Navigating Korean income tax filing can be confusing, especially understanding which method to use (bookkeeping vs. estimated) and how previous year's sales determine your tax obligations for 2026. It's crucial to clarify the reference year for your previous year's sales to ensure accurate filing.

2026 Korean Income Tax Filing: What's the Previous Year Reference?

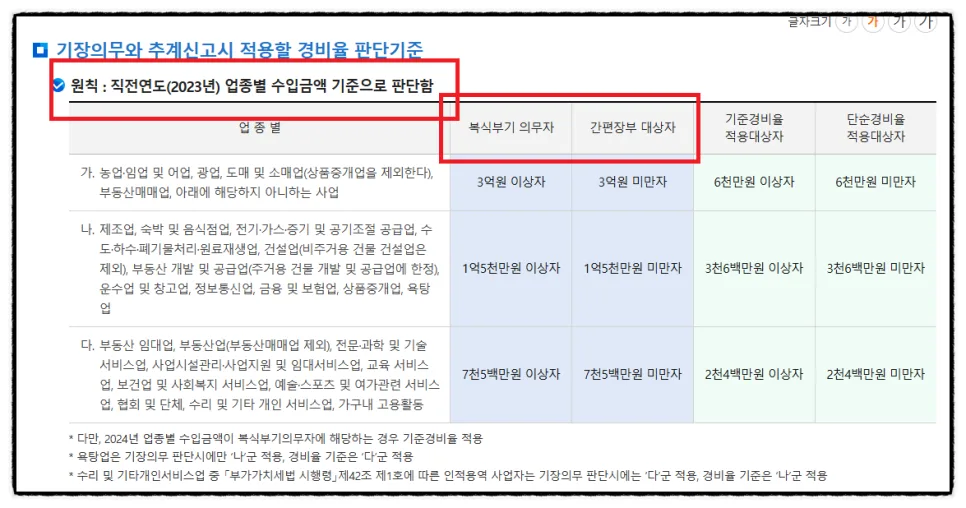

Many taxpayers are unsure about the 'previous year' when filing their 2026 Korean income tax. Simply put, the income tax filed in May 2026 covers earnings from January 1 to December 31, 2025. Therefore, the 'previous year' referenced for the 2026 filing is actually 2024. For instance, if you start a business on January 1, 2025, and need to determine your bookkeeping method, you'd look at your 2024 sales figures to decide if you fall under the simplified bookkeeping category or the double-entry bookkeeping requirement. This previous year's sales data is a critical factor in determining your bookkeeping obligations and the expense ratios applicable for estimated tax filings.

Korean Income Tax: Bookkeeping vs. Estimated Filing Explained

Korean income tax filing primarily falls into two categories: bookkeeping (장부신고) and estimated filing (추계신고). Bookkeeping is the standard method for businesses, involving the calculation of net profit by subtracting actual expenses from actual income. This can be further divided into double-entry bookkeeping (복식부기), typically used by businesses with higher revenues and often requiring professional assistance, and simplified bookkeeping (간편장부), which is more accessible for smaller businesses. If maintaining detailed records is challenging, estimated filing offers an alternative. This method uses government-set expense ratios – either the simple expense ratio (단순경비율) or the standard expense ratio (기준경비율) – to calculate taxes.

Simple vs. Standard Expense Ratios: How to Choose?

The choice between the simple and standard expense ratios for estimated filing usually depends on your previous year's sales revenue. Businesses with lower previous year sales, generally below a certain threshold, often qualify for the simple expense ratio. This method allows a fixed percentage of your income to be recognized as expenses, which can be advantageous if your actual costs are low. Conversely, businesses exceeding the revenue threshold are typically subject to the standard expense ratio. This method prioritizes essential expenses like labor, materials, and rent, with additional deductions possible. However, if your actual business expenditures, particularly for materials, labor, or rent, are significantly high, the standard expense ratio might prove more beneficial than the simple one. It's advisable to compare both options or consult a tax professional to determine the most advantageous method for your specific business situation.

Common Mistakes and Precautions for Korean Income Tax Filing

Many taxpayers make mistakes during their income tax filing, such as misunderstanding the previous year's sales revenue criteria or neglecting their bookkeeping obligations. Another common pitfall is choosing the wrong estimated expense ratio (simple vs. standard) without a proper comparison, potentially leading to a higher tax burden than necessary, especially if actual expenses are substantial. It's vital to thoroughly assess your business scale and expenditure details before filing and to accurately confirm your previous year's sales to select the correct filing method. If bookkeeping is difficult or you're uncertain about the filing process, seeking assistance from a tax professional can ensure accuracy and optimize your tax outcome. Since income tax filing occurs annually in May, early preparation and understanding of the relevant information are key.

For more details, check the original source below.