consistent payments during this period can lay the foundation for retirement readiness. In their 40s, retirement planning becomes more serious. This is a time to assess existing assets and retirement needs, using annuity insurance to supplement any shortfalls. If you have accumulated a certain level of assets, you might consider increasing monthly payments or opting for short-term payment plans. For those in their 50s and beyond, the shorter payment period may limit compound interest benefits, making lump-sum or short-term payment options potentially more attractive for quickly building retirement funds. However, the penalties for early termination are significant, requiring a cautious approach. Regardless of age, the key is to enroll within your means, considering your current income and future cash flow, without overextending financially.

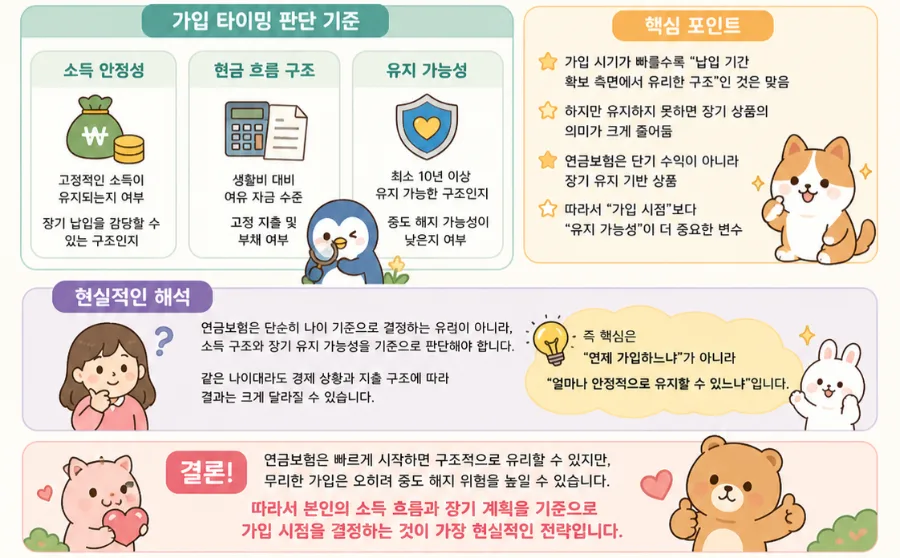

What Criteria Should Be Used to Determine Annuity Insurance Enrollment Timing?

The most critical factors for deciding when to enroll in annuity insurance are 'income stability' and 'retention capability.' First, assess whether you have a steady, reliable income stream currently and if it's likely to continue for the foreseeable future. This will help determine if you can afford to make consistent monthly payments for an extended period (at least 10 years). It's also important to analyze your current spending habits, fixed expenses (like loan repayments), and potential for unexpected costs to understand your available discretionary funds. Simply enrolling due to a 'need for retirement planning' without considering your financial capacity can increase the risk of early termination. Terminating an annuity early may result in receiving less than your principal investment or facing a 16.5% other income tax. Therefore, thoroughly analyzing your cash flow before enrollment and ensuring you can maintain payments for at least 10 years is essential.

Common Mistakes to Avoid When Enrolling in Annuity Insurance

The most frequent mistake people make with annuity insurance is focusing solely on the 'enrollment timing' while neglecting the 'retention capability.' Many individuals fail to understand the complex structure of these products and enroll without a clear grasp of their terms. Others select products that don't align with their financial situation or long-term goals. It's also common to underestimate the impact of early termination penalties, which can include principal loss and a 16.5% other income tax. Before signing up, it's crucial to review the early termination refund rates and potential tax implications. Additionally, not comparing different annuity products and their features—such as guaranteed interest rates, investment options, and fee structures—can lead to choosing a suboptimal plan.

For more details, check the original source below.