Many young Koreans worry about extending their housing loans when their security deposit exceeds the 300 million KRW (approx. $225,000 USD) threshold. However, it's crucial to understand that loan extension policies differ from new application rules. In the Seoul metropolitan area, you can often extend your loan even if your deposit surpasses 300 million KRW, potentially up to 500 million KRW (approx. $375,000 USD).

Korean Youth Housing Loan Extension: What's the Deposit Limit Past 300 Million KRW?

I remember the stress of renewing my lease two years ago after taking out the Youth栋梁 (Dongnyang) housing loan for a deposit under 300 million KRW (approx. $225,000 USD). When my rent increased by 5% and pushed my deposit over the 300 million KRW mark, I spent sleepless nights worrying if my loan extension would be denied. Fortunately, I confirmed that for the Seoul metropolitan area, the Youth Dongnyang loan can be extended for deposits up to 500 million KRW (approx. $375,000 USD). This is a critical distinction from the 300 million KRW limit for new loan applications, a detail many overlook, causing unnecessary anxiety. My experience taught me the vital importance of understanding these specific extension criteria well in advance, rather than waiting anxiously for the bank's notification a month or two before the loan matures.

What's the Extension Process for Korean Youth Housing Loans Over 300 Million KRW?

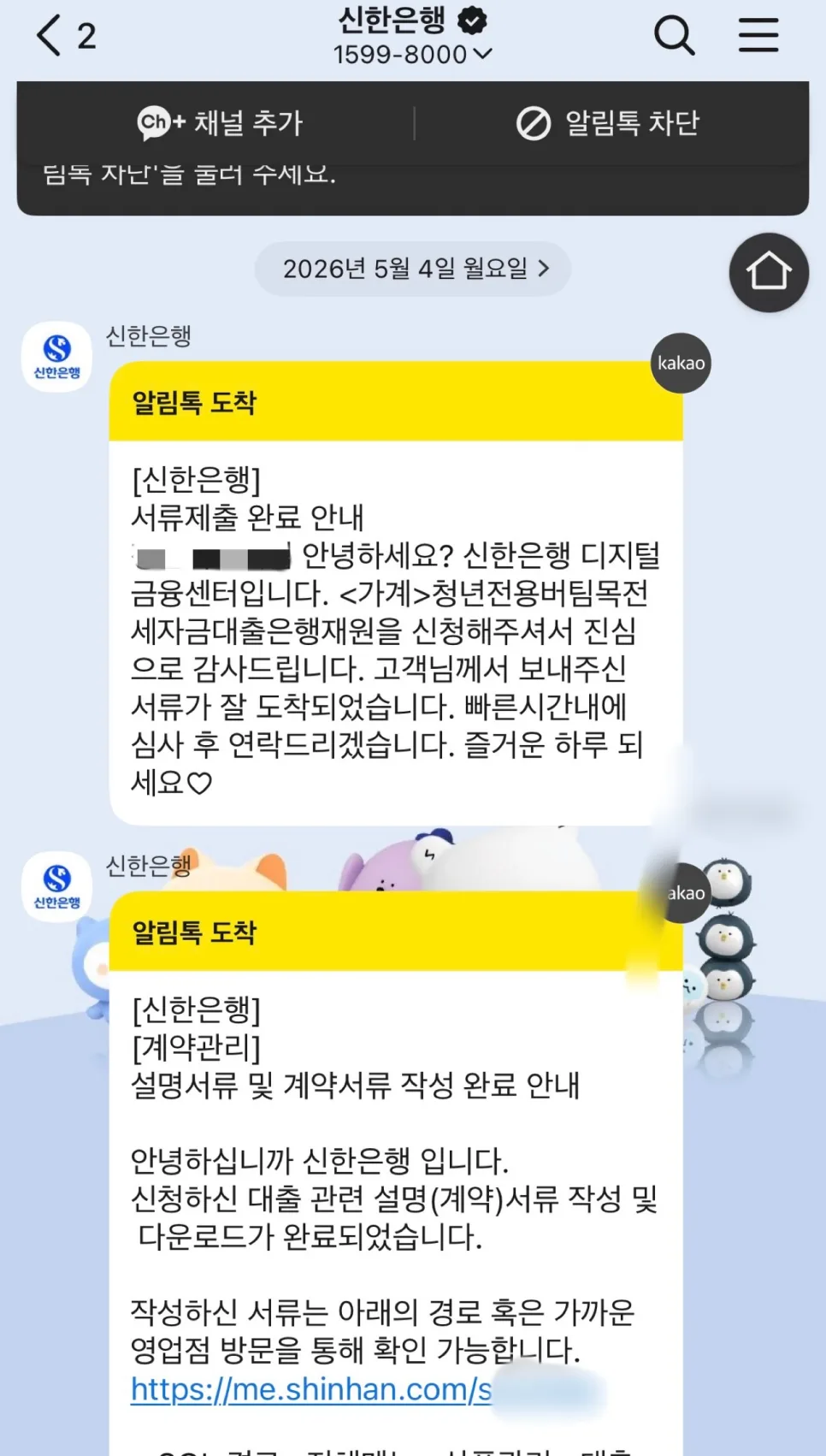

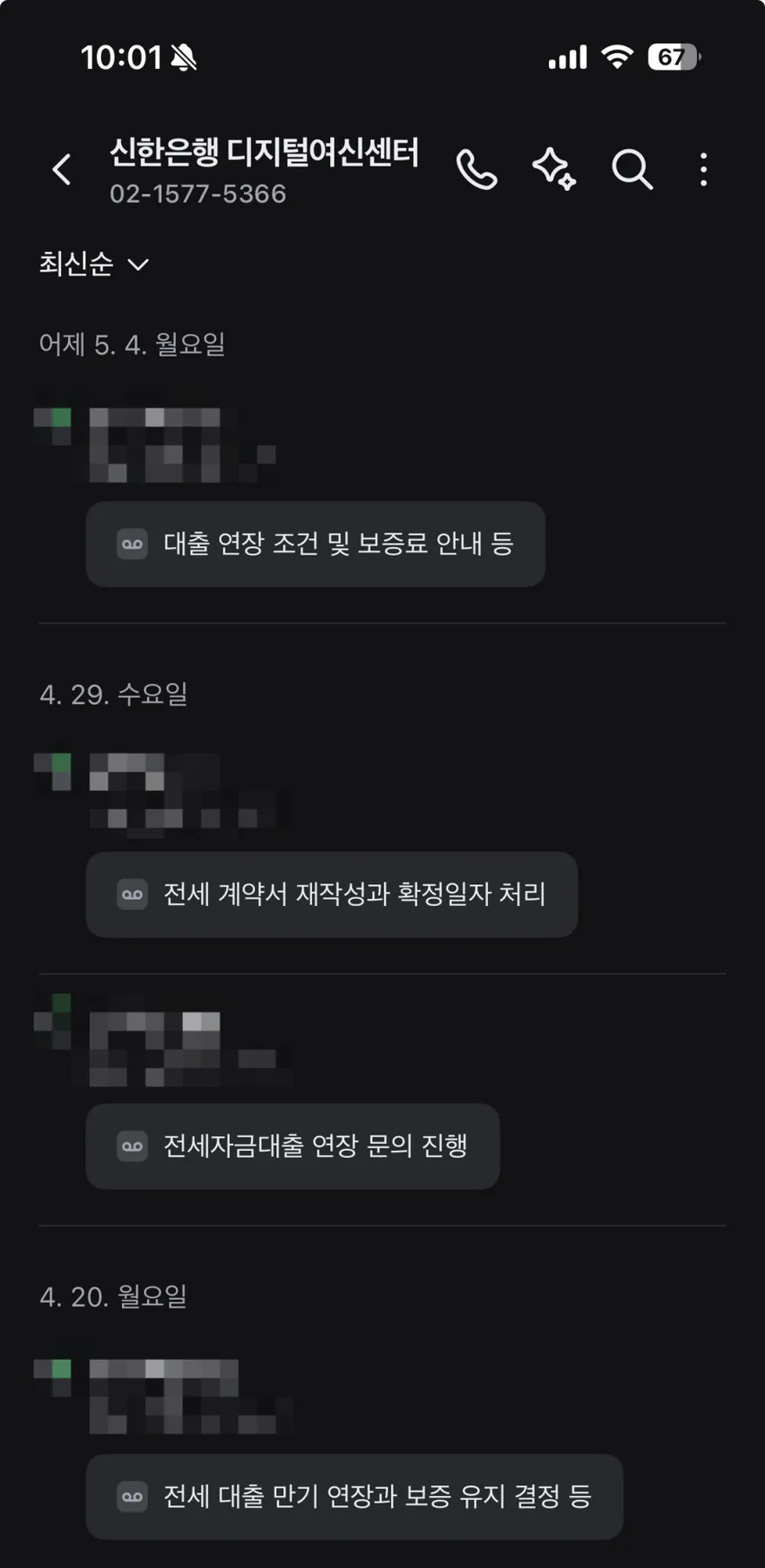

Despite my concerns about the increased deposit, my bank, Shinhan Bank, contacted me about a month before my loan's maturity date regarding the extension. The process was surprisingly smooth; I received a link to upload my renewed lease agreement and the stamped copy of the lease from the online portal. This digital approach eliminated the need for in-person branch visits or gathering extensive paperwork, making it incredibly convenient. Obtaining the official stamp (확정일자, hwakjeong-ilja) from the internet registry took about two hours, though visiting a local community center (동사무소, dongsamuso) is also an option for faster processing. Utilizing these online systems significantly saves both time and effort in managing your housing loan.

