As of April 25, 2026, the US stock market is showing a clear upward trend, particularly in tech stocks. This guide details a strategy for leveraging this growth to increase your assets, including specific investment allocations and the use of margin loans to amplify your portfolio. We'll explore how to strategically deploy capital to maximize returns in the current market environment.

Why Consider Leverage in the 2026 US Stock Market?

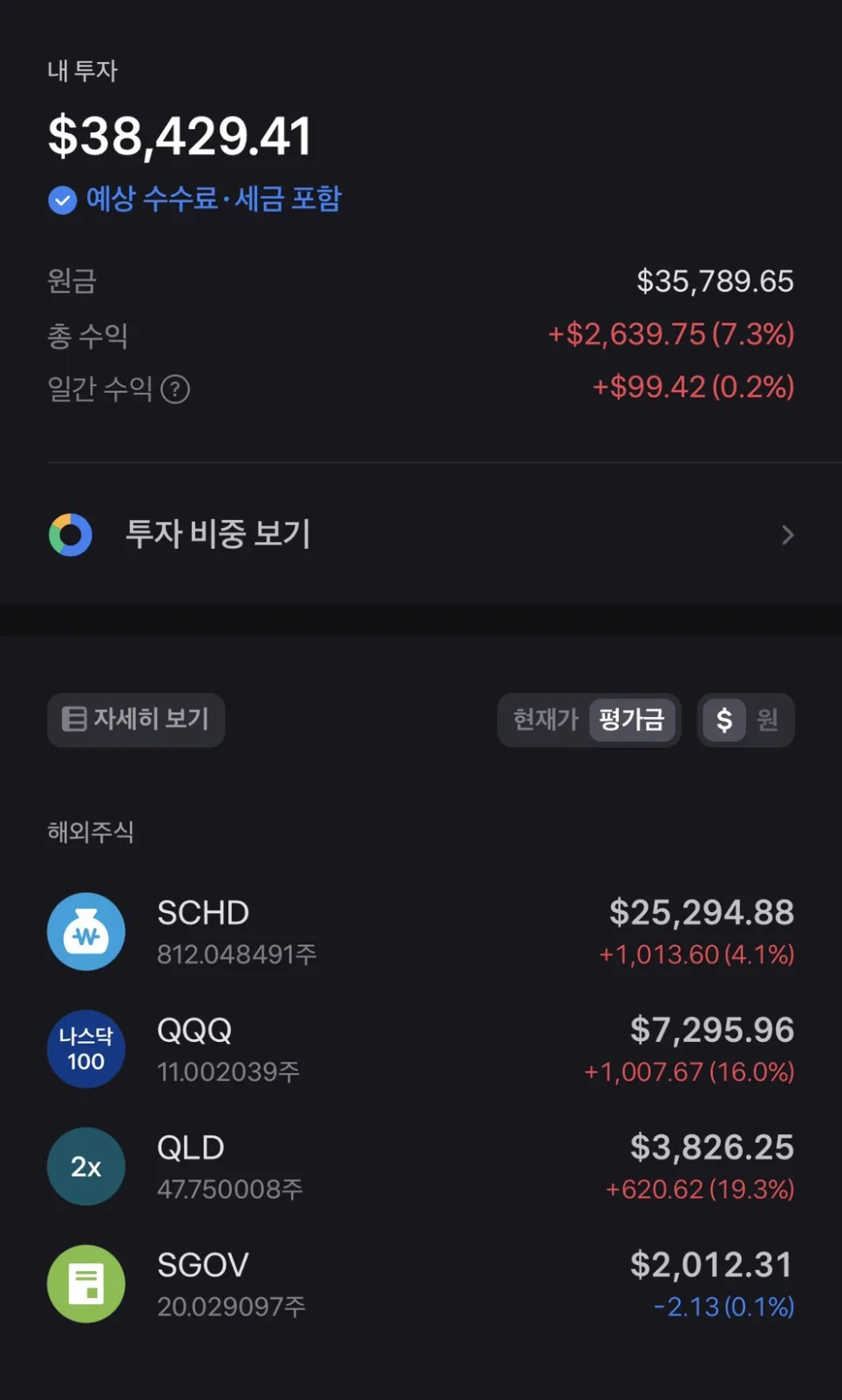

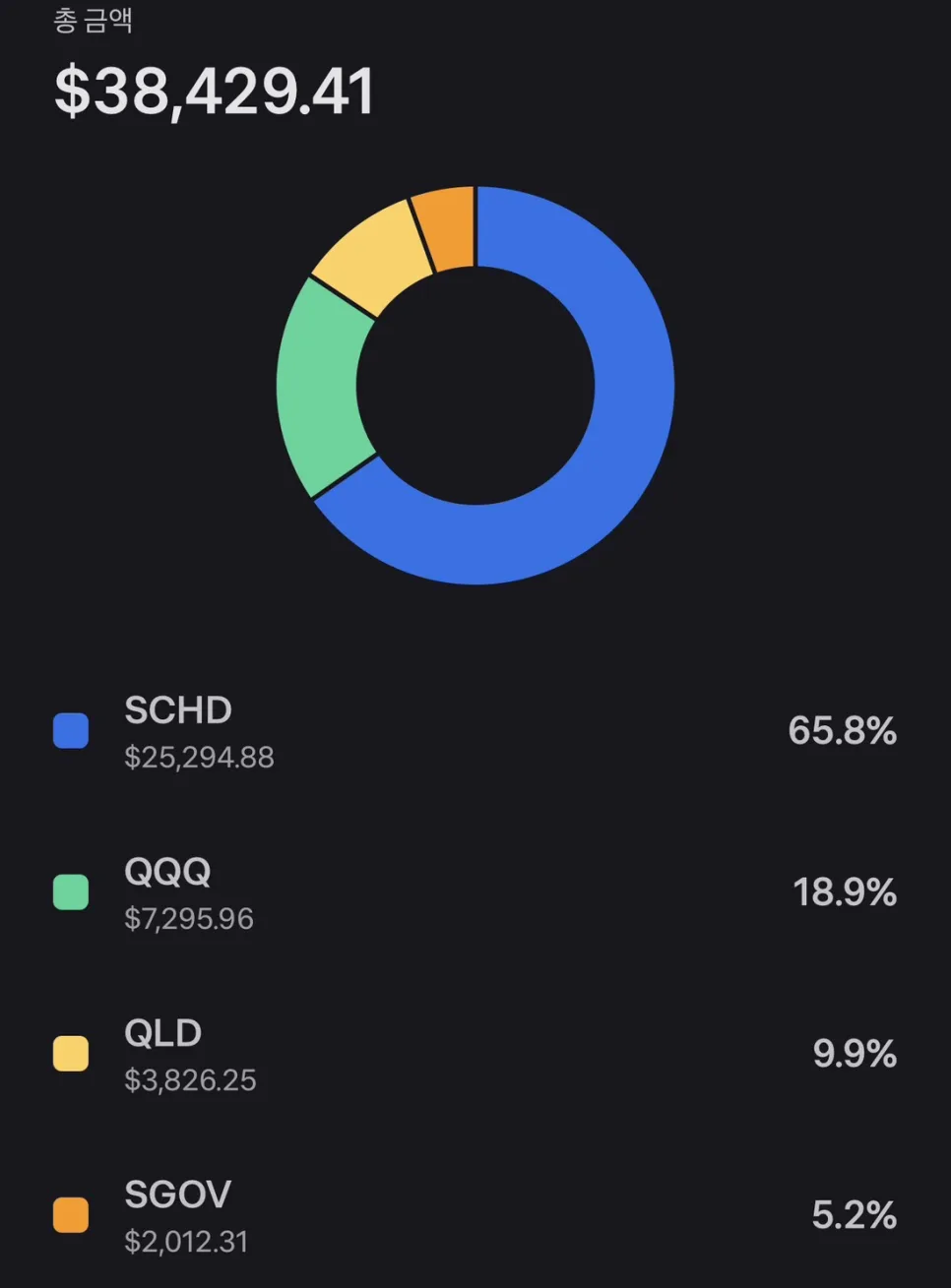

The US stock market, especially the Nasdaq, is experiencing a notable rally, fueled by optimism around potential peace in global conflicts and a strong outlook for technology companies. This has led to significant price increases in tech-focused ETFs like SOXL. While I previously held SOXL, I've since shifted my strategy to focus on long-term asset growth and efficient capital deployment. I'm currently increasing my holdings in SGOV, a Treasury bill ETF, to strategically manage my dollar assets and generate returns, rather than simply holding cash. This approach aims to actively grow wealth rather than passively letting it sit idle, especially considering inflationary pressures.

Detailed Investment Plan Using Margin Loans

My current systematic automated buying strategy involves investing $48 per day, allocated as $18 to SCHD (Schwab U.S. Dividend Equity ETF), and $15 each to QQQ (Invesco QQQ Trust) and QLD (Direxion NASDAQ-100 Equal Weight Index 1x Shares). This amounts to approximately $1,056 per month (around $1,600 USD). To accelerate asset growth, I plan to increase this daily investment to $85 ($35 for SCHD, $30 for QQQ, and $20 for QLD), totaling about $1,870 per month (around $2,800 USD). This represents a roughly 