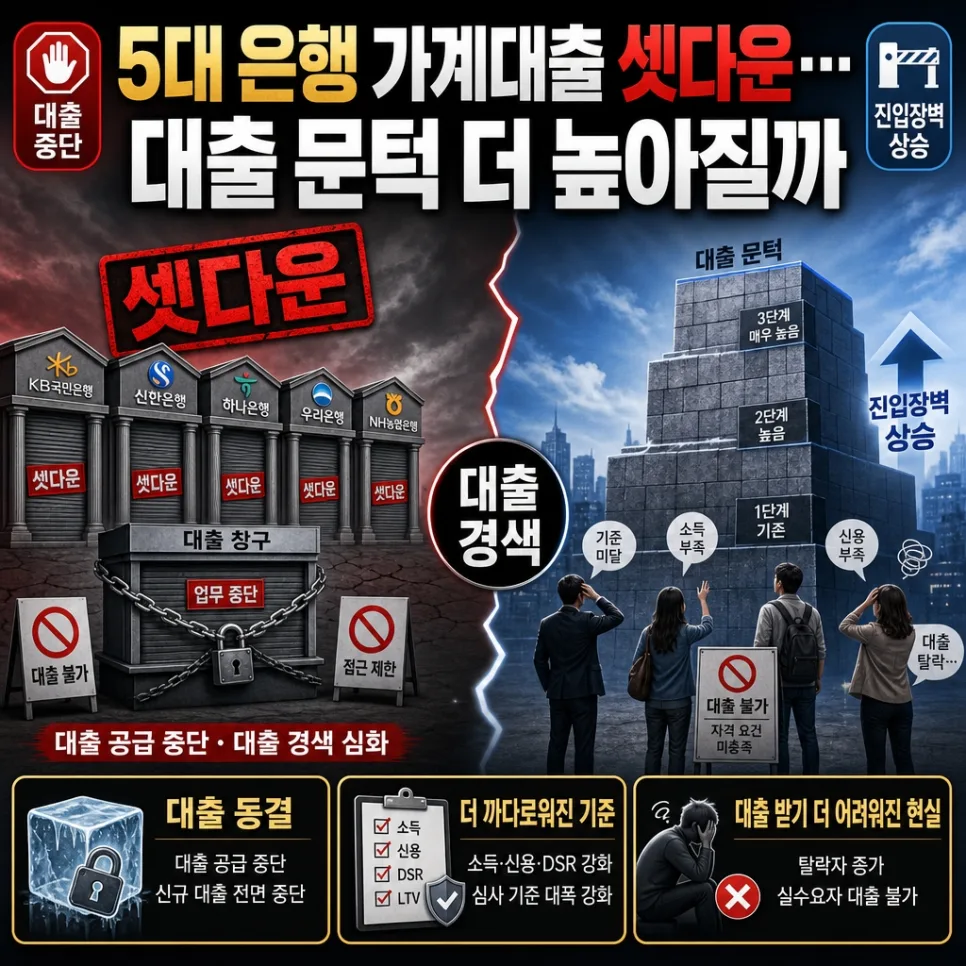

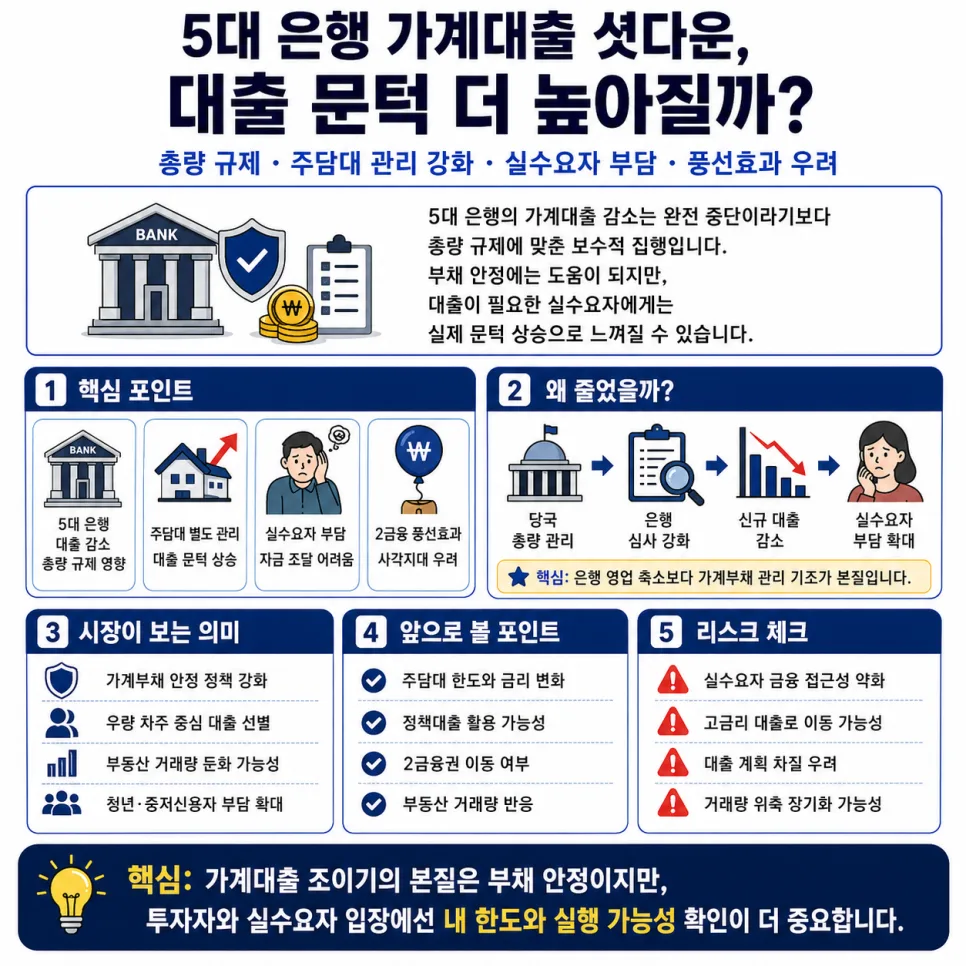

South Korea's top five banks saw a decrease in household loans in Q1 2026, not due to simple business changes, but a tightening of loan volume controls by financial authorities. With a lowered growth target for household loans and stricter management of mortgage lending in 2026, the borrowing threshold for genuine homebuyers may rise significantly.

Why Are Banks Moving Cautiously on Household Loan Limits?

While banks can increase interest income by expanding loans, exceeding the financial authorities' household debt management targets incurs regulatory penalties. For this reason, banks have been controlling new loan volumes since the beginning of the year. Mortgage loans, in particular, are subject to separate management, making them likely to be handled with even greater caution. In fact, the fact that the top five banks' household loans recorded a year-on-year decrease in Q1 indicates that the banking sector is already maintaining a significantly conservative stance. This goes beyond simply reducing loan amounts and could impact the overall funding environment in the financial market going forward.

Rising Loan Thresholds: What's the Impact on Homebuyers and Lower-Income Borrowers?

Managing household debt is crucial for stabilizing overall debt levels, but loan contraction can directly affect genuine borrowers who urgently need funds. Young adults, individuals with lower credit scores, and those relying on loans for essential living expenses may face stricter loan evaluations. If banks prioritize lending to prime borrowers, the financial accessibility for these groups could further diminish. This could lead not only to increased difficulty in obtaining loans but also to a rise in financial exclusion. Therefore, loan regulations require a careful approach that balances financial market stability with social equity.

