Korean ISA (Individual Savings Account) principal can be withdrawn anytime without affecting tax benefits, regardless of the 3-year mandatory holding period. With the expanded tax-free limits and the income-offsetting feature under the 2026 reforms, you can maximize your tax savings. This guide breaks down the types of ISAs, their benefits, and strategies for US investors.

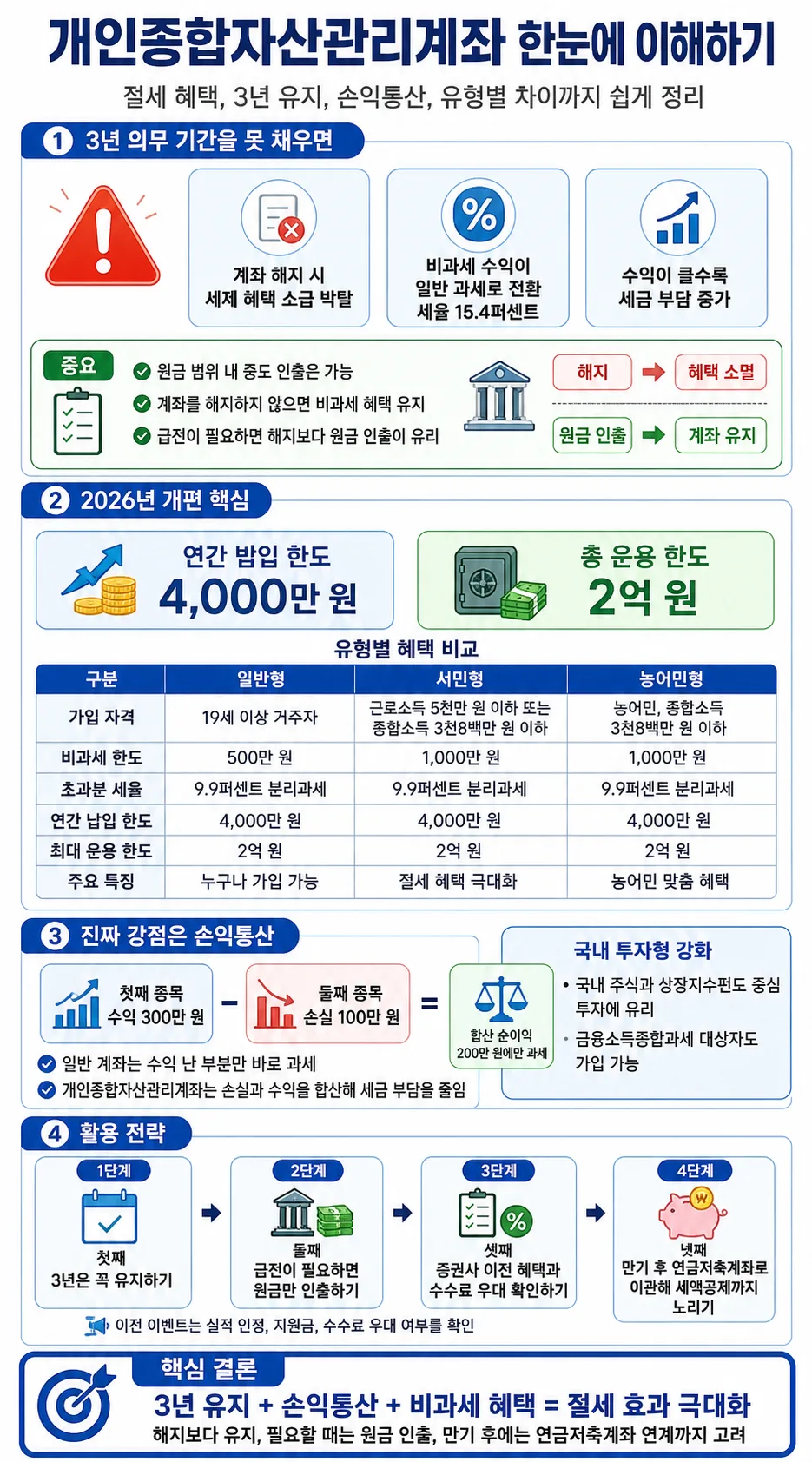

What Happens If You Don't Meet the ISA's Mandatory Holding Period?

