Achieve over $1,500 in profit with Nasdaq 100 ETF investments while leveraging tax savings through retirement accounts. Discover smart strategies for year-end tax deductions and the power of compounding for long-term wealth growth.

Why Invest in Nasdaq 100 ETFs Through Retirement Accounts?

Investing in ETFs that track the Nasdaq 100 index via retirement accounts like a Traditional IRA or 401(k) offers a compelling dual benefit: maximizing long-term compounding growth and securing valuable tax deductions during tax season. I've personally experienced how the power of time, combined with these accounts, can significantly boost returns. Recently, Nasdaq 100 ETFs held within these retirement vehicles have outperformed other safer asset allocations. Historically, investments in IRAs and 401(k)s have proven advantageous for long-term wealth accumulation. While leveraged ETFs can offer substantial gains, a long-term perspective is crucial due to their inherent volatility. Traditional IRAs allow for annual contributions up to $6,500 (for those under 50 in 2023, subject to change), with potential tax deductions of up to 16.5% for those earning under $120,000 annually, translating to a significant tax credit. This additional benefit effectively increases your real return on investment. Therefore, for those planning to invest long-term in high-growth assets like the Nasdaq 100, utilizing a Traditional IRA or similar retirement account is a wise financial move.

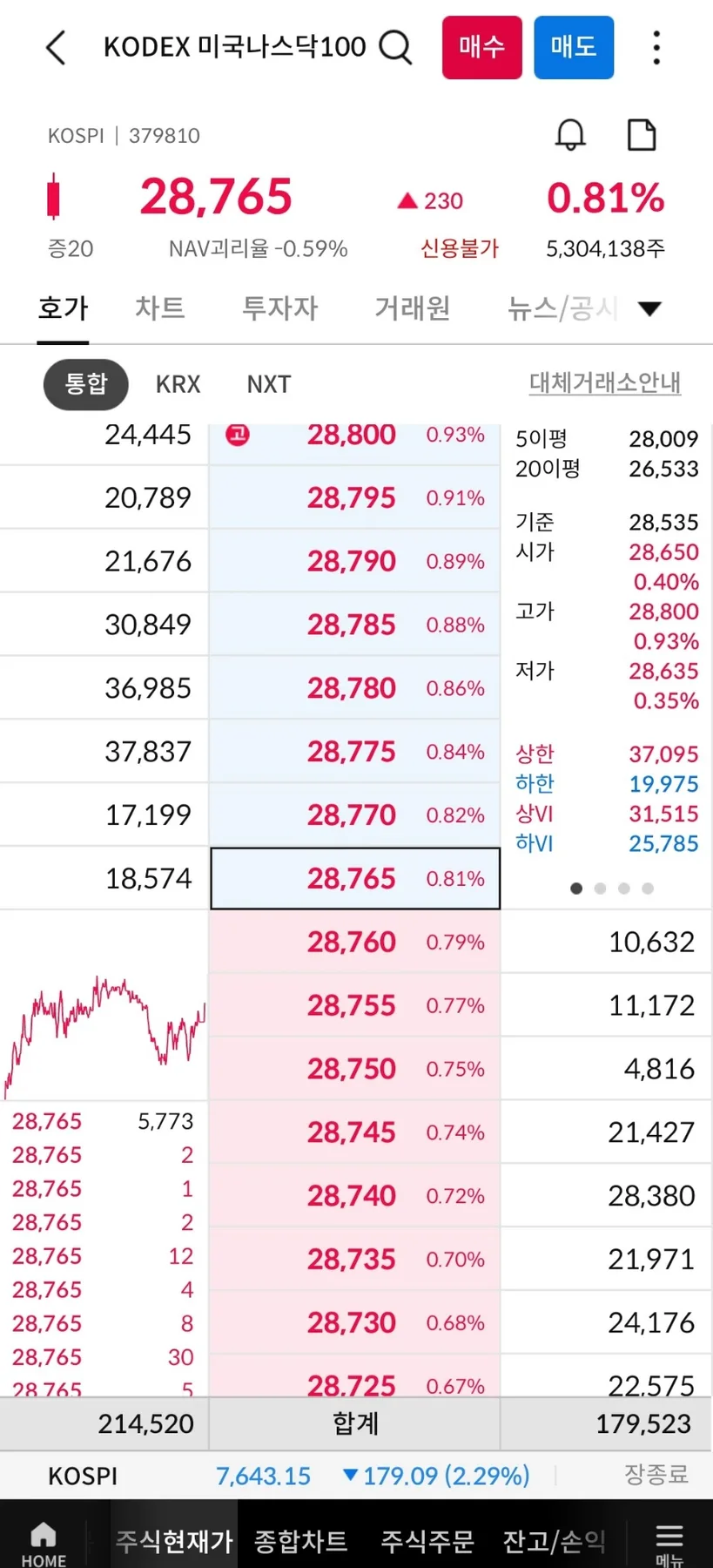

Choosing the Right Nasdaq 100 ETF for Your Portfolio

Related Articles

Once you've decided to invest in Nasdaq 100 ETFs, selecting the right product is key. Popular options include QQQ (Invesco QQQ Trust) and its variations. When choosing, carefully review the ETF's expense ratio, tracking error relative to its index, and distribution frequency. Leveraged ETFs, such as TQQQ (ProShares UltraPro QQQ) or SOXL (Direxion Daily Semiconductor Bull 3X Shares), aim to deliver 2x or 3x the daily returns of the Nasdaq 100, offering the potential for higher profits but also carrying significantly greater risk and volatility. For beginner investors, starting with a standard Nasdaq 100 ETF like QQQ is advisable to understand market dynamics before considering more complex leveraged products. It's also important to understand the differences between lump-sum investing and dollar-cost averaging. Dollar-cost averaging, by consistently investing a fixed amount over time, can mitigate the risk of timing the market and potentially lower your average cost per share. Lump-sum investing, conversely, can yield greater returns during bull markets but exposes you to higher risk during downturns.