What's the Effect on the Real Estate Market and Secondary Banks?

When bank loan thresholds rise, it can dampen home-buying sentiment, initially impacting real estate transaction volumes. Genuine buyers who rely heavily on loans may postpone their purchase plans or need to re-evaluate their financial strategies. Conversely, this environment could become relatively more favorable for buyers with substantial cash reserves. Additionally, some demand might shift to secondary financial institutions (like credit unions or savings banks) as bank loans become restricted, a phenomenon known as the 'balloon effect.' However, secondary institutions are also strengthening their household debt management, so the impact might be limited. The concern is that borrowers in genuine need could be pushed towards high-interest loans or less conventional financial channels, increasing risks for the overall financial system.

Household Loan Freeze: What Scenarios Can We Expect Moving Forward?

In the short term, expect continued tightening of loan evaluations and reduced limits from banks. In the medium term, genuine borrowers, particularly for mortgages and 'jeonse' (lump-sum deposit) loans, may experience increasing inconvenience. In the long term, while these measures may contribute to household debt stability, they could burden consumption and real estate transactions. Therefore, if you are planning to take out a loan, it's crucial to meticulously check loan limits, interest rates, and execution timelines in advance, and establish conservative financial plans. Since loan eligibility and terms can vary based on individual circumstances, consulting with a financial expert for accurate information is recommended.

For more details, check the original source below.