The Special Mortgage (특례보금자리론) allows for early repayment with no fees, but it's crucial to consider factors like interest rates, debt-to-income ratios (DSR), and tax benefits before paying it off. Making an informed decision can save you significant money over the life of your loan.

What is the Special Mortgage and why are early repayment fees waived?

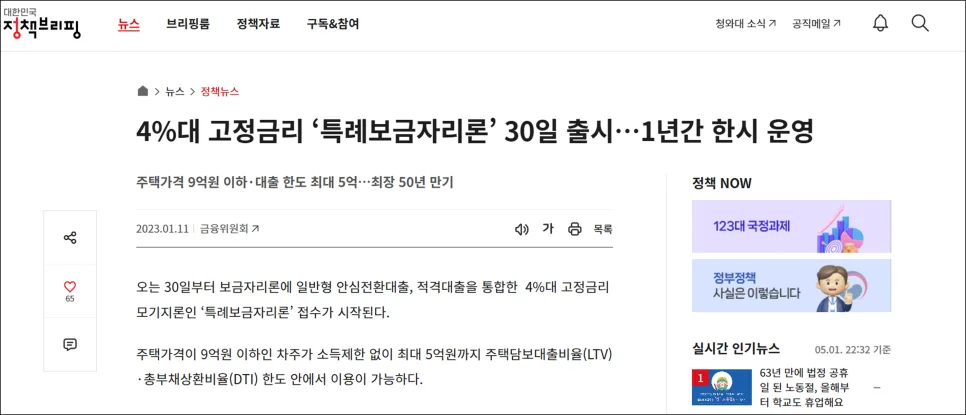

The Special Mortgage was a limited-time government-backed mortgage program launched in 2023 by the Korea Housing Finance Corporation (HF). Its primary goal was to stabilize household debt and support lower-income homeowners. A key feature was the complete waiver of early repayment fees, typically around 1.2% to 1.5% of the repaid principal, for loans repaid within three years. This applied both when switching from an existing mortgage to the Special Mortgage, and when refinancing or paying off the Special Mortgage itself. Lenders usually charge these fees to offset potential lost interest income when borrowers repay loans early. By eliminating this charge, the Special Mortgage significantly reduced the financial burden for borrowers, making it easier to manage their housing debt.

How much can you realistically save by repaying the Special Mortgage early?

For example, if you have a $300,000 Special Mortgage at a 4.5% interest rate and decide to repay $100,000 early, you could see substantial savings. This early repayment could reduce your monthly payments by approximately $510 (equivalent to ₩670,000) and save you around $126,000 (equivalent to ₩167 million) in total remaining interest over the loan's term. This translates to an annual improvement in your cash flow of over $6,000 (equivalent to ₩8 million), offering significant financial relief.

What is the standard procedure for early repayment?

To make an early repayment on your Special Mortgage, you can typically initiate the process through the Korea Housing Finance Corporation (HF) website or their mobile app. After submitting your repayment request, you will be provided with a virtual account number to deposit the repayment amount. Once the funds are received, the corporation will process the early repayment, reducing your outstanding loan balance and subsequent interest accrual. It's advisable to confirm the exact steps and required documentation with HF directly, as procedures can sometimes vary.

How does refinancing work with the Special Mortgage?

If you're looking to refinance your Special Mortgage with a new loan from a different bank, the process usually involves applying for the new mortgage first. Once your new loan is approved, the new lending institution will handle the repayment of your existing Special Mortgage on your behalf. This means you won't need to manage the transaction directly; the funds from your new mortgage will be used to clear the balance of the Special Mortgage. This streamlined process aims to make refinancing as convenient as possible for borrowers seeking better interest rates or loan terms.

What essential factors must you check before repaying the Special Mortgage early?

Before deciding to make an early repayment on your Special Mortgage, it's crucial to consider four key variables. First, compare current interest rates: if your Special Mortgage has a low fixed rate (e.g., around 4%), and new loan offers are only slightly lower or even higher (e.g., 4.5%), it might be more beneficial to stick with your current loan, especially if future rate hikes are anticipated. Second, check your Debt-to-Income ratio (DSR) regulations. While the Special Mortgage had lenient DSR rules, switching to a new bank loan will subject you to current DSR limits (often around 40%). If your income has decreased or you have other loans, your refinancing capacity might be less than expected. Third, consider the 'Year-End Tax Settlement' (연말정산) benefits. Interest paid on qualifying home loans can be tax-deductible in Korea. Paying down your principal early could reduce this tax benefit, so evaluate your tax bracket and potential savings. Finally, ensure you maintain sufficient liquidity. Using all your cash for early repayment can leave you vulnerable if unexpected expenses arise, potentially forcing you to take out new, costly loans. It's wise to keep an emergency fund. The best decision depends on your individual financial situation, and consulting a financial advisor is recommended.

For more details, check the original source below.