The 2026 Military Savings Plan (Jangbyeong Naeil Junbi Jeokgeum) is a powerful financial tool allowing service members to save over $14,000 USD by their discharge, thanks to a doubled principal match from the government and tax-free interest. This guide breaks down how to maximize these benefits for US-based service members.

What's New with the 2026 Military Savings Plan?

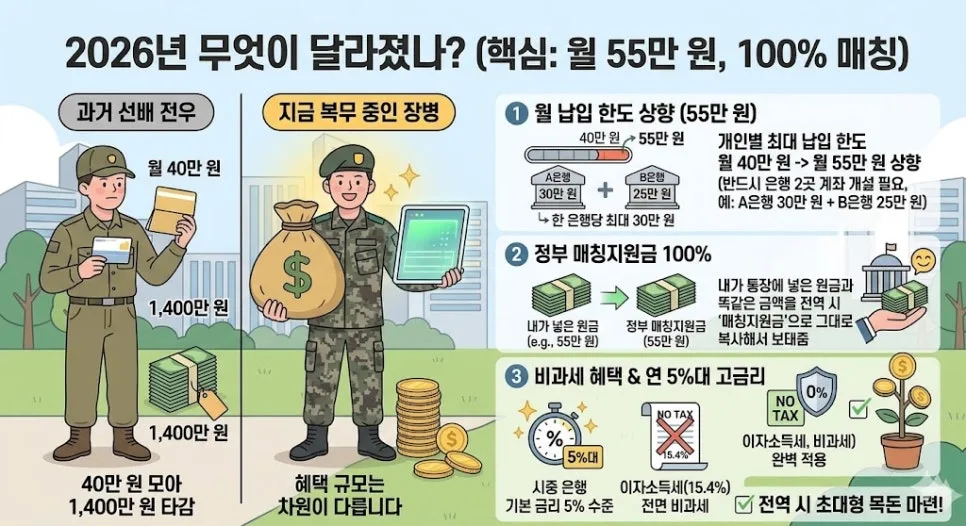

Starting in 2025, the monthly contribution limit for the Military Savings Plan has significantly increased from $300 to $400 USD. However, to maximize this, service members must open accounts at more than one bank, as each bank has a maximum monthly deposit limit of $220 USD. For example, you could deposit $220 USD in Bank A and $180 USD in Bank B. The government matches 100% of your principal contributions, effectively doubling your savings. Additionally, these savings earn a competitive interest rate of around 5% annually, with all interest being tax-free. These enhanced benefits make it easier than ever for service members to build substantial savings.

What Can You Expect to Receive After 18 Months of Service?

If you serve 18 months and consistently contribute the maximum monthly amount of $400 USD, you can expect to receive approximately $14,000 USD upon discharge. This total includes your principal contributions of $7,200 USD, the government's matching contribution of $7,200 USD, and roughly $270 USD in interest (based on a 5% annual rate, tax-free). This represents a guaranteed return that significantly exceeds your initial investment, making it a highly secure way to build wealth during your service. This is a fixed return that is difficult to achieve even with high-risk investments like stocks or cryptocurrency.

Who is Eligible for the Military Savings Plan and What Are the Requirements?

Eligibility extends to all active-duty service members, including active reservists, social service workers (equivalent to US civil service), and alternative service personnel. A key requirement is having at least one month of remaining service time. The most common way to enroll is through bank representatives who visit training centers. For those already assigned to their duty stations, you can obtain a 'Qualification Certificate' from the 'Nara Sa-rang Portal' (a government-backed online service) and then visit a commercial bank during leave to open an account. Regular automatic deductions from your salary ensure consistent contributions.

What Are the Consequences of Early Withdrawal from the Military Savings Plan?

The most critical warning is to avoid early withdrawal at all costs. If you terminate the plan before its maturity date, you will forfeit the entire 100% government matching contribution, rendering your 18 months of dedicated saving potentially worthless. Therefore, unless there are extraordinary circumstances, maintaining the plan until its full term is strongly advised. The estimated payout figures are based on standard interest rates and tax-free benefits; actual amounts may vary based on individual preferential interest rates or the exact deposit dates. It's best to confirm the precise final amount with your specific bank.

For more details, check the original source below.