Preparing for a property insurance exam? This guide breaks down the essential theories and exam strategies for the 'Overview of Property Insurance 2' section, crucial for your 2026 test success.

What are the core theories for 'Overview of Property Insurance 2' that frequently appear on exams?

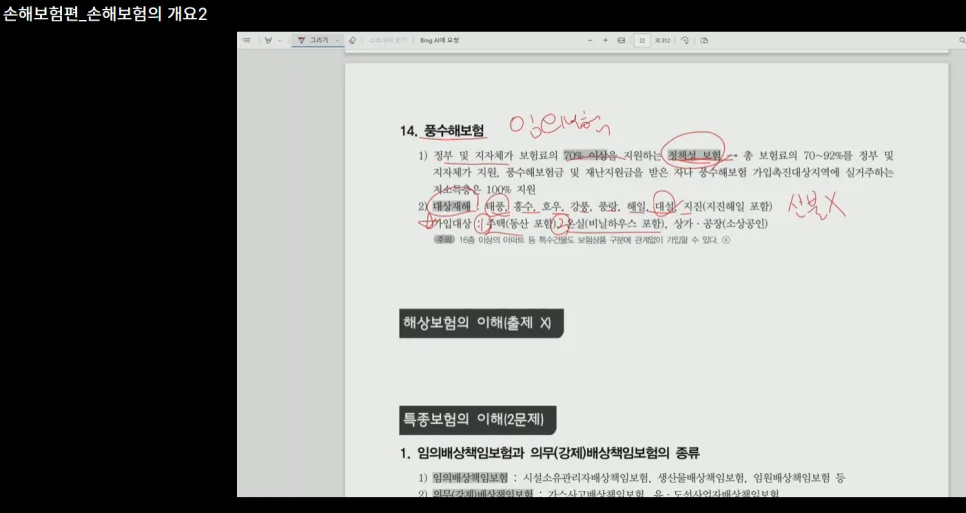

The 'Overview of Property Insurance 2' section often trips up test-takers. A key area is understanding catastrophe insurance, particularly for natural disasters. While government and local support often covers over 70% of policy costs for these government-backed policies, it's crucial to note that wildfire damage is *not* covered. Policies typically cover homes, greenhouses, commercial properties, and factories (for small businesses) against damage from typhoons, floods, heavy rain, strong winds, tidal waves, heavy snow, and earthquakes. When diving into specialty insurance, distinguishing between voluntary liability insurance (like facility owner's liability, product liability, and directors & officers liability) and mandatory liability insurance (for gas accidents, boat operators, sports facilities, and academies) is vital. A helpful mnemonic for remembering the types of mandatory liability insurance is '다학체가유' (Da-Hak-Che-Ga-Yu), which covers various mandatory insurance types in Korea. Other important policies include the Personal Information Protection Liability Insurance II, Elevator Accident Liability Insurance, and Fierce Dog Owner Liability Insurance.

What's the difference between loss occurrence basis and claims-made basis for liability insurance?

Related Articles

Liability insurance is broadly categorized into two main types: loss occurrence basis and claims-made basis. Loss occurrence basis policies cover claims that arise from incidents that occurred during the policy period, even if the claim is filed after the policy has expired. In contrast, claims-made basis policies cover claims that are filed during the policy period, regardless of when the incident occurred. This basis is primarily applied to Directors & Officers (D&O) liability insurance and professional liability insurance. Understanding this distinction is crucial for accurately answering exam questions. Professional liability insurance often covers professionals with '사' (sa) in their job title, such as doctors, lawyers, accountants, and architects.

What are the special policy types for commercial general liability insurance, and what is the coverage scope of theft insurance?

Commercial General Liability (CGL) insurance can be structured with various endorsements, including those for facility owners/managers, contractors, security services, parking lots, and auto repair shops. Theft insurance covers direct losses due to burglary or theft. However, it excludes losses resulting from intentional acts or gross negligence, theft from a vacant property left unattended for over 72 hours, or losses not discovered within 30 days. Additionally, theft losses occurring while property is stored outside its designated storage location are also not covered. It's essential to be aware of these exclusions to avoid surprises.

What are the main coverage details for leisure comprehensive insurance and travel insurance?

Leisure comprehensive insurance is divided into time-based and event-based policies. Time-based policies include golf insurance and hunting insurance, while event-based policies cover activities like fishing and skiing. Event-based policies often provide coverage from departure from your residence until arrival at your destination. However, coverage for loss of equipment related to specific activities (like fishing gear) is generally not included. Travel insurance typically includes a base policy covering accidental death and dismemberment with fixed payouts. Optional riders can provide coverage for accidental death due to illness, disability, medical expenses (up to $50,000 for overseas medical costs), liability claims, and personal belongings. For personal belongings, coverage is subject to per-item, per-set, or per-pair limits, and losses due to simple misplacement are not covered.

For more details, check the original source below.