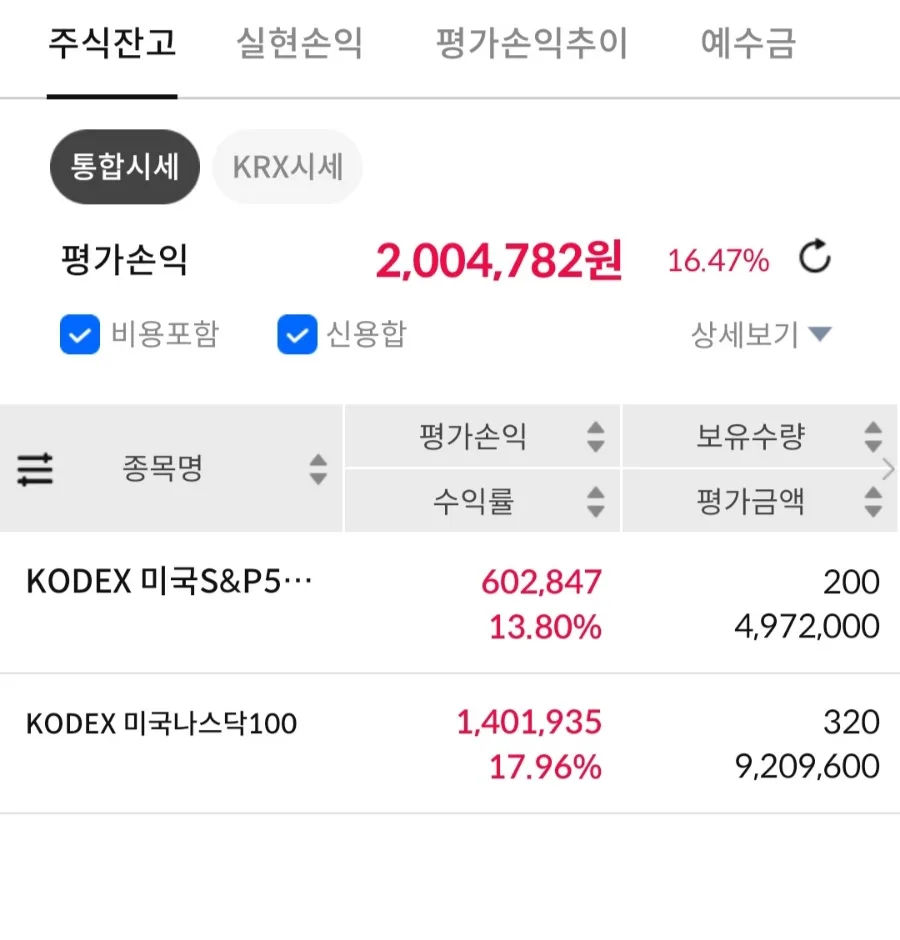

Real Returns and Tax Benefits of Nasdaq 100 ETF Investment

My Nasdaq 100 ETF investments have yielded approximately $1,500 in profit, excluding the tax benefits from my retirement account. The annual contribution limit for a Traditional IRA is $6,500 (for individuals under 50 in 2023, adjusted annually), with a potential tax deduction of up to 16.5% for those with a modified adjusted gross income under $120,000. This could result in a tax refund of up to $990 annually, effectively boosting your overall investment gains. It's crucial to determine your optimal contribution amount based on your income and tax situation. Furthermore, the investment gains within a Traditional IRA are tax-deferred, meaning you won't pay taxes on them until you withdraw the funds in retirement. This tax deferral significantly enhances the power of compounding over the long term. However, be aware that early withdrawal penalties and taxes may apply if you withdraw funds before retirement age, so careful planning is essential.

Key Considerations for Nasdaq 100 ETF Investors

Investing in Nasdaq 100 ETFs, especially leveraged ones, requires careful consideration. Firstly, the high volatility is a significant factor. The Nasdaq 100, being tech-heavy, can experience rapid price swings based on market news and economic conditions. Leveraged ETFs amplify these movements, increasing both potential gains and losses. Secondly, the compounding effect in leveraged ETFs can be a double-edged sword. Because returns are calculated daily, long-term holding of leveraged ETFs can lead to underperformance compared to the underlying index, even if the index rises over time. For long-term investors, a standard Nasdaq 100 ETF might be more suitable, or leveraged ETFs should be approached with strict risk management. Thirdly, tax implications differ significantly. Investing in a Nasdaq 100 ETF through a standard brokerage account incurs capital gains tax (typically 15% or 20% depending on your income bracket) on profits. However, using a Traditional IRA allows for tax deferral, and withdrawals in retirement are taxed at your then-current income tax rate, which may be lower. Therefore, for tax efficiency, retirement accounts are generally preferred. Your individual investment goals and risk tolerance will ultimately dictate the best strategy, and consulting a financial advisor is recommended.

Discover more investment experiences and tax-saving tips in the original article.