Worried about the downsides of an ISA account or facing early withdrawal dilemmas? This guide clarifies the latest 2026 information, drawing on real-world experiences. While an ISA (Individual Savings Account) allows you to manage various financial products in one place and offers tax benefits, it comes with significant drawbacks and common misconceptions that US investors should understand.

What Are the Main Downsides of an ISA Account?

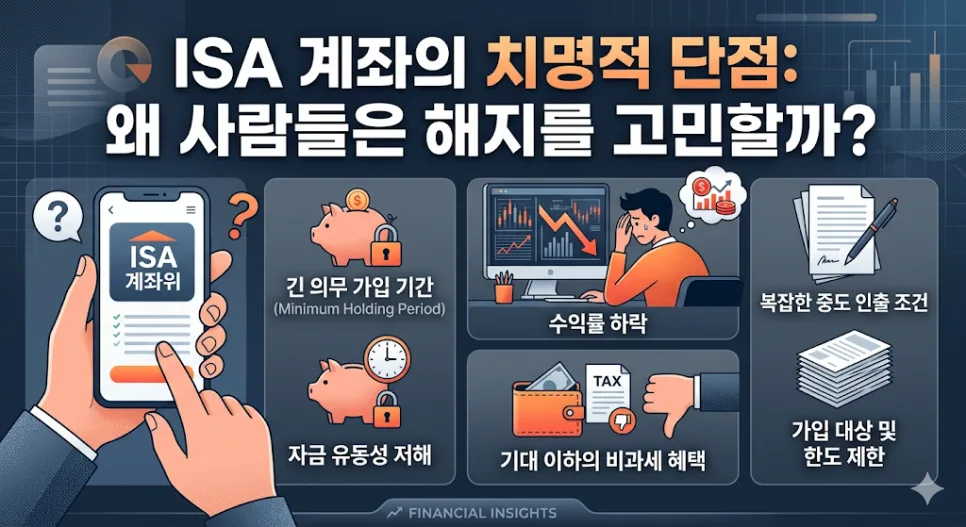

Often touted as a 'universal bank account,' ISA accounts have several easily overlooked disadvantages. The most significant are the mandatory holding period and the penalties for early withdrawal. Most ISA accounts in Korea have a mandatory 3-year holding period. If you withdraw funds before this period ends, you forfeit all previously received tax benefits, and a 16.5% income tax may be imposed. This penalty can be a substantial burden, especially if you need access to your funds unexpectedly. Furthermore, ISA accounts have a cap on tax-exempt earnings. If your investment returns exceed this limit, the excess amount will be taxed. For high-net-worth individuals or those expecting rapid, high returns, the tax-saving benefits of an ISA might be limited.

What Are Common Misconceptions About ISA Accounts?

One of the most prevalent myths about ISA accounts is that all investment profits are tax-free. In reality, the tax-exemption limit varies by ISA type. For instance, a 'regular' ISA account offers tax exemption up to ₩2 million (approximately $1,500 USD) for general investors, while a 'low-income' ISA offers up to ₩4 million (approximately $3,000 USD). Profits exceeding these limits are taxed at a 9.9% rate. Another misconception is that early withdrawals are flexible. While some early withdrawal options exist, they differ from a full account termination and may impact tax benefits. Early withdrawals involve taking out a portion of your principal and profits, which can reduce your tax-exempt allowance or, under certain conditions, diminish your tax benefits. Therefore, careful consideration is necessary even when making partial withdrawals.

How Can You Maximize Tax Savings with an ISA Account?

To maximize the tax benefits of an ISA account, a strategic approach is essential. Firstly, plan for the long term and aim to fulfill the mandatory holding period. Holding the account for over three years allows you to benefit from tax-free income within the exemption limits or enjoy lower tax rates on excess earnings, making long-term investment crucial. Secondly, select the ISA account type that aligns with your investment profile and goals. General investors might opt for a regular ISA, while those with lower incomes could benefit from a 'low-income' ISA for a higher tax-exempt threshold. Thirdly, diversify your investments within the ISA account by including a balanced mix of financial products. Combining savings accounts, funds, ETFs, and stocks can help mitigate risk and achieve stable returns, aligning with the original purpose of an ISA. If you need funds before the mandatory period, consider using the early withdrawal facility cautiously and adjust your future deposit plans accordingly.

What Should You Watch Out For When Canceling an ISA Account Early?

If you find yourself needing to cancel an ISA account before the mandatory period ends, there are critical points to keep in mind. The most significant consequence is the forfeiture of tax benefits. Upon early cancellation, all investment profits generated within the ISA account are subject to a 16.5% income tax. This rate is higher than the standard interest income tax of 15.4% for typical financial products, potentially leading to substantial financial losses. Therefore, it's advisable to fulfill the mandatory holding period unless absolutely necessary. If early termination is unavoidable, it's crucial to accurately assess your profits and principal and calculate the estimated tax burden beforehand. Additionally, ISA accounts have annual deposit limits, which you must consider if you plan to re-enroll after cancellation. The optimal strategy for using an ISA account can vary based on individual financial circumstances and investment objectives, so consulting with a financial advisor is recommended for informed decisions.

English crawl path

Next English reads from this pilot cluster

Continue through the category hub, latest English stories, and related posts so this translated article is not an isolated URL.

Tags

💬Frequently Asked Questions

What should I check first in ISA Account Downsides & Myths 2026: Solving Early Withdrawal Worries?

Does this Finance article link back to the Korean source?

Where can I find similar English stories?

English discovery path

Explore more English K-culture stories

Keep browsing the indexed English pilot cluster so Google and readers can move between this story, the category hub, and fresh discovery pages.

Original Source

Read the Korean original