77% increase in monthly investment. Utilizing a margin loan (similar to a home equity line of credit or personal line of credit) is a calculated risk to boost returns in an environment where asset appreciation is expected, helping to combat inflation and enhance growth potential.

Margin Loan vs. Personal Loan for Investment Leverage

The decision to use a margin loan for investment is not solely about chasing high returns; it's about optimizing my existing long-term dollar-cost averaging strategy. Unlike a traditional personal loan, a margin loan offers more flexibility with principal repayment, allowing for better cash flow management while investing. My analysis indicates that for the first three years, the interest burden on a margin loan could be lower than that of a comparable personal loan. Although utilizing debt for investment carries inherent risks, my plan involves a systematic and gradual increase in investment amounts under disciplined risk management. My year-end target is to grow my total assets to over $60,000 USD.

Key Considerations for Leverage Investing

Leveraged investing, particularly through margin loans, carries significant risks. Market volatility can lead to unexpected losses, and rising interest rates can increase the cost of borrowing. Therefore, it's crucial to carefully assess your repayment capacity and your tolerance for potential losses before committing to leveraged strategies. A long-term perspective is essential; reacting emotionally to short-term market fluctuations can be detrimental. Currently, I am increasing my allocation to international equities as part of a diversified approach to potentially mitigate risks and capture global growth opportunities.

For more details, check the original source below.