Not all medical expenses are covered by Korean health insurance, even the widely popular 'Silson' (actual cost reimbursement) policies. Understanding the exclusions—like cosmetic procedures, routine check-ups, and items specifically excluded by policy terms—is crucial to avoid unexpected out-of-pocket costs. This 2026 guide details the main medical expenses that are typically not covered by Korean health insurance.

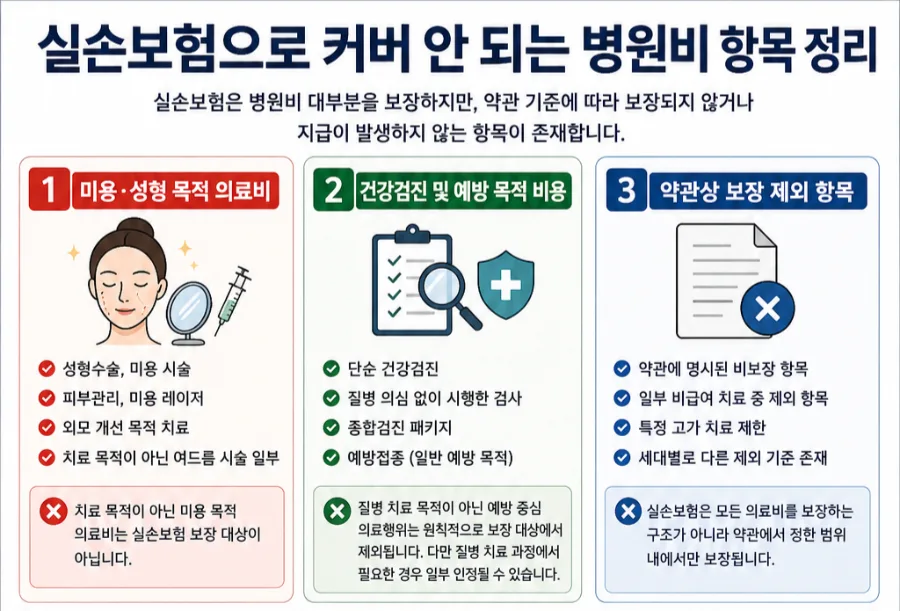

What Cosmetic and Plastic Surgery Costs Aren't Covered?

Korean health insurance primarily covers medical expenses for treating illnesses or injuries. Therefore, procedures aimed at improving appearance, such as plastic surgery, skincare treatments, or cosmetic laser procedures, are generally not covered. Even acne treatments may be excluded if deemed cosmetic rather than medically necessary. The key factor in determining coverage is whether the procedure was medically required. Many individuals find their claims denied when seeking reimbursement for purely aesthetic enhancements, highlighting the importance of understanding this distinction.

Why Aren't Routine Check-ups Covered?

Costs for general health check-ups or screenings performed when there's no suspicion of illness are typically not covered by health insurance. Similarly, preventative care measures or general wellness exams fall outside the scope of coverage. However, exceptions can be made if a specific test or preventative measure is deemed medically necessary as part of treating a diagnosed illness. For instance, if a patient has a confirmed diagnosis, subsequent tests or preventative actions required for managing that condition might be covered. Therefore, when claiming costs for a check-up, it's essential to demonstrate its direct link to treating a medical condition.

How Do I Check for Items Excluded by Insurance Policy Terms?

All Korean health insurance policies include specific non-covered items outlined in their terms and conditions. These can range from certain non-reimbursable treatments to high-cost procedures that may have limitations, and exclusions that vary by policy generation or specific plan. It is vital to thoroughly review your individual insurance policy documents to identify these excluded items. Understanding these exclusions beforehand can help prevent misunderstandings and disputes when you file a claim. For example, new, cutting-edge treatments for specific conditions might not yet be included in the policy's coverage list.

What Constitutes Medically Unnecessary Treatment?

A primary criterion for insurance claim approval is the medical necessity of the treatment received. Procedures for simple fatigue recovery, treatments administered without a clear diagnosis, or certain repetitive non-reimbursable therapies lacking strong medical evidence may be denied. Insurers evaluate the necessity of treatment by reviewing submitted medical records and established medical guidelines. It is advisable to have a thorough discussion with your healthcare provider about the medical justification for any proposed treatment before undergoing it. Based on experience, claims for treatments without a clear diagnostic basis are often difficult to get approved.

When Might My Insurance Payout Be Zero After Deductions?

Korean health insurance policies incorporate a deductible system. The amount reimbursed is calculated after deducting this deductible from the total medical cost. For minor outpatient treatments, it's possible for the final payout to be zero after the deductible is applied. This scenario is not due to an excluded item but rather a result of the insurance structure where the payable amount doesn't meet the minimum threshold for disbursement. For example, if your outpatient co-payment is 20% and you incur a $10 medical bill, you'd expect to be reimbursed $8. However, with small bills, the deductible might be a significant portion, or the claim might fall below a minimum payout threshold, resulting in no actual payment.

What Happens If I Don't Meet the Insurance Coverage Conditions?

Coverage under Korean health insurance can vary based on when you enrolled and the specific riders or add-ons you've purchased. Medical expenses incurred before the policy's coverage start date are, naturally, not covered. Furthermore, if you haven't subscribed to specific riders for certain treatments or conditions, your coverage for those items will be limited. Claims may also be denied if you fail to meet other conditions stipulated in your policy. Therefore, it's crucial to fully understand the coverage scope and terms of your insurance plan and select appropriate riders. It's a good practice to re-check your policy documents before submitting a claim to ensure the treatment is covered.

While Korean health insurance covers most medical expenses, it does not cover everything. It's essential to consider policy exclusions, medical necessity, and the deductible system when filing claims. Always verify if your treatment is eligible for coverage.