The primary appeal of an ISA account lies in its tax-exempt and low-tax benefits. However, these advantages are contingent upon fulfilling a mandatory 3-year holding period. If you withdraw funds before this period ends, all previously enjoyed tax benefits will be retroactively revoked. Specifically, any profits that were tax-exempt will be subject to the standard 15.4% income tax rate. For investors with significant gains, this can result in a substantial and unexpected tax burden. Many investors overlook this crucial detail, leading to a 'tax bomb.' Fortunately, ISAs allow for the withdrawal of principal funds at any time without impacting the account's tax-exempt status. Therefore, if you face an urgent need for cash, it's wiser to withdraw only the principal and keep the account open to preserve its tax benefits. This strategy allows you to access liquidity while maintaining your tax advantages, making it a practical approach to tax-efficient saving.

Korean ISA Account Types and Benefits Under 2026 Reforms

Related Articles

As of May 2026, the contribution limits and tax-exempt scopes for ISA accounts have been significantly expanded. The annual contribution limit is now set at 40 million KRW (approximately $30,000 USD), with a total investment ceiling of 200 million KRW (approximately $150,000 USD). This offers greater opportunities for tax savings for affluent individuals and a solid foundation for young professionals to build wealth. Notably, for individuals qualifying for the 'Commoner Type' ISA (typically those with lower income levels), the tax-exempt limit doubles to 10 million KRW (approximately $7,500 USD). Choosing the right ISA type based on your income and investment goals is crucial. For instance, if your annual income is below 50 million KRW (approx. $37,500 USD) or total income below 38 million KRW (approx. $28,500 USD), you may qualify for the Commoner Type ISA, enjoying a higher tax-exempt threshold. Carefully compare the eligibility criteria and tax-exempt limits for each type to select the most suitable ISA account for your financial situation.

The Magic of Income Offsetting in ISAs and the Rise of Domestic Investment ISAs

The true value of an ISA extends beyond its tax-exempt limits due to its powerful 'income offsetting' (sonik tongsan) feature. In a standard brokerage account, if you profit from Stock A but lose money on Stock B, you'll still pay taxes on Stock A's gains. However, within an ISA, your gains and losses across all investments are netted out, and taxes are only applied to the final net profit. Furthermore, a significant portion of this net profit is tax-exempt, and any remaining taxable amount is subject to a low, separate tax rate of 9.9%. The newly enhanced 'Domestic Investment ISA' introduced in 2026 also allows individuals subject to comprehensive financial income tax to open an account. This type is designed to encourage domestic stock and ETF investments, fostering capital circulation within Korea. It presents an attractive option for investors focusing on dividend-paying stocks. These features collectively enable investors to substantially reduce their actual tax burden while potentially increasing their investment returns.

Related Articles

Strategies for Transferring ISA Accounts Between Brokerages and Leveraging Promotions

Major brokerages, including Korea Investment & Securities' 'Bankis' platform, are actively marketing to attract customers holding ISA accounts at other institutions. Promotions running until May 31, 2026, offer incentives such as doubling the value of transferred assets or conducting lotteries for high-value investment bonuses. These events are excellent opportunities not only to receive gifts but also to renegotiate fee structures. Operating an ISA account with preferential online trading fees as low as 0.003% can lead to significant differences in returns, potentially tens of millions of KRW (tens of thousands of USD), over the long term. The intermediary-type ISA is a legally sanctioned tax-saving vehicle. With just a 3-year commitment, you can enjoy the dual benefits of compound growth and tax savings. After maturity, you can even transfer the funds to a retirement pension account to pursue additional tax credits, a strategy known as 'windshield wiper' investing. The optimal strategy varies depending on individual circumstances, so consulting with a financial advisor is recommended to find the best approach for you.

For more details, check the original source below.