Korean Youth Housing Loan Extension: Guarantee Insurance and Interest Rate Options

With the increase in my security deposit, I had to decide whether to increase my coverage with the Housing & Urban Guarantee Corporation (HUG) insurance or maintain the existing amount. Increasing the insurance coverage would incur additional guarantee fees. For the interest rate, I was presented with two options: a 0.1%p increase on my existing rate or repaying 10% of the loan principal. Considering the burden of a large lump-sum repayment, I opted for the 0.1%p interest rate hike, bringing my rate from 2.5% to 2.6%. If I were renewing after April 26, 2024, and qualified as a young person employed in a small or medium-sized enterprise (SME), I could have benefited from a 0.3%p rate reduction and waived extension interest. This makes me look forward to my next renewal, as I plan to focus on saving for a down payment on my own home by then.

Key Considerations for Extending Your Korean Youth Housing Loan

The most critical aspect when extending your Youth Dongnyang housing loan is clearly understanding the difference between the new application criteria and the extension criteria. While new applicants must have a security deposit of 300 million KRW (approx. $225,000 USD) or less, extensions in the Seoul metropolitan area can accommodate deposits up to 500 million KRW (approx. $375,000 USD). Failing to grasp this distinction can lead to unnecessary worry about loan ineligibility due to a rising deposit. Additionally, if you're extending during a period of rising interest rates, carefully weigh the options of a marginal rate increase versus a partial principal repayment based on your financial capacity and future plans. It's always wise to consult with a financial professional to make the best decision considering your personal financial situation and the dynamic housing market.

For detailed extension procedures and conditions, check the original source below.