Considering switching to the 5th generation of Korean private health insurance (Silson) launching May 6, 2026? While it promises lower premiums, it also comes with reduced coverage for non-essential medical services. This guide breaks down the key changes, compares it to older generations, and helps you decide if switching is the right move for your healthcare needs and budget.

What Generation Is My Korean Health Insurance?

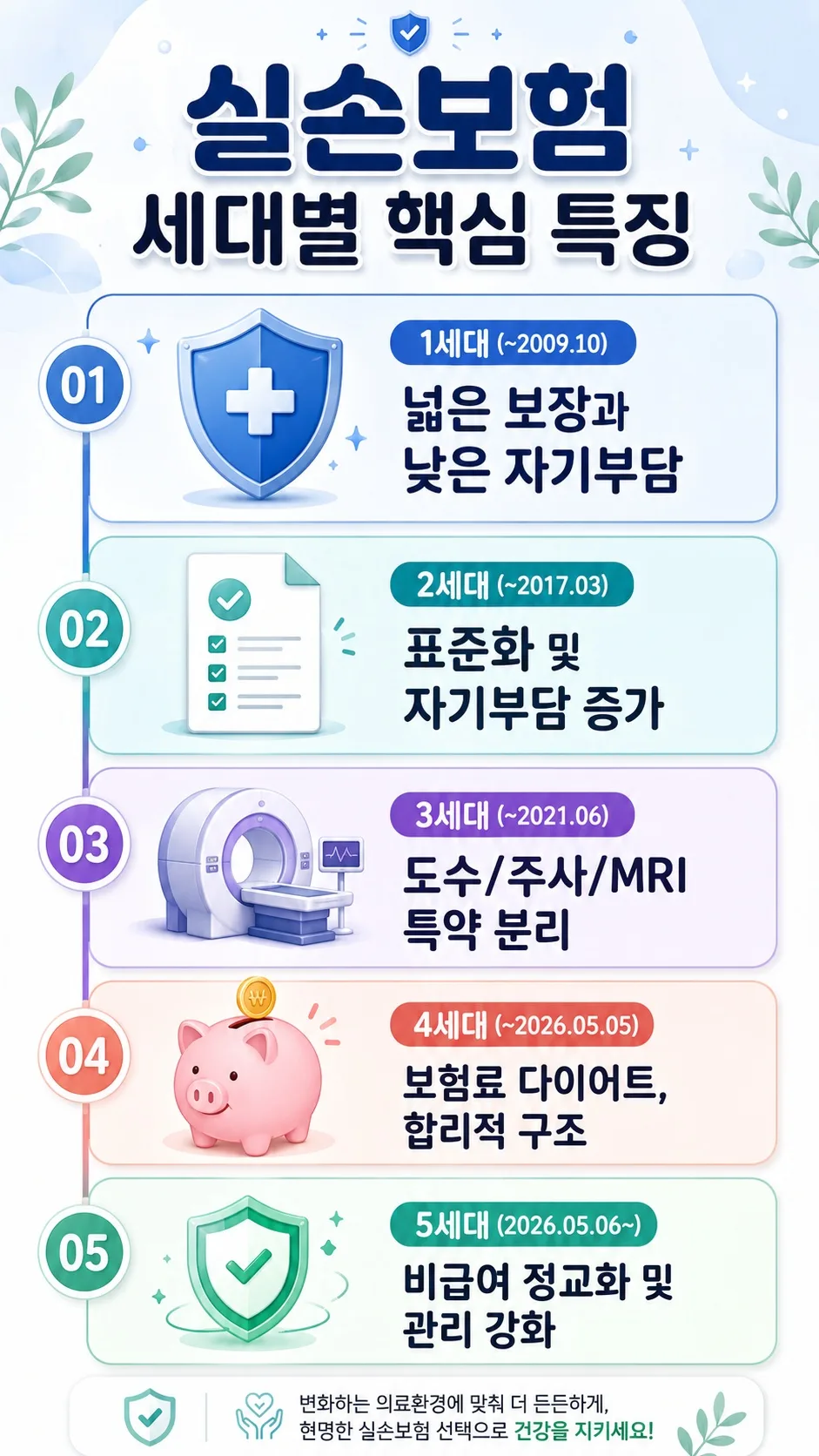

Before deciding on the 5th generation, it's crucial to know which generation of Korean private health insurance (Silson) you currently have. Generally, the 3rd generation was sold from April 2017, the 4th from July 2021, and the upcoming 5th generation will be available starting May 6, 2026. Older generations (1st and 2nd) have more variation, but checking your insurance policy's issue date is the most accurate way to determine your current generation. While older generations offer broader coverage with lower deductibles, they come with higher premiums. Newer generations tend to lower premiums but tighten controls on non-essential (non-benefit) medical services and increase deductibles. Therefore, instead of just looking at premium reductions, it's vital to first understand how your frequently used non-essential services will be covered under the 5th generation.

5th Gen Korean Health Insurance vs. 4th Gen: Key Changes

Related Articles

The 5th generation of Korean private health insurance introduces several key differences compared to the 4th generation. Firstly, the co-payment for essential (benefit) medical services during outpatient visits will now align with the national health insurance co-payment rate, resulting in a minimum deductible of 20% or approximately $7-14 USD (10,000-20,000 KRW), whichever is greater. Secondly, non-essential (non-benefit) coverage will be split into severe and non-severe categories. Non-severe non-benefit services will have a reduced annual coverage limit of $7,000 USD (10 million KRW), with a higher deductible of 50% or $35 USD (50,000 KRW), whichever is greater, for both inpatient and outpatient care. Thirdly, while severe non-benefit services largely retain their existing framework, a new annual out-of-pocket maximum of $3,500 USD (5 million KRW) will apply for inpatient care at comprehensive and general hospitals. Finally, essential medical costs related to pregnancy, childbirth, and developmental disorders are newly covered, though specific conditions and enrollment periods may apply. These changes mean the 5th generation could feel like a coverage reduction for those frequently using minor non-essential services, but potentially offer enhanced protection for severe conditions requiring extensive treatment.

Will Manual Therapy, Non-Benefit Injections, or MRIs Be Covered Under the 5th Gen?

Coverage for services like manual therapy, non-benefit injections, and MRIs under the 5th generation of Korean private health insurance requires careful consideration. In the 5th generation, services such as musculoskeletal physical therapy, extracorporeal shockwave therapy, and non-benefit injections are classified as non-severe non-benefit items. This means their coverage limits and deductibles will differ from previous generations. If you frequently utilize these treatments, the reduction in coverage might outweigh the premium savings. While MRIs and MRA scans are not explicitly excluded in the 5th generation, they are likely to be categorized under non-severe non-benefit services, potentially leading to reduced coverage. Before making a switch, it is essential to thoroughly review the policy details and terms of the specific 5th generation plan you are considering to understand the exact scope of coverage.

5th Gen Korean Health Insurance: Switch or Stay? A Decision Guide

The decision to switch to the 5th generation of Korean private health insurance hinges on your personal healthcare spending patterns. If you frequently visit doctors and utilize non-essential services like manual therapy or non-benefit injections, sticking with your current plan might be more beneficial, as the potential reduction in coverage could outweigh the premium savings. However, if you are generally healthy and believe the risk of incurring high medical costs from major illnesses or accidents is low, transitioning to the 5th generation could be a smart move to lower your insurance premiums. When considering a switch, it's crucial to compare the coverage details of the 5th generation plan with your current policy and your anticipated medical needs. Consulting with a financial advisor or insurance specialist is highly recommended to make the best decision for your individual circumstances.

For more details on the 5th Gen Korean health insurance switch, check the original source below.