Understanding the Newborn Special Loan limits for 2026, including LTV and DTI requirements, can help you calculate your maximum loan amount, potentially up to $300,000 for home purchases. This guide breaks down the key figures for both purchase and rental funds, offering a clear path for new parents navigating the Korean housing market.

Newborn Special Loan Purchase Fund Limits: What Are the 'Didimdol Loan' Standards?

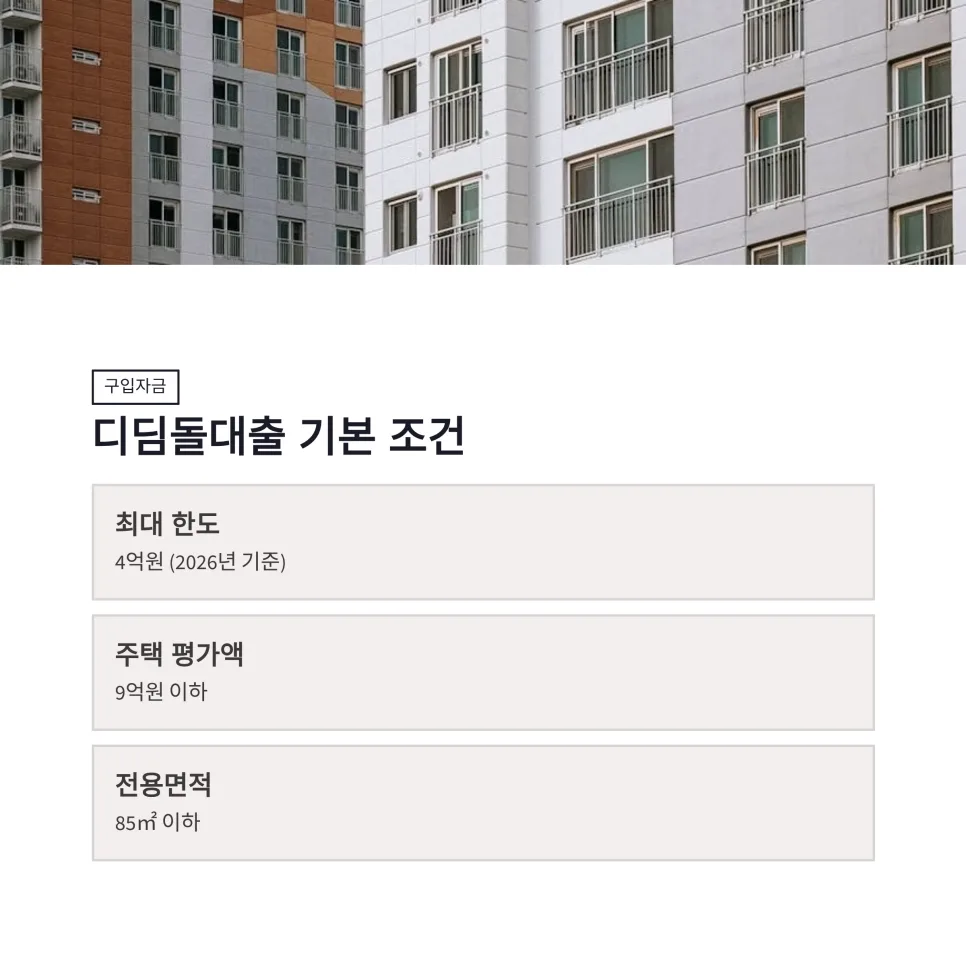

When calculating the purchase fund limit for the Newborn Special Loan, the first crucial step is to understand the 'Newborn Special Didimdol Loan' criteria. For 2026, the maximum loan amount is set at 400 million KRW (approximately $300,000 USD), applicable to homes valued at 900 million KRW (approx. $675,000 USD) or less, with a floor area under 85 square meters. However, it's vital to note that the '$300,000 USD' figure isn't guaranteed. Your actual loanable amount will be the lower of either 70% of the home's appraised value (LTV) or the 400 million KRW (approx. $300,000 USD) product limit. While first-time homebuyers might qualify for an 80% LTV, this can be reduced to 70% in regulated areas or specific regions. Failing to grasp these nuances before signing a contract can lead to a significant shortfall compared to your expected loan amount.

How Are LTV and DTI Applied in Newborn Special Loan Limit Calculations?

Related Articles

- Seoul Sillim-dong Multi-Family Home Auction: Analyzing the 2026 Lowest Price Investment Opportunity

- Real Estate Tax Bomb After June Election? Comprehensive Tax, Long-Term Discount, Acquisition Tax Changes 2026

- 500M-700M KRW ($375K-$525K USD) Capital Area Apartment Entry Strategy 2026: Owner-Occupier vs. Investor Guide

When calculating your Newborn Special Loan limit, it's common for DTI (Debt-to-Income ratio) to reduce your borrowing capacity more than the LTV (Loan-to-Value ratio). While LTV dictates the maximum loan amount relative to your home's value, DTI measures the proportion of your annual income that goes towards repaying all your debts annually. For the Newborn Special Didimdol Loan, the DTI is capped at 60%. For instance, on a 600 million KRW (approx. $450,000 USD) home, a 70% LTV would suggest a maximum loan of 420 million KRW (approx. $315,000 USD). However, the 400 million KRW (approx. $300,000 USD) product limit is the first constraint. Furthermore, your existing debts—including credit card debt, car loans, and any outstanding balances on lines of credit—are factored into the annual principal and interest payments. This means your actual loanable amount could be significantly less than the initial calculation suggests. I've seen firsthand how complex these calculations can be, far beyond simple multiplication.

Newborn Special Loan Rental Fund Limits: How Do They Differ from 'Bumtteok Loans'?

When calculating rental fund limits for the Newborn Special Loan, different criteria apply compared to purchase funds. The Newborn Special Bumtteok Loan, as of 2026, can go up to 240 million KRW (approx. $180,000 USD), determined by 80% of your rental deposit. There are also regional caps: 500 million KRW (approx. $375,000 USD) for deposits in the Seoul metropolitan area and 400 million KRW (approx. $300,000 USD) outside of it. For example, if your rental deposit is 300 million KRW (approx. $225,000 USD), 80% is 240 million KRW (approx. $180,000 USD), matching the maximum limit. If your deposit is 400 million KRW (approx. $300,000 USD), 80% would be 320 million KRW (approx. $240,000 USD), but your loan will be capped at the 240 million KRW (approx. $180,000 USD) maximum. While rental fund calculations are generally more straightforward than purchase loans, remember that the actual loan amount can vary based on the guarantor's assessment and the specifics of the lease agreement.

What Are the Common Mistakes When Calculating Newborn Special Loan Limits?

The most frequent error when calculating Newborn Special Loan limits is confusing the criteria for purchase funds versus rental funds. Purchase loans are capped at 400 million KRW (approx. $300,000 USD) based on LTV of 70% and DTI of 60%. Rental loans, under the Bumtteok program, have a maximum of 240 million KRW (approx. $180,000 USD), typically covering 80% of the rental deposit, with regional caps. Understanding which loan type you're applying for and its specific requirements is the first step to accurate calculation. Additionally, underestimating the impact of existing debts on your DTI can lead to a lower-than-expected loan amount. Always verify your eligibility and the precise calculation method with the lending institution before making any financial commitments. This is not financial advice. Consult a licensed financial advisor.